Mortgage – HousingWire |

- Will the 10-year yield send mortgage rates over 4%?

- Fannie Mae and NAR at odds over flood-risk disclosures

- Wells Fargo pays $12M for wrongly denying mortgage modifications

- Mortgage origination tech startup Vesta raises $30M

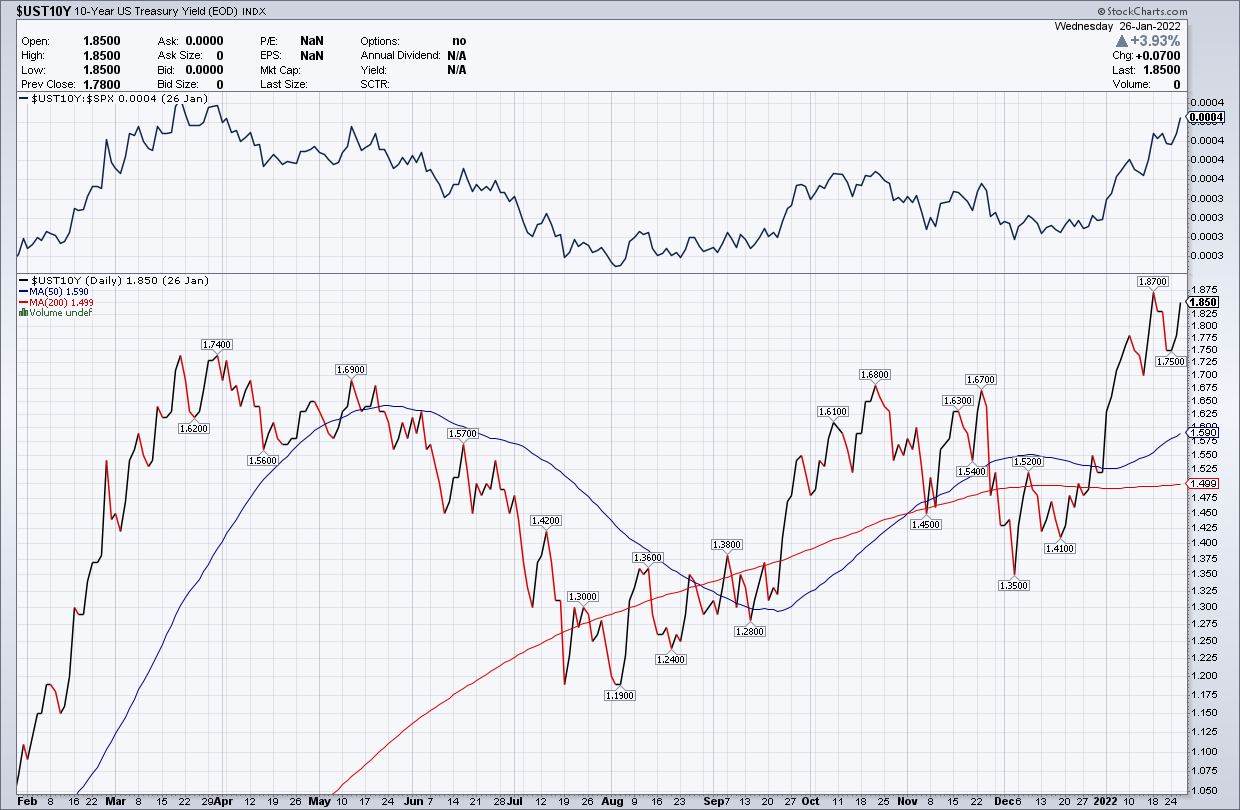

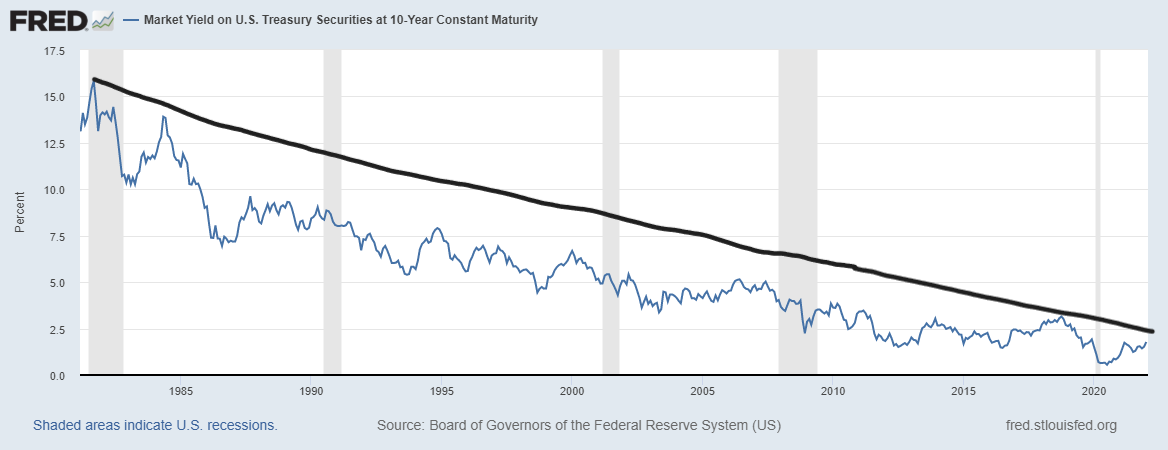

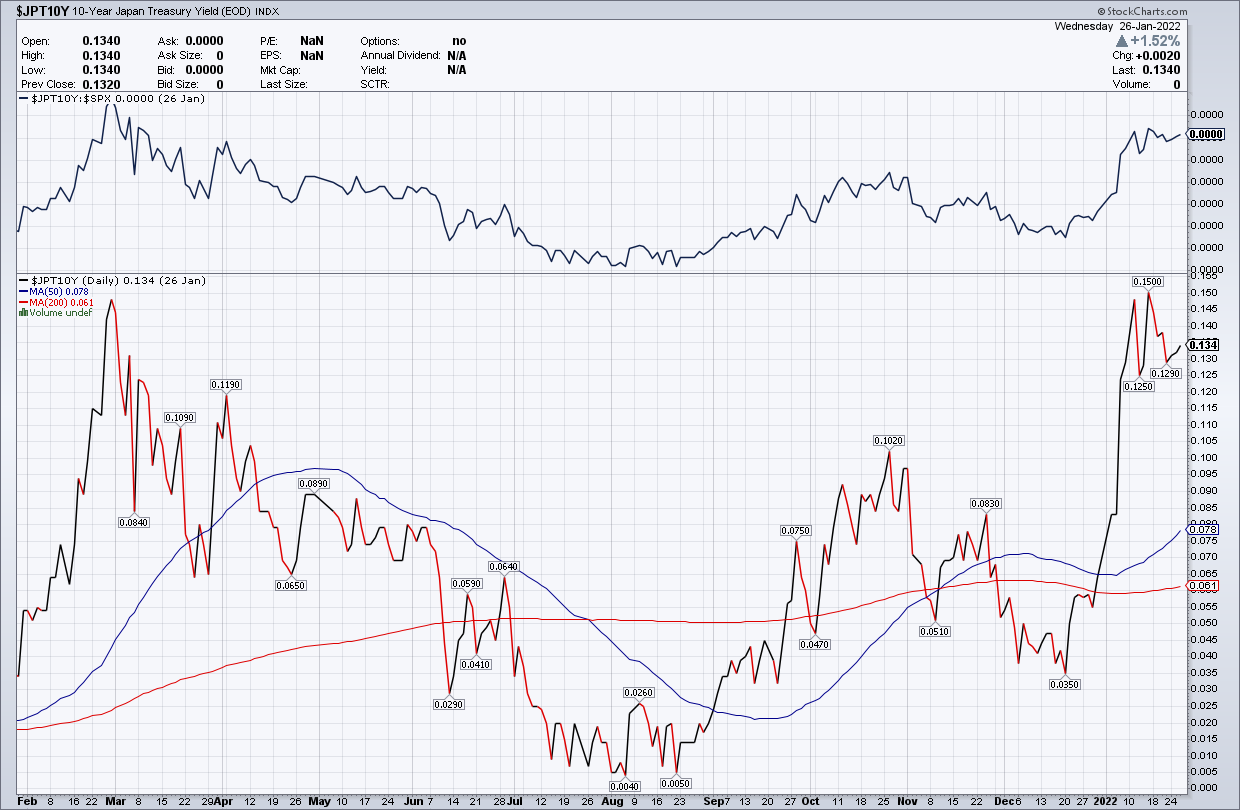

| Will the 10-year yield send mortgage rates over 4%? Posted: 27 Jan 2022 03:58 PM PST  I have been a happy camper lately, particularly with the rise of the 10-year yield as I am seeking balance in the housing market. I love these times in the market and the San Francisco 49ers are making an epic run in the playoffs, so what else can a person ask for? Other people might not be as happy as I am. I retired in 2020 from the mortgage business after 24 years, so I understand how some people who were floating their rate lock might not feel this way. Between the FOMC meeting and stock market volatility, there is a lot of angst about the market right now so I want to break down what’s happening with the 10-year yield and how that could affect mortgage rates. I am a bond market guy because, to the core, I am an economics person first, so my discussions are more about the 10-year yield and the economic cycle versus mortgage-backed securities. Let’s look at my 2022 forecast based on the 10-year yield. "For 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper-end range in mortgage rates is 3.375%-3.625%, and the lower-end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981." In the previous expansion, when I started to incorporate 10-year yield ranges as part of my forecast beginning in 2015, I always said the same thing up until it was apparent that COVID-19 was about to hit us: The 10-year yield would be in a range between 1.60%-3%. In 2018, we tested the higher-end range when the 10-year yield got to 3.25%. I remember it well as everyone thought mortgage rates and the bond market were headed higher. At a conference that day, I was scolded that I didn't know what I was talking about. Fifty economists surveyed by the Wall Street Journal all said rates would go higher, but my 2019 forecast spoke about a 10-year yield under 2%. This was based on the long-term downtrend not breaking, and I thought growth would slow, as it did. Now on to the second portion of the 2022 forecast: "We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don't support this." I know it seems like a crazy time with stocks falling and bond yields rising. However, if you ignore the noise, everything still looks about right. If our 10-year yields had risen well over 1.94% (3.50% plus) due to inflation and Germany and Japan weren't increasing, I would be having a different conversation today. However, that isn't the case. I understand some people’s confusion because inflation data should send yields much higher. However, that isn't happening and economic growth is booming. But, the economy’s growth rate can't sustain itself unless population growth takes off or productivity does. In time, things will moderate to a proper trend, and the supply shortage issues will be gone as demand gets back to normal and the world economies heal. What that means is that we will go back to being a country with slowing population growth in a world that has a lot of economies with slowing population growth. Now the question is: can yields take mortgage rates over 4%? The key will be Germany and Japan, so keep watching their yields. The longer we go without our 10-year breaking over 1.94%, the higher the risk that the bond market will rally and send yields — and mortgage rates — lower. With housing inventory hitting fresh new all-time lows, sub-4% mortgage rates combined with sub-4% unemployment rates are not what I want to see heading into the spring home-buying season. The post Will the 10-year yield send mortgage rates over 4%? appeared first on HousingWire. |

| Fannie Mae and NAR at odds over flood-risk disclosures Posted: 27 Jan 2022 01:44 PM PST  Two of the most powerful U.S. housing entities are at odds over the future of the federal government's cash-strapped flood insurance program. The National Association of Realtors, which represents real estate agents, brokerages and consumers, wants the Federal Emergency Management Agency to carve out a privacy law exception, and require that the history of a property's flood claims be disclosed to "buyers and renters, as well as owners before real estate transactions are completed," according to a letter NAR fired off to FEMA this week. But Fannie Mae, the government-sponsored entity that backstops a significant portion of the country's mortgages, does not seek an exception to the 1974 Federal Privacy Act. Instead, Fannie seeks, "continuing to protect the personal privacy of individual policyholders consistent with the Privacy Act," in a letter the GSE wrote to FEMA in January 2022. Fannie also wants FEMA and perhaps Congress to create uniform flood risk disclosure rules. NAR, meanwhile, no longer wants to see states excluded from the federal government's flood insurance program due to not meeting FEMA standards. The trade group wants states and localities to set their own rules. Sources close to NAR question if Fannie Mae truly understands how flood insurance works. They wonder if states might pull out of the federal plan entirely if faced with more onerous requirements. Meanwhile, Fannie Mae did not respond to requests for comment. The differences emerged as FEMA seeks public input on revisiting the National Flood Insurance Program, or NFIP, the federally administered program to make flood insurance and federal relief available to homeowners. NFIP has been around since 1968, and there have been periodic attempts to update it the last 20 years amid a fast-growing number of household claims. After Hurricane Sandy in 2012, Congress increased NFIP's borrowing limit to $30.5 billion, according to the Congressional Research Service. As of December, NFIP's borrowing authority had dwindled to $9.9 billion, per Congress's research arm, while still being on the hook for $2.9 billion in reinsurance payments. NFIP provides over five million policies, according to CRS, in jurisdictions that meet federal criteria on building, design standards, and risk index. Despite the NFIP servicing a significant chunk of homeowners, the program has struggled with its financial wherewithal, partially due to the fact that Congress requires NFIP to charge discounted premium rates to policyholders. A report published by the Government Accountability Office in July 2021, found that as of August 2020, FEMA's debt was $20.5 billion, despite Congress having canceled $16 billion in debt in October 2017. Both NAR and Fannie Mae seek a policy that requires more disclosure – especially amid a real estate or mortgage transaction – about a home's flood history and future risk assessment. But the key ideological difference is that Fannie Mae wants the federal government to establish laws mandating flood-risk disclosures at the time of the property sale. NAR, meanwhile, believes that state and local government should set requirements. As for mandatory disclosure, the trade group sees work around: Simply allow prospective homebuyers to see a home's Comprehensive Loss Underwriting Exchange, or CLUE report, which would require a Federal Privacy Act exception. The public comment period ends Thursday. Unclear is FEMA's timetable to adopt recommendations, but a spokesperson told HousingWire that FEMA will review all of the comments and publish a summary “in the future.” The post Fannie Mae and NAR at odds over flood-risk disclosures appeared first on HousingWire. |

| Wells Fargo pays $12M for wrongly denying mortgage modifications Posted: 27 Jan 2022 12:19 PM PST Wells Fargo agreed to pay $12 million to more than 1,800 mortgage borrowers to resolve a class action lawsuit that alleged the bank’s clients had loan modifications wrongfully denied due to calculation errors in the bank's system. A judge from the U.S. District Court for the Southern District of Ohio approved the settlement on Tuesday after a hearing between the parties. A spokesperson for Wells Fargo, the largest depository residential mortgage lender in the U.S., told HousingWire that the bank is “pleased to be able to put this lawsuit behind us” but had no more comments to add about the settlement. The deal will provide $9 million to the class members, with the remainder going to plaintiffs' attorneys, costs, service awards, and settlement expenses. The benefit distribute date is currently scheduled to occur on March 15. Plaintiffs Diane Hawkins and Ethan Ryder filed the class action in 2019. The lawsuit alleges that, between 2010 and 2018, Wells Fargo failed to detect errors in its automated system to determine whether consumers in default would be eligible for loan modifications with Fannie Mae or Freddie Mac, or under the U.S. Department of Treasury's Home Affordable Modification Program (HAMP). Also, the bank failed to audit the software for compliance with government requirements, allowing life-changing error to remain uncorrected for years. One caveat: the government provided a free tool for the bank, but Wells Fargo decided to use its own software, according to the lawsuit. Wells Fargo publicly acknowledged the calculation error in 2018, including the information in filings with the Securities and Exchange Commission (SEC). The bank estimated that approximately 625 customers were incorrectly denied a mortgage modification, and 400 of them were foreclosed. The bank set aside $8 million to be used to remediate the customers, but plaintiffs filed the lawsuit alleging breach of contract, fraudulent concealment, and intentional infliction of emotional distress. Wells Fargo denies plaintiffs' allegations, and the settlement document clarifies that it may not be used as an admission, or evidence, of the validity of the claims. In September, Wells Fargo was slapped with a $250 million civil penalty by the Office of the Comptroller of the Currency for “unsafe or unsound” practices pertaining t its home lending loss mitigation program. Specifically, the agency accused the bank of charging customers mortgage interest rate lock extension fees, even though some of the loan closings failed due to the bank's own volition. The bank recently entered into a three-year deferred prosecution agreement that required changes to Wells Fargo’s management and its board of directors. It also required a stronger compliance program. Last week, Wells Fargo appointed Derek Flowers as its new chief risk officer. The post Wells Fargo pays $12M for wrongly denying mortgage modifications appeared first on HousingWire. |

| Mortgage origination tech startup Vesta raises $30M Posted: 27 Jan 2022 08:06 AM PST San Francisco-based startup Vesta, which provides a software-as-a-service platform for mortgage loan originators, announced on Thursday that it raised $30 million through a Series A funding round. The new capital will be invested in an "aggressive" hiring plan and technology expansion. The round is led by the venture capital firm Andreessen Horowitz, with participation from new investor Zigg Capital and seed investors Conversion Capital and Bain Capital Ventures. Investors backing Vesta also include Index Ventures. In total, Vesta has raised $35 million since November 2020, when Mike Yu and Devon Yan, early employees at the cloud-based platform for banking products Blend, founded the startup. Vesta has a system of record for loan origination data and documentation; a workflow engine to orchestrate process among borrowers, loan officers, underwriters; and open APIs (application programming interface) for partners to build their own solutions. The platform supports approval, underwriting, closing, and funding of home loans. The company targets the $2.6 trillion mortgage loan origination market, according to the Mortgage Bankers Association (MBA) forecast for 2022. Mike Yu, Vesta’s founder and CEO, said that amidst the pandemic, first-time homeowners and refinancing demand went to all-time record highs, and the increased volume uncovered how "inflexible, antiquated, and painfully" the mortgage process can be. Mortgage Cadence Releases Next Generation Loan Origination Software Today, it's not just about creating the mortgage asset. It's about doing it faster and cheaper. With timelines expanding and cost-to-close still too high, if your LOS is not helping you manage your time and money, it's not doing its job and it's time to seek out a new solution. Presented by: Mortgage Cadence"Today, as the market contracts, this shift to digital-first loan origination will accelerate. Lenders are motivated more than ever to invest in technologies that open and speed up the process to better serve borrowers, improve margins, and unlock new services." According to Angela Strange, general partner at Andreessen Horowitz, all the players – banks, brokers, and title agents – agree that a new system is needed to orchestrate and standardize loan origination, but to date no one has successfully built it. "Vesta's team understands the depth of the problem and is technically adept to solve it." The post Mortgage origination tech startup Vesta raises $30M appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment