Mortgage – HousingWire |

- Unemployment rates and mortgage rates both under 4%

- [video] The three most important housing factors for 2022

- Consumer direct mortgage lender lays off 35 LOs

- HW+ Member Spotlight: Joe Langner

| Unemployment rates and mortgage rates both under 4% Posted: 07 Jan 2022 02:11 PM PST  Today, the Bureau of Labor Statistics reported that 199,000 jobs were created in December — a miss from estimates. They also reported we had 141,000 in positive revisions to the previous jobs report. The unemployment rate is currently at 3.9% and we had another big print from the household survey which showed 651,000 jobs gained. For men and women age 20 and over, the unemployment rate is currently at 3.6%.

With nine months left until the end of September 2022 (the milestone in my forecast), let's see how much progress we need:

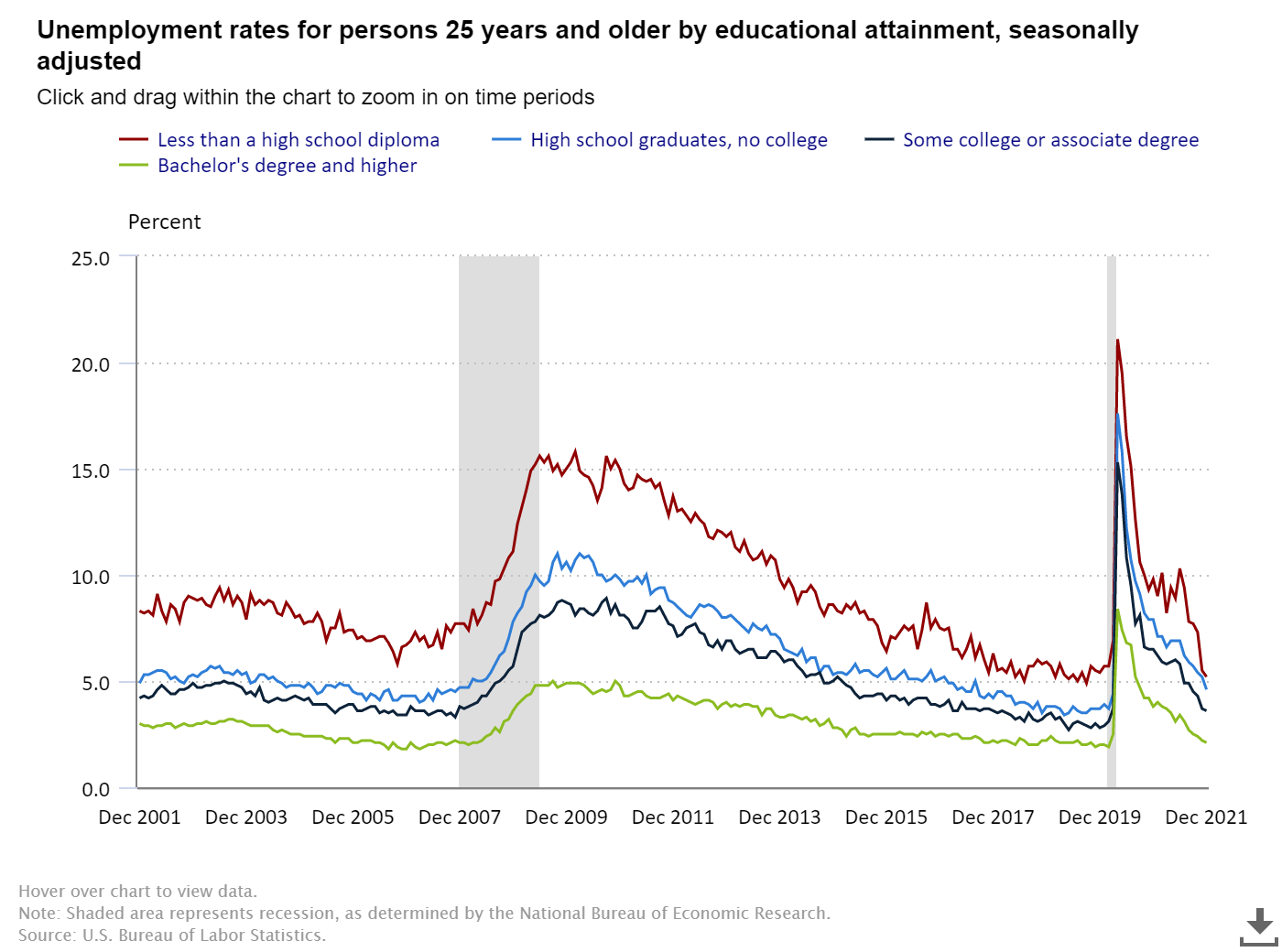

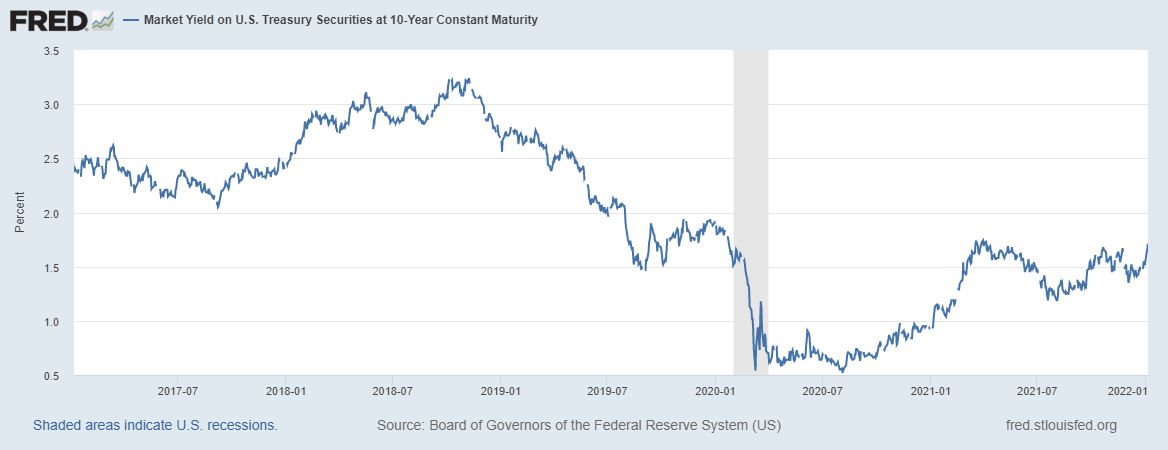

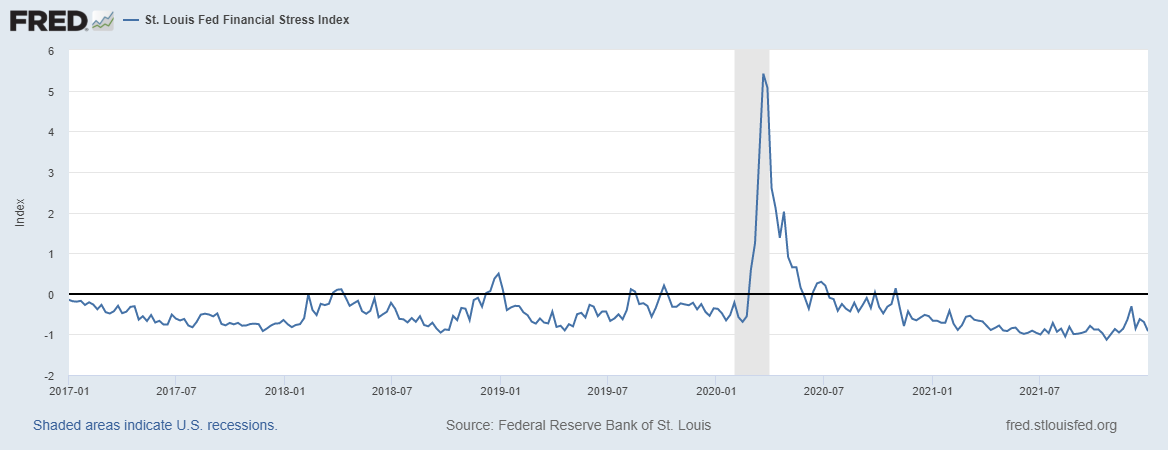

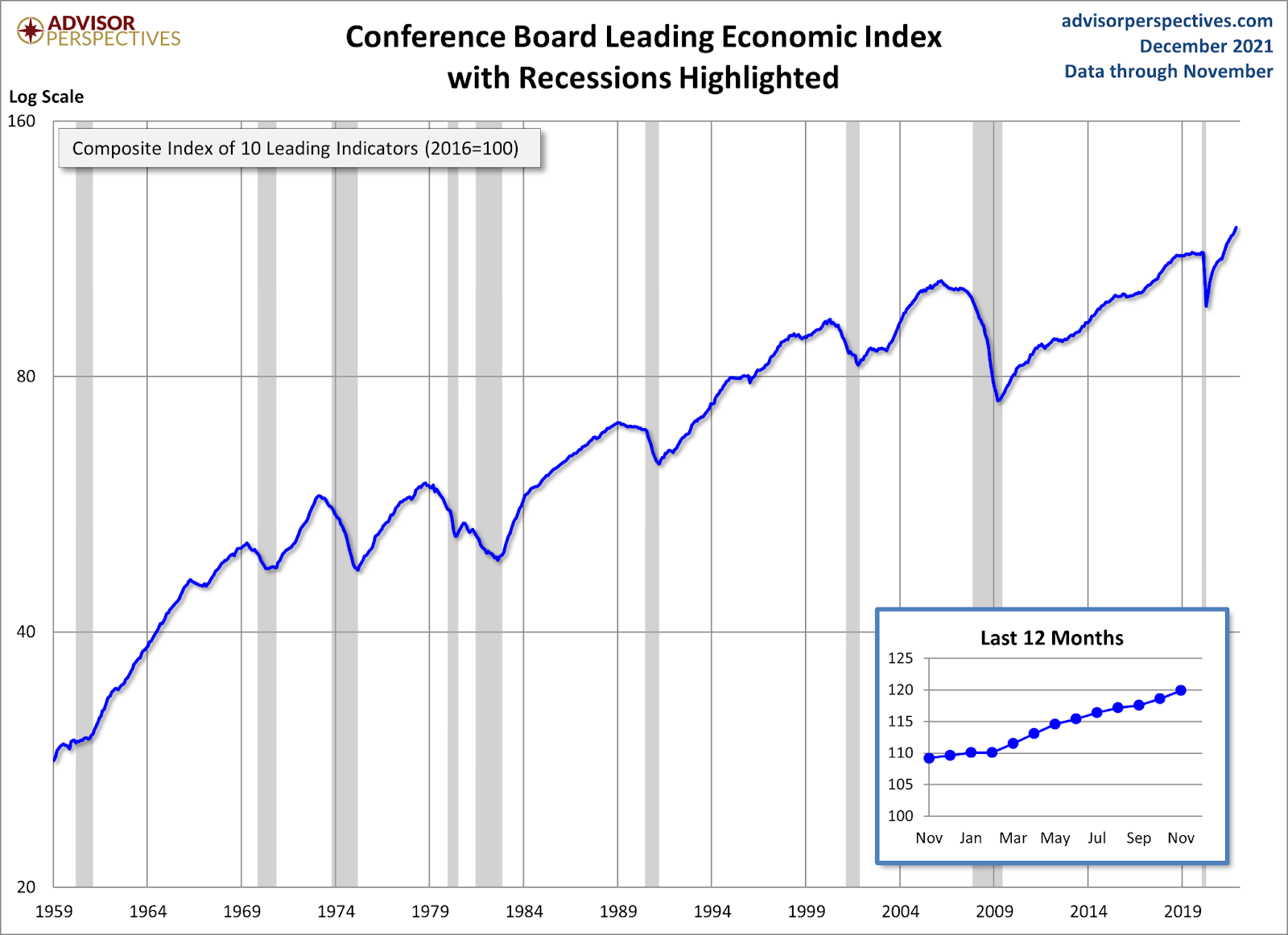

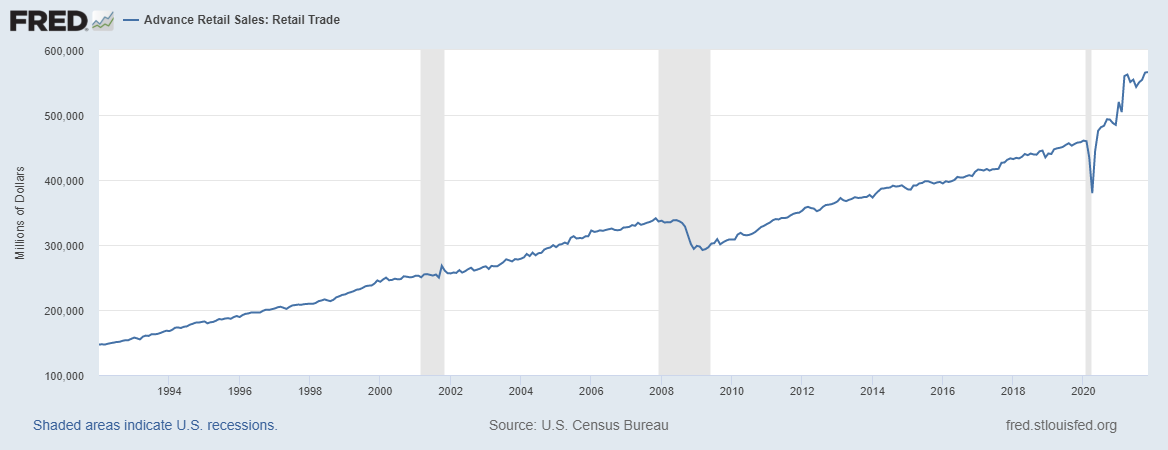

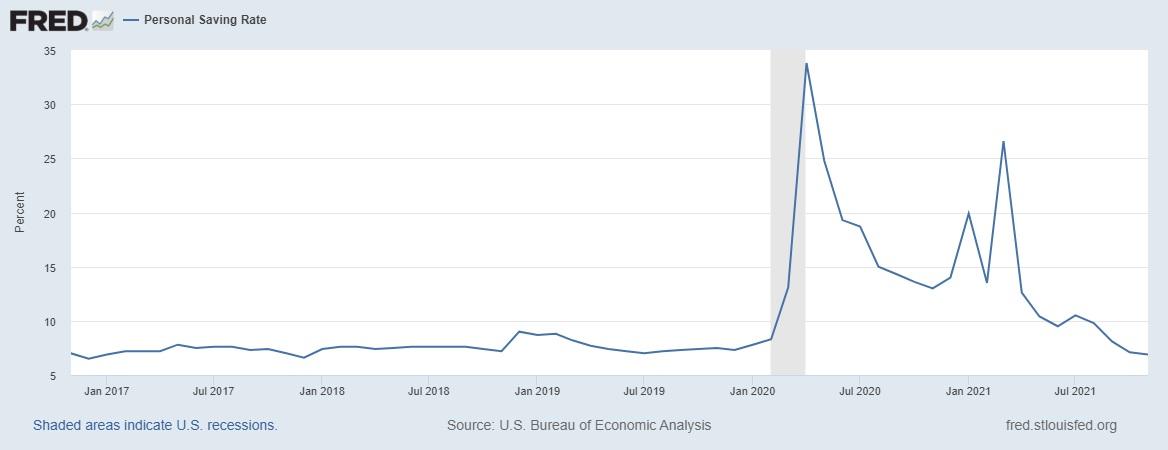

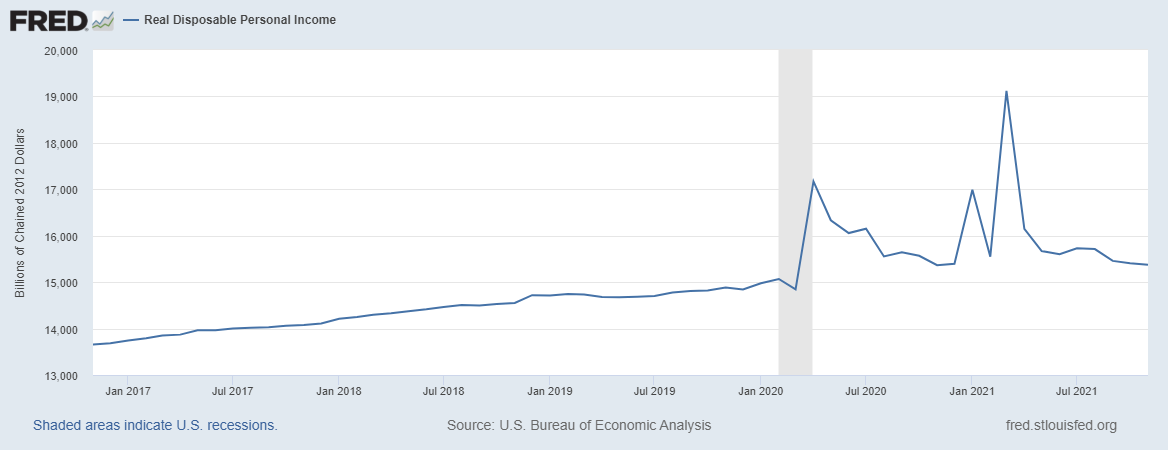

Here is a look at the job gains and losses reported today. Construction jobs came in positive but we still have a fairly high level of construction job openings currently. The lack of construction productivity over the decades has been one reason why I have never believed in a housing construction boom in America. The other reason is that the builders don't ever oversupply a housing market, so when demand fades, so will construction. The builders have been complaining about labor for many years. However, the builders confidence index has picked up because they believe they can sell their product and make money since they have pricing power. This also means housing starts are rising. Don't make it more complicated than it needs to be. Education and employmentMost people who want to work in our country are employed on a regular basis. I know that some people blame COVID-19 for not going back to work, but context is key: the majority of the country’s population is working today. The part of the labor force with the least educational attainment tends to have a higher unemployment rate. On Twitter, I started the hashtag A Tighter Labor Market Is A Good Thing to remind everyone that the economy runs hot when we have a tighter labor market. We want to see the kind of unemployment rates that college-educated people have spread to everyone, because we have tons of jobs that don’t need a college education. The unemployment rate for those that never finished high school has been falling sharply lately, which means the labor market is getting tighter and tighter every month. You want to have this problem rather than the other way around. Here is a breakdown of the unemployment rate and educational attainment for those 25 years and older: —Less than a high school diploma: 5.2%. As you can see above, life is great for those looking for a job. For companies that need labor, it's not the best news, but again, it’s first-world American problems — the economy is hot! As I have stressed from April 7, 2020, the U.S. recovery was going too fast, which would shock many people because they had no faith in their economic models. With near record-low unemployment and massive job openings, you would assume mortgage rates should be skyrocketing, but they’re not. My 2022 forecast said: For 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper end range in mortgage rates is 3.375%-3.625% and the lower end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981. We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don't support this. Yes, it does seem strange, we have the hottest economy in decades and inflation is hot but the 10-year yield as I write this is at 1.75%. Don't forget the trend is your friend on bond yields and mortgage rates for decades. We had a major fall in headline inflation that didn't take bond yields lower in the same way in 2009-2010 and now you're seeing the reverse with a short-term spike in the inflation rate of growth with yields not rising either. Even though we haven't tested 1.94% yet, we are getting to an exciting area where we might be able to see the first real test of 1.94% since 2019. Keep an eye on the close of the 10-year yield today and see if we get some bond market sell-off next week. If not, the bond market can rally and yields can fall short term as we are oversold on the bond report. Economic cycle update Now for an economic update. So far, so good, even with the Omicron cases exploding higher, we simply don't see the economic and market reacting any more as we have learned to consume goods and services with an active virus infecting and killing us each day. This has been the case since the second surge in 2020, and even though sectors of the economy will not perform at total capacity with cases rising, it's just not like what we saw in March of 2020. The St. Louis Financial Stress Index, a crucial variable in the AB recovery model, is still acting bored out of its mind with a recent print of -0.9201%. This will rise when the markets react to stress, so don't assume we will be at these low levels forever. We still haven't had a stock market correction of 10% plus since the March lows in 2020. The leading economic index has been very solid lately, when this data line falls for 4-6 months straight, then the topic becomes different. However, this hasn't been the case, it bottomed in April of 2020 and has had a sharp rebound. Retail sales are still off the charts, but I don't believe we can have the type of growth we saw last year. Moderation is the key to retail sales data going out, but what a crazy ride in 2021. Expect less purchases on goods and more service spending going out, especially when we are finally done with COVID-19. The personal savings rate and disposable income are very healthy to keep the expansion going! Even though the disaster relief has faded from the economic discussion, both these levels are good to go as employment has picked up a lot from the COVID-19 lows. However, just like I had an America is Back recovery model on April 7, 2020, I have recession models and raise recession red flags as the expansion matures. In the previous month's jobs report, I raised one of the flags as the unemployment rate got to 4% and the 2-year yield was above 0.56%, which means the Fed rate hike is on. Once the Fed raises rates, the second recession red flag will be raised. My job is to show you the progress of the economic expansion, into the next recession, and out — over and over again. My models don't sleep! Once more red flags are raised, I will go over each and every single one. At some point in the future, I will be on recession watch, when enough red flags are up. However, we are not in that time yet. Even though I no longer say we are early in the economic expansion, we are still on solid footing. The post Unemployment rates and mortgage rates both under 4% appeared first on HousingWire. |

| [video] The three most important housing factors for 2022 Posted: 07 Jan 2022 11:24 AM PST This video is part of our HousingWire 2022 forecast series. After the series wraps in January, join us on February 8 for the HW+ Virtual 2022 Forecast Event. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the predictions for this year, along with a roundtable discussion on how these insights apply to your business. The event is exclusively for HW+ members, and you can go here to register. In this video interview, HW+ Managing Editor Brena Nath sits down with Housingwire Lead analyst Logan Mohthashami as he breaks down his predictions for the new year. Mohtashami shares his perspective on where mortgage rates and home prices are headed, along with the future of inventory. Watch the full session below and here is a small preview of the interview, which has been lightly edited for length and clarity: Brena Nath: Everyone’s also looking at home prices right now since they all kind of work together and impact each other. So where do you view home prices going in 2022? Logan Mohthashami: Unfortunately, my biggest fear for 2021 was that home prices would accelerate, and we’re still at a level where total inventory is below 1.5-2 million. And for me, as long as it’s below that, it’s not a good thing. Home price growth can facilitate higher prices, but we do not want the repeat of 2021. So inventory is going to fade, you know like it does in the fall and winter. However, if rates do pick up a little bit or housing slows down, it’s a positive. We want more inventory. The post [video] The three most important housing factors for 2022 appeared first on HousingWire. |

| Consumer direct mortgage lender lays off 35 LOs Posted: 07 Jan 2022 10:28 AM PST Pink slips arrived for nearly three dozen loan officers at Wyndham Capital Mortgage on Wednesday, HousingWire has learned. The consumer direct mortgage lender, headquartered in Charlotte, North Carolina, said it laid off 35 LOs across its offices in Dallas, Charlotte, Salt Lake City, Kansas City, and Phoenix. In a statement, Jeff Douglas, CEO of Wyndham Capital Mortgage, said that the company is "well-positioned and continues making investments to compete in a purchase market and is poised to gain market share to meet the needs of today's borrowers." Last year, Wyndham actively expanded, opening two hubs in Dallas and Phoenix, which pushed its office count to five. It also grew its executive team. In January 2021, Wyndham hired Mike Ciambotti, a former Wells Fargo executive, to serve as its chief information officer. In November, the company brought on Melissa Smith, a former compliance executive at Key Bank, to serve as a senior vice president of risk and compliance. Lenders – now is the time to market yourself HousingWire CEO Clayton Collins and Wyndham Capital Mortgage SVP of Marketing Trey Rigdon discuss why loan officers should take control of their marketing efforts, even in today's seller's market. Presented by: Wyndham CapitalThe company has also made a recent push to expand its retail operations. Wyndham announced a plan in July 2021 to launch a retail division, and in August, hired former Citi executive Karen Mayfield to lead the national effort. Adding retail loan officers was a “natural progression,” Douglas said at the time. According to a company spokesperson, the company launched the division sometime in the fourth quarter of 2021. In recent months, two other lenders with consumer direct models—Better.com and Interfirst Mortgage—also announced loan officer layoffs. Analysts say lenders with consumer direct models, which tend to be refi-heavy and rely on call centers for intake, may struggle to find footing in a purchase market as rates climb and margins start to compress. However, despite the layoffs, the company has 17 active job openings that have been posted on LinkedIn within the past week. Most of the vacancies advertised are for originator positions, with over four years of experience. In the job postings, Wyndham notes that they are looking for mortgage professionals to "originate mortgage loans via telephone contact" and to make "outbound calls to company-provided warm leads." Wyndham, founded in 2001, has positioned itself as a fintech-focused mortgage lender. It has highlighted its proprietary software system and its use of augmented intelligence as factors that make it stand out from its competitors. The lender has also claimed that its closing timelines are 15% faster than the national average. The company originates loans in 47 states and Washington, D.C., and originates both conventional and Ginnie Mae-backed loans. The post Consumer direct mortgage lender lays off 35 LOs appeared first on HousingWire. |

| HW+ Member Spotlight: Joe Langner Posted: 07 Jan 2022 09:00 AM PST  This week's HW+ member spotlight features Joe Langner, CEO at ReverseVision. Langner has more than 30 years of senior leadership experience, driving growth at marquee mortgage technology and software companies. As a former executive vice president and chief sales officer at Ellie Mae, Langner helped execute the firm's initial public offering in 2011. His other leadership positions include serving as CEO at Blue Sage, president at PCLender and executive vice president and general manager at Sage. Langner is a thought leader and subject matter expert in the mortgage space, and regularly contributes and participates in industry panels, roundtables and conferences. Below, Langner answers questions about the housing industry: HousingWire: To start off, what is your current favorite HW+ article? Joe Langner: I'd like to say it's HW's acquisition of Reverse Mortgage Daily in June of this year, but technically it wasn't HW+ content; and, it's a bit self-serving with ReverseVision being exclusive to the reverse mortgage business! But in all seriousness, I don't have a particular favorite article. I read HW+ consistently and always gain significant value from the articles. HousingWire: What has been the most useful tech tool for you? Joe Langner: API's and interconnectivity between software solutions. HousingWire: When do you feel like a success in your job? Joe Langner: My customers' expectations have been exceeded and my team feels empowered, trusted and valued both internally and externally. HousingWire: What's the best piece of advice you've ever received? Joe Langner: "Put yourself in the other person's shoes." In college, I studied biochemistry/genetics and now I'm leading a mortgage software company. One key to my success in business is to ask a lot of questions and always listen to what your customers, peers, influencers, and teams say. I learned most of what I know in business by practicing this. When I ask questions for understanding and when I give answers to questions I've been asked, I always try to communicate from the perspective of my customer, peer, team member, etc. I've found that by looking at issues from the other person's perspective, it gives you the opportunity to get out of your own head and look at things from the other side of the equation. HousingWire: What keeps you up at night and why? Joe Langner: The prospect that our seniors could be placed in the wrong mortgage for their age and financial status, and that reverse mortgage products could and should have been offered, but they weren't because the lender that the borrower contacted does not offer them. We need to look out for our seniors and make sure they get what they need, and don't get what they don't need. HousingWire: What's one thing that people aren't paying attention to that you think they should be paying attention to? Joe Langner: Namely, it's the absence of reverse mortgage programs being in a lender's overall product offering. While the reverse process is a bit different from forward lending, it is a misconception that it's an arduous undertaking to get into that side of the business and that it takes a long time to get deals done. With the right technology and partners, however, it's simple to set up and begin offering reverse products to our seniors. Currently, there is a $7 trillion reverse mortgage market sitting dormant in untapped equity among seniors. That's a massive market opportunity that can add consistent revenue for years to come. To become an HW+ member, click here. For more information on HW+ benefits, click here. To view past issues of our HW+ exclusive HousingWire Magazine, go here. The post HW+ Member Spotlight: Joe Langner appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment