Mortgage – HousingWire |

- FHA backed $4.5B in mortgages without required flood insurance

- Homebuyers are really beginning to feel the squeeze

- Mortgage rates soar to 4.42% following rate hike

- New home sales are at risk with rising mortgage rates

- This global investment firm wants to become a non-QM rainmaker

- Homepoint to jump into the non-QM market

- Ginnie Mae announces the addition of two senior staffers

- Finance of America’s Jim Anderson on building customer relationships

- UWM targets real estate investors with new loan product

- Mortgage apps decline 8% amid rate hike

| FHA backed $4.5B in mortgages without required flood insurance Posted: 24 Mar 2022 02:42 PM PDT The Federal Housing Administration insured thousands of mortgages in 2020 without the mandatory flood insurance coverage. The potential loss on these loans could amount to $1.5 billion, an audit released this week by the Department of Housing and Urban Development Office of Inspector General found. According to the watchdog, at least 31,500 FHA-insured loans insured did not have the required National Flood Insurance Program coverage. Those loans, totaling close to $4.5 billion, either had private flood insurance, NFIP coverage that did not meet the minimum required amount or no coverage at all during 2020. The Department of Housing and Urban Development did not immediately respond to a request for comment. Properties located in special flood hazard areas must have national flood insurance program coverage. FHA does not permit borrowers to opt for private flood insurance. The watchdog report said that out of nearly 8.3 million loans with FHA insurance in 2020, approximately 197,747 loans are in areas that require flood insurance. The IG said that the administration did not have adequate controls in place to detect when loans did not have the required flood insurance. One of the problems the watchdog highlighted is that FHA did not require servicers to enter information into HUD’s systems to show compliance with federal flood insurance requirements. As a result, the administration did not have information on the coverage amount or whether an NFIP flood insurance policy was in place. The IG added that FHA's handbooks also failed to clearly communicate to servicers about the flood insurance requirements. The IG recommended the FHA require lenders to provide evidence of sufficient flood insurance and to better detect loans that did not maintain the required flood insurance. In doing so, "$1.5 billion [will be put] to better use by avoiding potential future costs to the FHA insurance fund from inadequately insured properties,” the report said. The IG also asked FHA to make any needed adjustments to the forward and reverse mortgage handbooks to ensure consistency with the law. By implementing these recommendations, HUD will be able to identify properties in its servicing portfolio that do not meet requirements and avoid risk from at least $4.5 billion in ineligible loans each year, the report said. The report marks the second time in recent years the IG has found that FHA failed to ensure loans in its portfolio were properly covered. An IG report in 2021 found that at least 3,870 loans were insured in 2019 without proper flood insurance, totaling $940 million. Although the NFIP services a significant chunk of homeowners, the program has had funding problems over the years, in part because Congress requires NFIP to charge discounted premium rates to policyholders. A report published by the Government Accountability Office in July 2021, found that as of August 2020, the Federal Emergency Management Agency, which manages the flood insurance program, had debt totaling $20.5 billion, even after Congress canceled $16 billion of its debt in October 2017. The rules surrounding flood insurance may soon change, to allow borrowers to opt for private flood insurance. A rule dubbed “Acceptance of Private Flood Insurance for FHA-Insured Mortgages ” is currently pending on the Office of Management and Budget‘s website. When implemented, it will undo regulations that have been in place since 1968, mandating that FHA borrowers with properties located in flood hazard areas must purchase government flood insurance. The FHA has said that allowing borrowers to choose private flood insurance could save them money. “Acceptance of private flood insurance policies would additionally benefit borrowers who want FHA-insured mortgages, by providing them consumer choice, including the opportunity to obtain private flood insurance policies that may be more affordable than NFIP policies,” the FHA said in the rationale for its proposed rule. The post FHA backed $4.5B in mortgages without required flood insurance appeared first on HousingWire. |

| Homebuyers are really beginning to feel the squeeze Posted: 24 Mar 2022 07:57 AM PDT The one-two punch of higher mortgage rates and escalating home prices reduced homebuyers' ability to buy homes in February. The trend is also likely to worsen in the coming months. The national median monthly mortgage payment settled in loan applications increased 8.3%, from $1,526 in January to $1,653 in February, according to a survey published Thursday by the Mortgage Bankers Association. Compared to February 2021, payments jumped 25.6%. Conventional loans' national median mortgage payment went from $1,582 in January to $1,749 in February. Meanwhile, FHA loans increased from $1,142 to $1,201 in the same period. "Low unemployment has spurred strong income growth in early 2022, but homebuyer affordability has decreased due to the quick rise in mortgage rates amidst steep home-price growth," said Edward Seiler, MBA’s associate vice president for housing economics and executive director at the Research Institute for Housing America, in a statement. Loan officers on Thursday told HousingWire that rate locks on 30-year fixed-rate mortgages were coming in around 4.75%, about 30 basis points higher than what Freddie Mac’s weekly PMMS report found. "Together with increased loan application amounts, a mortgage applicant's median principal and interest payment in February jumped $127 from January and $337 from one year ago," Seiler said. The new Purchase Applications Payment Index (PAPI) increased to 146.3 in February, compared to 135.1 in the prior month. In February 2021, the index was 120. A higher mortgage payment to income ratio means new loans are taking up a larger share of a typical person's income, due to increasing application loan amounts, rising rates, or a decrease in earnings. Mortgages comprehend a higher portion of Black households' income. The group's index went from 140 in January to 151.6 in February. For Hispanic households, it increased from 125.9 to 136.4 in the same period. For White households, the index grew to 147.9 in February, compared to 136.6 in January. The report also shows that mortgage payments for home purchases have increased relative to rents. The MBA's national mortgage payment to rent ratio (MPRR) rose from 1.01 in December 2020 to 1.14 in November 2021 and 1.15 in December 2021. The national median asking rent in fourth-quarter 2021 was $1,207, up 16% compared to the first quarter of 2020. Given that the Federal Reserve will likely begin hiking rates by 50 basis points as soon as May, affordability concerns are virtually certain to worsen in the months to come. The post Homebuyers are really beginning to feel the squeeze appeared first on HousingWire. |

| Mortgage rates soar to 4.42% following rate hike Posted: 24 Mar 2022 07:00 AM PDT The rollercoaster is still climbing. Mortgage rates are approaching 4.5%, a level economists forecasted would not be reached until the tail end of 2022. And there’s good reason to believe mortgage rates will be in the 5% range before too long. According to data from Freddie Mac's PMMS survey, mortgage rates on the traditional 30-year fixed-rate mortgage jumped 26 basis points to 4.42% this week, with increases across all loan types. "Rising inflation, escalating geopolitical uncertainty and the Federal Reserve's actions are driving rates higher and weakening consumers' purchasing power," Sam Khater, Freddie Mac's chief economist, said in a statement. He added: "In short, the rise in mortgage rates, combined with continued house price appreciation, is increasing monthly mortgage payments and quickly affecting homebuyers' ability to keep up with the market." The Fed made its first move to increase rates last week, raising the benchmark rate by a quarter of a percentage point. The Fed said there would likely be six more rate hikes in 2022 and three more in 2023, the primary tool the central bank is using to reduce inflation, which climbed to a 40-year high in February, at an annual rate of 7.9%. But last week, Fed Chairman Jerome Powell said he believed inflation was still too high and that the central bank would take ‘necessary steps’ to address it. He noted those rate rises could go from the standard 25 basis point moves to more aggressive 50 basis point increases starting in May. That would push mortgage rates even higher, potentially into the 5% range. Here's how home price appreciation impacts taxes – And what that means for servicers Real estate prices (and home appreciation) have been on a tear over the past few years. But sooner or later all this good fortune will translate into higher assessments and tax increases. Here's what servicers should be doing to anticipate tax issues this year. Presented by: LERETAThe 30-year-fixed rate rose 26 points from 4.16% for the week ending March 24, according to Freddie Mac. A year ago, the 30-year averaged 3.17%. Freddie Mac assumes borrowers bought 0.8 mortgage points on their loan. The 15-year fixed-rate mortgage averaged 3.63%, up from 3.39% last week. A year ago, the 15-year fixed-rate mortgage averaged 2.45%. The 5-year Treasury-indexed hybrid adjustable-rate mortgage averaged 3.36% with an average of 0.3 point purchase by borrowers, 17 basis points higher last week. A year ago, the 5-year ARM averaged 2.84%. The increase in rates in recent months has chilled activity in the mortgage market. According to the Mortgage Bankers Association, mortgage applications this week are down 8.1% from the prior week. The seasonally adjusted purchase index decreased 1.5% from one week earlier and was 12% lower year-over-year. Meanwhile, refi applications fell 14.3% from the prior week and were down 54.2% from a year ago. The post Mortgage rates soar to 4.42% following rate hike appeared first on HousingWire. |

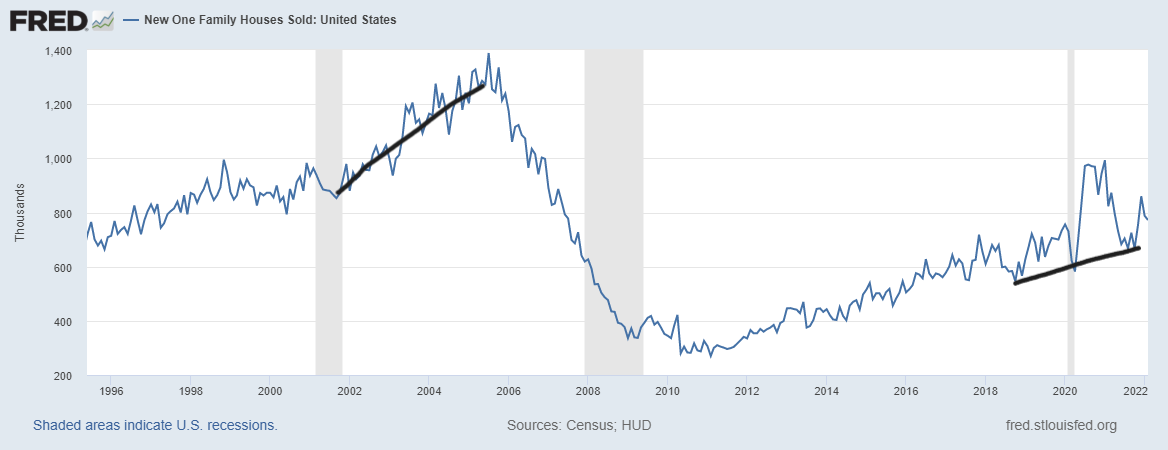

| New home sales are at risk with rising mortgage rates  Posted: 23 Mar 2022 03:16 PM PDT  We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housing market was last year — and it got a lot worse this year — it's a blessing that was much needed. Recently, I downgraded the housing market from an unhealthy housing market to a savagely unhealthy housing market, something I discussed with HousingWire Editor in Chief Sarah Wheeler on our recent podcast. For 2020-2024, I set some critical parameters for sales and price growth, knowing that this marketplace will be different from the market we had from 2008 to 2019. This is why I always separate my work into those two periods. First, total home sales should be 6.2 million or higher during 2020-2024. This is new home sales and existing home sales combined. The demographic bump in 2020-2024 is giving us a push in demand. The fact that the 23% home-price growth level has been smashed in just two years and inventory just collapsed to all-time lows has created the most unhealthy housing market post-2010. The only risk to that 6.2 million line in the sand has been this:

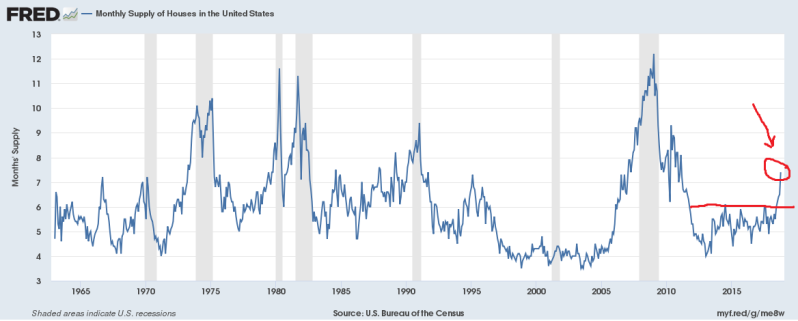

The two things I had as risk factors are now in play. We have a risk to sales here, and the one area where we could be most in trouble is the new home sales sector. This sector on an apples-to-apples basis is more expensive than the existing home sales market. It’s also driven more by mortgage buyers who tend to be older and make more money than the new-home buyers. Compared to the existing home sales marketplace, it doesn't have a high cash buyer or investor buyer profile. Today, new home sales came in as a miss of estimates at 772,000, but the revisions were all positive so there’s not too much going on here. The builders are struggling to finish their homes, and there is a risk to builders in a rising rate environment when you have people wait so long to build a house. Regarding the new home sales sector itself, it's just an OK marketplace and has been for some time. From Census: Sales of new single‐family houses in February 2022 were at a seasonally adjusted annual rate of 772,000, according to estimates released today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 2.0 percent (±11.9 percent)* below the revised January rate of 788,000 and is 6.2 percent (±13.7 percent)* below the February 2021 estimate of 823,000. As you can see below, the new home sales market from 2018-2022 doesn't look like the housing market we had from 2002-2005. Without exotic loan debt structures, credit always has limits, which is a good thing. Could you imagine this housing market if we eased lending standards? I would be protesting in front of Congress and speaking at congressional hearings if lending standards were reduced. My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

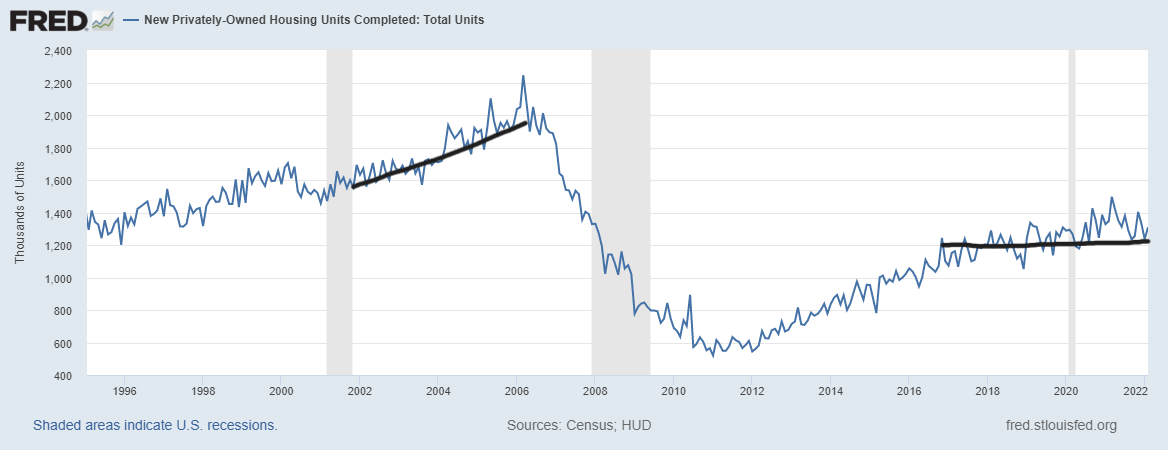

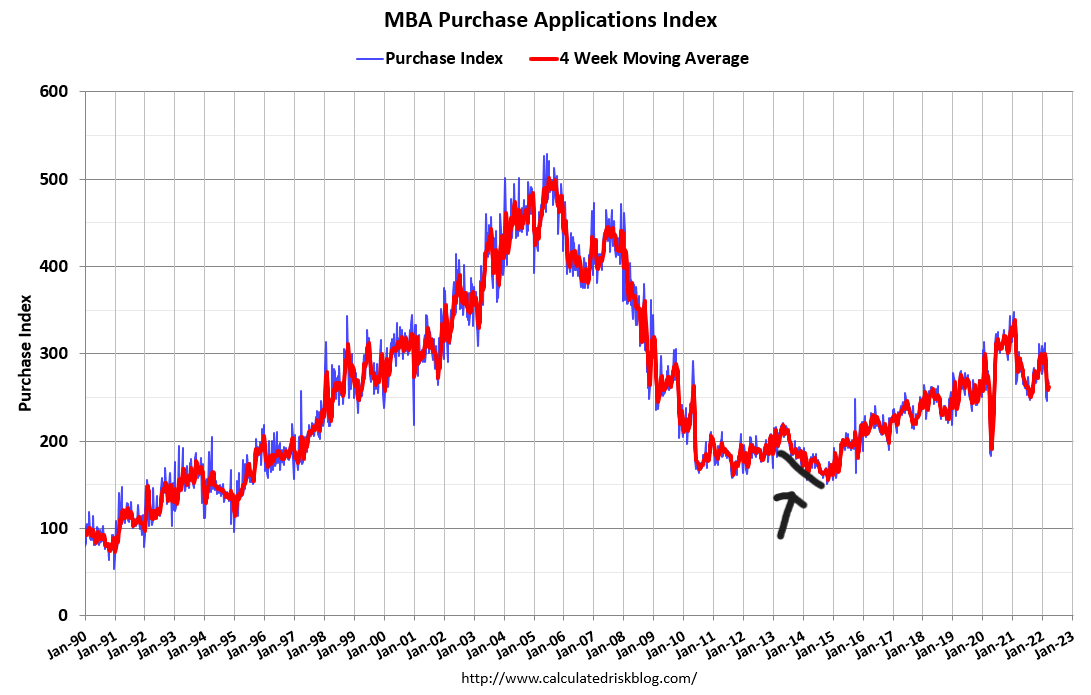

As you can see below, the completion data looks terrible. It's taking forever to build a home and that has created a huge number of homes under construction. The risk is that cancellations can rise by the time the home is ready for move in. As always, the years 2020-2024 were going to be different. The builders have pricing power that means they can push the price onto their consumers. Like home sellers, they try to make as much money as possible. The only thing we have that creates balance in this market is higher rates, hence why I am team higher rates. Purchase application dataRegarding the purchase application data that came out on Wednesday, some context needs to be discussed here. Purchase application data is down 2% week to week, 12% year over year. This data line has been negative year over year since June of 2021. A big theme of my work on HousingWire is to try to talk about housing data making COVID-19 adjustments because if you didn't realize that we had some high comps due to the make-up demand of COVID-19, you might have thought housing was crashing in the middle of last year. First, as you can see from the chart below, the market we had from 2002-2005 never existed in housing from 2014-2022. We cannot have a credit boom because speculation debt has been taken off-grid post-2010 with credit. It was always a slow and steady ride from the 2014 lows. This is the year-over-year data since the start of the year. I have talked about how we would still have some makeup demand COVID-19 comps into February, and that’s what happened from my view: makeup demand spilled over into early 2021.

Those make-up demand comps are now gone.

Now, this week the year-over-year data shows -12%. You can see some of the weakness, but nothing too drastic. We can compare these previous times when housing was soft too. Speaking at a housing conference in 2019, I explained to the audience that it was a good thing that real home prices went negative. I had a big smile back then as housing was balanced. We don't have a balanced housing market any longer. Why won’t inventory grow? At the end of 2017, existing home sales went from 5.72 million and trended toward 4.98 million by Jan 2019, and we saw no inventory growth back then! Housing tenure has doubled; homeowners on paper in 2018-2019 were already in great shape and now look better than ever on paper with the last refinance boom. What a hedge against inflation this year! But, housing tenure has become a severe problem in the housing market as inventory is collapsing in 2022. While I am on team higher rates and welcome this significant bit of news to try to create more days on the market to cool this terrible home-price growth down, I am not blinded by the reality that this can also cause issues with home sellers who want to buy a home. Home seller data has been showing some stress, and that is the last thing I wanted to see right now. However, it makes sense when inventory has collapsed to such low levels, and now rates are higher. Are you going to risk selling your home, not getting the home you want, and renting at a higher cost? This is the last thing I wanted to see in 2022, and since we are so close to April, it's a reality we have to deal with for the rest of the year as long as inventory is still negative year over year. Going out for the rest of the year, keep an eye out for that new home sales data. One of my six recession red flags is that new home sales and housing starts fade into a recession. Because the new home sales marketplace means more to an economy than the existing home sales marketplace, it's more important to look at that. Housing construction jobs and big-ticket item purchases are things that move with the demand of new homes. The existing home sales market results in a transfer of commission, moving trucks and some big-ticket item purchases. Going back to my summer of 2020 premise of what can cool down the housing market, a 10-year yield over 1.94% should. Even though mortgage rates are still low historically, rising rates do matter, and with the home-price growth we saw in 2020, 2021 and 2022, it matters even more. You can see why I believe in economic models; they keep us in line. The post New home sales are at risk with rising mortgage rates  appeared first on HousingWire. |

| This global investment firm wants to become a non-QM rainmaker Posted: 23 Mar 2022 12:41 PM PDT  Minneapolis-based CarVal Investors, a global alternative investment manager and long-time player in the mortgage market, has launched a real estate mortgage investment conduit, or REMIC, that plans to work with loan originators around the country to develop and acquire innovative nonagency mortgage products. The new REMIC, Mill City Loan Holdings LLC, will serve as a mortgage conduit for funds managed by CarVal while also developing relationships with originators to acquire "residential mortgage assets across multiple strategies," according to a CarVal statement announcing the launch of the REMIC, which will do business as Mill City Loans. A REMIC is a special purpose tax vehicle that holds pools of mortgages and issues multiple classes of ownership interests to investors in the form of pass-through securities, such as bonds. REMICs are tax exempt under federal law, although the income earned by investors is taxable. "We expect it to be a challenging [mortgage] market from a volume perspective due to interest rates and credit spreads," said David Pelka, head of RMBS business and a principal at CarVal. "However, we are optimistic on both opportunistic mortgage-loan acquisition opportunities as well as continued product evolution of non-QM — not just this year, but through this economic cycle. "This is why our funds founded a mortgage conduit, Mill City Loans." CarVal Investors is a major player in the investment management world, with a focus on acquiring, managing, selling and securitizing loans, including credit-intensive assets, such as non-QM mortgages. Pelka said his firm has invested more than $24 billion in nearly 2,000 loan portfolio transactions globally since 2014. CarVal, which also has offices in New York, London, Luxembourg and Singapore, currently has more than $11 billion in assets under management — including corporate securities, loan portfolios, structured credit and hard assets. The investment management firm and its affiliated funds also are active in both the residential whole loan and RMBS markets, with some 30 years of experience buying, managing and trading nonperforming, sub-performing and reperforming loans. CarVal has acquired $10 billion in whole loans over the past decade and a half, Pelka added, and securitized $5 billion in residential mortgages, primarily through its Mill City Mortgage Loan Trust shelf. As the mortgage market transitions from a refinancing-dominated cycle to one where rising rates move purchase mortgages to the forefront, Pelka said he expects many originators will be looking for more inroads into that purchase market, such as innovative non-QM loan products. CarVal's new REMIC will act as a tool for providing liquidity for that evolving market, according to the Mill City Loans website. "Mortgage volumes overall will be under pressure as long as rates are high, increasing and/or volatile," he said. "Non-QM will need to be re-priced to higher coupons as well, which will also impact volumes. "I expect it will be a challenging environment for originators," Pelka added, "which is why we are excited to have Mill City Loans as a mortgage conduit to meaningfully partner with originators to offer interesting nonagency mortgage products." The range of nonagency, non-QM mortgage products is broad and encompasses the self-employed borrower as well as entrepreneurs who purchase investment properties — and who can't qualify for a mortgage using traditional documentation, such as payroll income. As a result, they must rely on alternative documentation, including bank statements, assets or, in the case of rental properties, debt-service coverage ratios. Non-QM mortgages also go to a slice of borrowers facing credit challenges — such as a recent bankruptcy or slightly out-of-bounds credit scores. The loans may include interest-only, 40-year terms or other creative financing features often designed to lower monthly payments. Pelka said Mill City loans will be led by mortgage-industry veterans Trey Jordan, former general counsel at New York Mortgage Trust; Mike Petersen, a former TCF Bank executive with experience in capital markets and loan-portfolio management; and Kent Usell, a mortgage and investment banking expert who worked previously at New York Mortgage Trust and alternative investment firm Oak Hill Advisors. "We see significant opportunity," Pelka said, "both navigating the current uncertainty, but also partnering with originators [through Mill City Loans] to develop meaningful nonagency mortgage products." The post This global investment firm wants to become a non-QM rainmaker appeared first on HousingWire. |

| Homepoint to jump into the non-QM market Posted: 23 Mar 2022 11:36 AM PDT  Add Homepoint to the list of lenders entering the non-QM market in 2022 amid a fall in origination volume. The wholesale lender is preparing to launch two non-qualified mortgage products this year, including bank statement and investor cash flow loans. “We’re currently in the process of assessing our entry point into non-QM loans. Our team has experience working with those products,” Phil Shoemaker, Homepoint’s president of originations, told HousingWire. The non-QM sector, which largely includes self-employed borrowers and those who work in the gig economy, is expected to take off in a landscape in which accelerating home prices and higher interest rates push borrowers outside the Fannie Mae and Freddie Mac credit boxes. So far, United Wholesale Mortgage (UWM), the nation’s largest wholesale lender, has launched new non-QM offers. In March, the lender announced a bank statement product for self-employed borrowers and loans for real estate investors. Current government-sponsored enterprise guidelines make it difficult for these borrowers who don’t have a traditional salary to qualify for agency-backed loans. According to Shoemaker, Homepoint will also pursue borrowers who fall into those buckets: one that allows borrowers to qualify for loans based on their bank statements as opposed to a traditional W2 salary; and the other for real estate investors, a business purpose loan that considers the investor cash flow. The executive said Homepoint will not rush to launch the products because it requires an efficient operational infrastructure, as it is not “something you can haphazardly jump into.” “We do believe that in a purchase market, products will become more and more important,” Shoemaker said. “We’ve been focused on jumbo, and then we will be leaning into non-QM in a very responsible way because there’s a lot of borrowers out there that are underserved by either the prime jumbo market or the agency market.” Based on the recent home appreciation across the country, the Michigan-based lender launched the Homepoint Jumbo Preferred in January, with flexibilities such as delayed financing and loan amounts for qualified borrowers that begin with $1 above conforming county loan limits up to $2.5 million. The product does not require mortgage insurance on primary residential loans with up to 90% loan-to-value (LTV). It is available in 15- year and 30-year fixed terms, on purchases and rate-and-term on primary, secondary, and investment properties. Shoemaker said the home appreciation is “here to stay” due to the imbalance between supply and demand. Another product Homepoint is preparing to launch is a partnership with a company to help homebuyers compete in cash offers – the executive did not share more details about the product. “You do see several startups out there trying to solve this. We want to be on the leading edge of solving this problem. But you will see a pretty rapid expansion of these options across all vendors.” The higher-rate landscape has chipped away at the profitability of Homepoint’s parent company, Home Point Capital, in recent quarters as margins in wholesale have declined. The company turned a $19.3 million profit in the fourth quarter, a sequential decline from the $71 million it notched in the third quarter. But Home Point Capital was largely saved by a sale of $13.1 billion in Ginnie Mae servicing rights, which generated nearly $175 million. Homepoint is exiting the Ginnie Mae servicing space, and recently announced it would also move all of its mortgage servicing processing work to ServiceMac, another cost-cutting move. The post Homepoint to jump into the non-QM market appeared first on HousingWire. |

| Ginnie Mae announces the addition of two senior staffers Posted: 23 Mar 2022 09:50 AM PDT Ginnie Mae recently filled two executive roles, naming Sam Valverde as its first Hispanic executive vice president and Felecia Rotellini as senior advisor and chief of staff to the president. Alanna McCargo, president of Ginnie Mae, announced the appointments during the National Association of Hispanic Real Estate Professionals conference that took place in Washington D.C. last week. During the conference, McCargo stressed the importance of having diversity in leadership. She also expressed the need to make liquidity available for smaller community-based players. "We must have leaders that look like and understand the communities we ultimately serve," McCargo said. Both Valverde and Rotellini have a background in law and regulatory compliance. Prior to his appointment at Ginnie Mae, Valverde worked at the Federal Housing Finance Agency (FHFA) as a supervisory attorney advisor in the division of conservatorship oversight and readiness. How Mortgage as a Service Levels the Playing Field for Minority and First-Time Homeowners This white paper explores the benefits of closing the homeownership gap, systemic mortgage industry issues, and how Salesforce is partnering with Rocket Mortgage to enable mortgage as a service and increase minority and first-time homeownership. Presented by: SalesforceDuring his time at the FHFA from 2017 to 2022 , Valverde led agency-wide projects intended to support greater access to mortgage credit and affordable rental opportunities for working families. Additionally, Valverde worked to develop a post-conservatorship regulatory framework for the government-sponsored enterprises. Valverde also served as a counselor for domestic finance at the U.S. Treasury Department from 2010 to 2017. Rotellini joins Ginnie Mae from DriveTime, a used car retailer and finance company, where she worked from 2015 to 2021 as a director of compliance. Rotellini also worked as an attorney for five years at Zwillinger Greek Zwillinger & Knecht, PC, a commercial law firm. And she has a 13-year stint under her belt as an assistant attorney general at Arizona’s Attorney General’s Office from 1992 to 2005, according to Linkedin. Ginnie Mae, in a press release, said that Rotellini has experience in building diverse coalitions which will help advance the public and stakeholder engagement strategy for the government guarantor. "Sam and Felecia are great complements to our executive leadership team and will be integral to the organization as we advance our strategic roadmap and strengthen our service to the nation's diverse housing market," McCargo added. "I am thrilled to have their counsel and support as we work with all of our stakeholders to create broader and more equitable access to affordable homeownership and rental housing." The post Ginnie Mae announces the addition of two senior staffers appeared first on HousingWire. |

| Finance of America’s Jim Anderson on building customer relationships Posted: 23 Mar 2022 08:40 AM PDT The HousingWire award spotlight series highlights the individuals who have been recognized through our Editors' Choice Awards. Nominations for HousingWire's Marketing Leaders award are now open through Friday, March 25, 2022. Click here to nominate someone you know — it can even be you! As the housing market continues to move from last year's refinance boom, lenders’ ability to identify customers and maintain consumer relationships has become more important than ever in not only securing loans but also ensuring they make it to close. "Marketers and loan officers need to be prepared for a longer lead-nurture timeline today than the refi market frenzy we experienced the last two years," said Jim Anderson, chief marketing officer at Finance of America Mortgage. “From the bottom up, our goal is to build a lifelong relationship around mortgage lending.” Lenders like Finance of America need to be ready to engage with potential and past customers at all points of the home-buying journey across web, mobile and social, added Anderson. That's where marketing teams like Anderson's are working to support loan officers in initiating and building on a consultative relationship with their customers, versus the transactional approach many lenders are often known for. Jim Anderson was honored as a 2021 HW Marketing Leader, an award that celebrates the most creative and influential marketing execs of the housing economy. HousingWire reached out to Anderson to learn more about how lenders and marketers can prepare for the current housing market and to hear about what's to come at Finance of America in 2022. HousingWire: What projects are you working on that you’re most excited about in 2022? Jim Anderson: We’ve just kicked off a customer segmentation project to identify purchase patterns and to group customers into personas with behavioral attributes. We’re also developing an algorithm to identify future customers’ personas quickly. Understanding our customers and their motivations will allow us to tailor personalized messages and content on their preferred platform to drive increased engagement. From the bottom up, our goal is to build a lifelong relationship around mortgage lending. We want to support our loan advisors in building a consultative relationship with their customers, versus the transactional approach many lenders employ. HousingWire: How is your team handling the compliance aspects of the digital marketing space? Jim Anderson: Finance of America Mortgage's field marketing team continually coaches and consults with our branches and loan advisors to maximize the marketing potential and ensure marketing meets all federal and local compliance guidelines. Our internal marketing QC team reviews and consults all materials and the compliance team actively monitors social media and the web to ensure compliance. Finance of America offers a robust mar-tech stack, working with the best technology partners in the business. We constantly evaluate new vendors to ensure our loan advisors have options that complement their unique business. HousingWire: What role are marketers playing in this current purchase-driven market and in what ways can marketing act as a revenue driver right now? Jim Anderson: With the decrease in refinance volume, you’ll see a shift to driving top-of-funnel purchase leads. Homebuyers often search for financing online before engaging a Realtor. This provides an opportunity for mortgage lenders to engage with customers as they evaluate how much home they can afford. However, marketers and loan officers need to be prepared for a longer lead-nurture timeline today than the refi market frenzy we experienced the last two years. We're ready to engage with potential and past customers at all points of the home-buying journey across web, mobile and social. Plus, our marketing team actively monitors our past customers to funnel leads for referrals, purchases and refinances to our loan advisors. We leverage propensity models to proactively identify customers ready for another transaction, combined with ongoing credit and listing monitors to re-engage with our past customers. The post Finance of America’s Jim Anderson on building customer relationships appeared first on HousingWire. |

| UWM targets real estate investors with new loan product Posted: 23 Mar 2022 08:00 AM PDT United Wholesale Mortgage (UWM), the nation's largest wholesale lender, announced on Wednesday a new product that will qualify borrowers for investment properties based on the monthly rental income, rather than the their current income. This is the second new non-QM product the Pontiac-based lender has launched this month – the wholesale lender also unveiled a bank statement loan product for self-employed borrowers. Rising interest rates, already in the mid-4% range, have dramatically slowed refinancings, forcing originators to look toward other products that entice purchase buyers or those with equity in their existing homes. According to UWM, the product called Investor Flex is a 30-year fixed Debt-Service Coverage Ratio (DSCR) loan option for real estate investors. It is available on purchase and refinance loans up to $2 million and can be used to finance up to 20 properties. "It will also be offered for short-term rental properties, giving brokers another competitive selling point when targeting real estate investors," the company said in a statement Wednesday. The new product targets real estate investors, a group that represented 16.4% of all home sales in the third quarter of 2021, according to the RealtyTrac Investor Purchase Report. How to minimize tenant turnover using online property management tools Tenant turnover costs money and time. Here’s a look at why tenant turnover happens and how to prevent it in the future. Presented by: TenantCloudInvestors paid a median purchase price of $245,000 to fix-and-flip and long-term rental properties, compared to a median price of $302,000 for all home purchases. But most of them pay in cash: 79% of all investor purchases were cash sales in the third quarter of 2021. "Rising home prices and inflation make it difficult for investors to achieve their return on investment (ROI) objectives, but they make it even harder for the average consumer to afford to buy a property," Rick Sharga, executive vice president at RealtyTrac, said in a statement. He added: "So, even though investor profit margins may be declining, it's possible that we will continue to see the investor share of purchases increase over the next few quarters." The post UWM targets real estate investors with new loan product appeared first on HousingWire. |

| Mortgage apps decline 8% amid rate hike Posted: 23 Mar 2022 04:00 AM PDT Interest in residential mortgage loans fell 8.1% for the week ending March 18 as mortgage rates rose to 4.5%, the highest level in years, according to the Mortgage Bankers Association's latest survey. "The jump in rates comes as markets moved to price in a much faster pace of rate hikes, as well as expectations of fewer MBS purchases from the Federal Reserve," Joel Kan, associate vice president of economic and industry forecasting for the MBA, said in a statement. The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $647,200) increased to 4.50% from 3.27%, with points increasing to 0.59% from 0.54% (including the origination fee) for 80 percent LTV loans. The 23 basis points increase last week was the largest weekly change since March 2020. Higher rates have significantly impacted the refinance activity, both for conventional and government loans. According to the MBA, refi applications fell 14.3% from the prior week and were down 54.2% from a year ago. Meanwhile, the seasonally adjusted purchase index decreased 1.5% from one week earlier and was 12% lower year-over-year. According to Kan, purchase FHA and VA applications had a larger drop, compared to a small decline in purchase conventional apps. "First-time homebuyers, who rely on these government programs, are increasingly challenged by both the rapid increase in home prices and higher mortgage rates," he said. "Repeat homebuyers, who are more likely to use conventional loans, benefit from the gains in home equity realized on a sale which can be used to fuel their next purchase, even with rates moving higher." How Mortgage as a Service Levels the Playing Field for Minority and First-Time Homeowners This white paper explores the benefits of closing the homeownership gap, systemic mortgage industry issues, and how Salesforce is partnering with Rocket Mortgage to enable mortgage as a service and increase minority and first-time homeownership. Presented by: SalesforceThe MBA found that the refi share of mortgage activity decreased to 44.8% of total applications last week, from 44.8% the previous week. The adjustable-rate mortgage share of the activity increased from 5.6% to 6.4% of total applications. The FHA share of total applications went from 8.7% to 8.8%, and the share of VA applications decreased from 10.5% to 9.8%. The post Mortgage apps decline 8% amid rate hike appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment