Mortgage – HousingWire |

- Staircase debuts AWS blockchain-backed tech to store, process mortgage data

- LoanLogics rolls out automated income calculation tool

- Why owning a home is the best hedge against inflation

- Profits for nonbanks shrink 44% in 2021

- Fannie Mae announces title insurance shake up

- Buyers rush to lock mortgages as rates move fast and furious

| Staircase debuts AWS blockchain-backed tech to store, process mortgage data Posted: 11 Apr 2022 02:11 PM PDT Mortgage tech startup Staircase this week launched a blockchain-backed digital infrastructure that it says enables lenders to safely store collected mortgage data while processing mortgages faster. Philadelphia, Pennsylvania-based Staircase rolled out Amazon Web Service blockchain-based “Staircase Persistence,” which it says helps companies manage data points used by their different customers by grouping data into sets, such as transactions, collections, and client accounts. Data stored through Staircase Persistence can later be used for data extraction, other mortgage processes, as well as translate data into different languages. "We collect data, we use blockchain to make each of those data points and data collections immutable,” Adam Kalamchi, Staircase CEO told HousingWire. "The final application is a subset of the total amount of data that has been collected. The data then is put into a final application that turns into a loan." The company hopes to tap into a market where "there hasn't been a simple way to store and access 'big data,'" according to Staircase. With the mortgage origination market forecast to consolidate this year, Kalamchi said its digital infrastructure will help clients save on expenses to capture and preserve data to compile the loan file or perform quality control on collected data. "Our target market is any mortgage data," said Kalamchi. "It's targeting anyone because what we enable is not only the full audit ability of a loan file with the full data bundle. Whether it's between a broker and lender, or a lender or a servicer, that data is something that everyone can leverage." Staircase, founded in 2020, raised $18 million in Series A funding the following year, led by Bessemer Venture Partners with participation from five ventures, including Avid Ventures and Clocktower Technology Ventures as well as angel investors. Sponsored Video Focused on providing automation for mortgage functions, Staircase provides an application programming interface platform that brings together parties involved in the mortgage origination process. Last month, the startup introduced Staircase Language, which enables any company in the mortgage industry to translate data into another language including the real estate finance industry's standards. "Having the data stored isn't as helpful if you can't translate the compiled data into a format that works natively, intuitively with your system," said Kalamchi. The post Staircase debuts AWS blockchain-backed tech to store, process mortgage data appeared first on HousingWire. |

| LoanLogics rolls out automated income calculation tool Posted: 11 Apr 2022 01:48 PM PDT LoanLogics this week rolled out LoanBeam Wage, a new automated tool that enables lenders to calculate borrower’s income quickly by using paper-based paystubs and W2s. The Jacksonville, Florida-based digital mortgage solutions provider combines machine learning with “layered optical character recognition technologies” to automatically extract and interpret income data in a paystub and W2 income documents without a lender’s human staff, the firm said in a release. “By automatically capturing income data from a borrower’s structured and unstructured documents, LoanBeam Wage empowers lenders to evaluate income early in the process, determine the need for verification of income and verification of employment, and make income calculation faster, less expensive, more accurate, and more reliable,” Roby Roberston, head of mortgage origination automation at LoanLogics, said in a statement. Paper and PDF documents, such as paystubs and W2 forms, are used to qualify borrower income on roughly 70% of all applications containing wages. The program is connected to a lender’s system of record and integrated into a lender’s automated workflows, which converts paper-based income verification into system-based automation. "While the majority of mortgage applications are qualified using wages, and some of this is certainly being automated through 'digital' income verification solutions, often not all borrower or co-borrowers' income can be accessed this way," said Roberston. Founded in 2005, the LoanLogics platform provides technology automation for mortgage document processing and data-driven audit software that improves efficiency, enhances transparency, streamlines commerce, and reduces risk. Lenders, are you prepared for upcoming changes from the IRS? The IRS extended the deadline to conform to their new 4506-C clean form requirements to October 1, 2022. Although lenders now have an additional seven months to abide by the updated conditions, several other major changes on the horizon will cause a seismic shift in how lenders and borrowers interact with and submit tax return verification requests. Presented by: CoreLogicTwo specific areas LoanLogics focused on in recent years include an on-demand document processing technology and enhanced automation for the Home Mortgage Disclosure Act reporting and generation of Loan Application Registers, which enable lenders to automate more than 90% of their HMDA review tasks. Private equity firm Sun Capital Partners acquired LoanLogics in 2021 for an undisclosed amount. The post LoanLogics rolls out automated income calculation tool appeared first on HousingWire. |

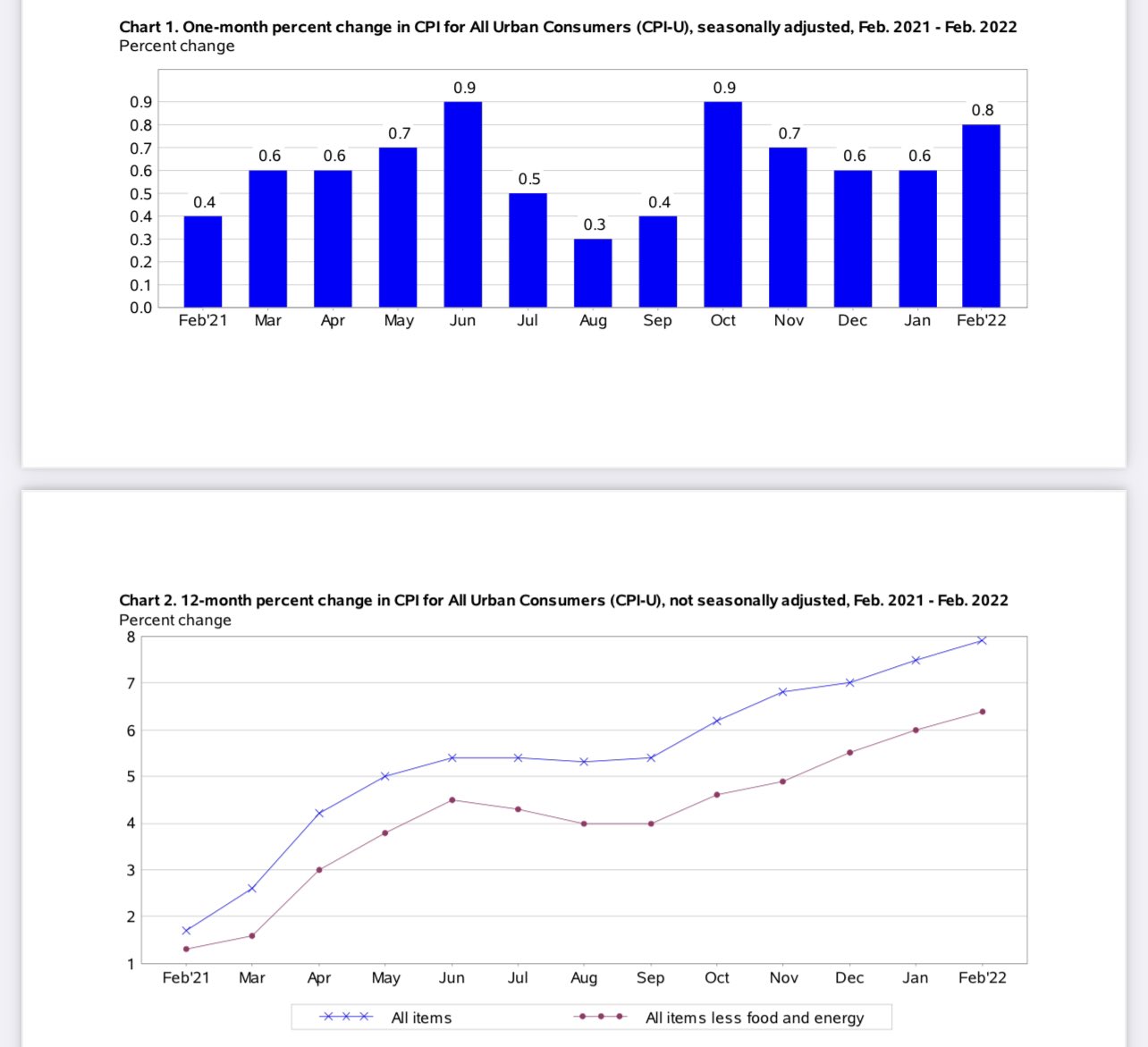

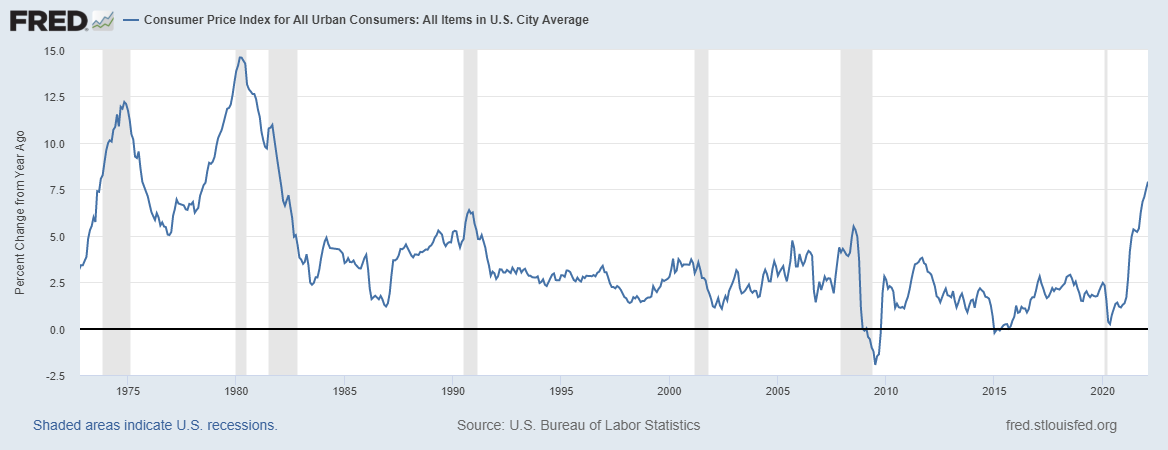

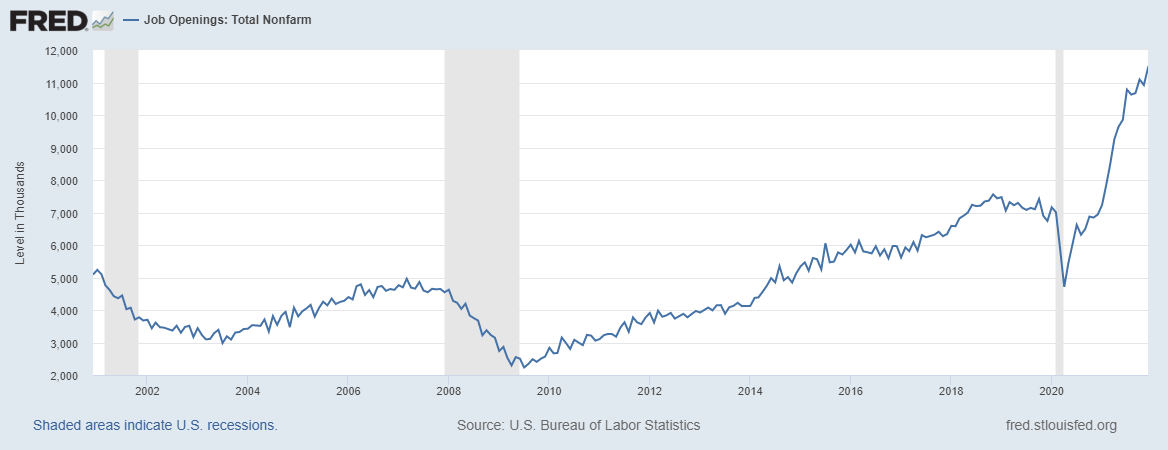

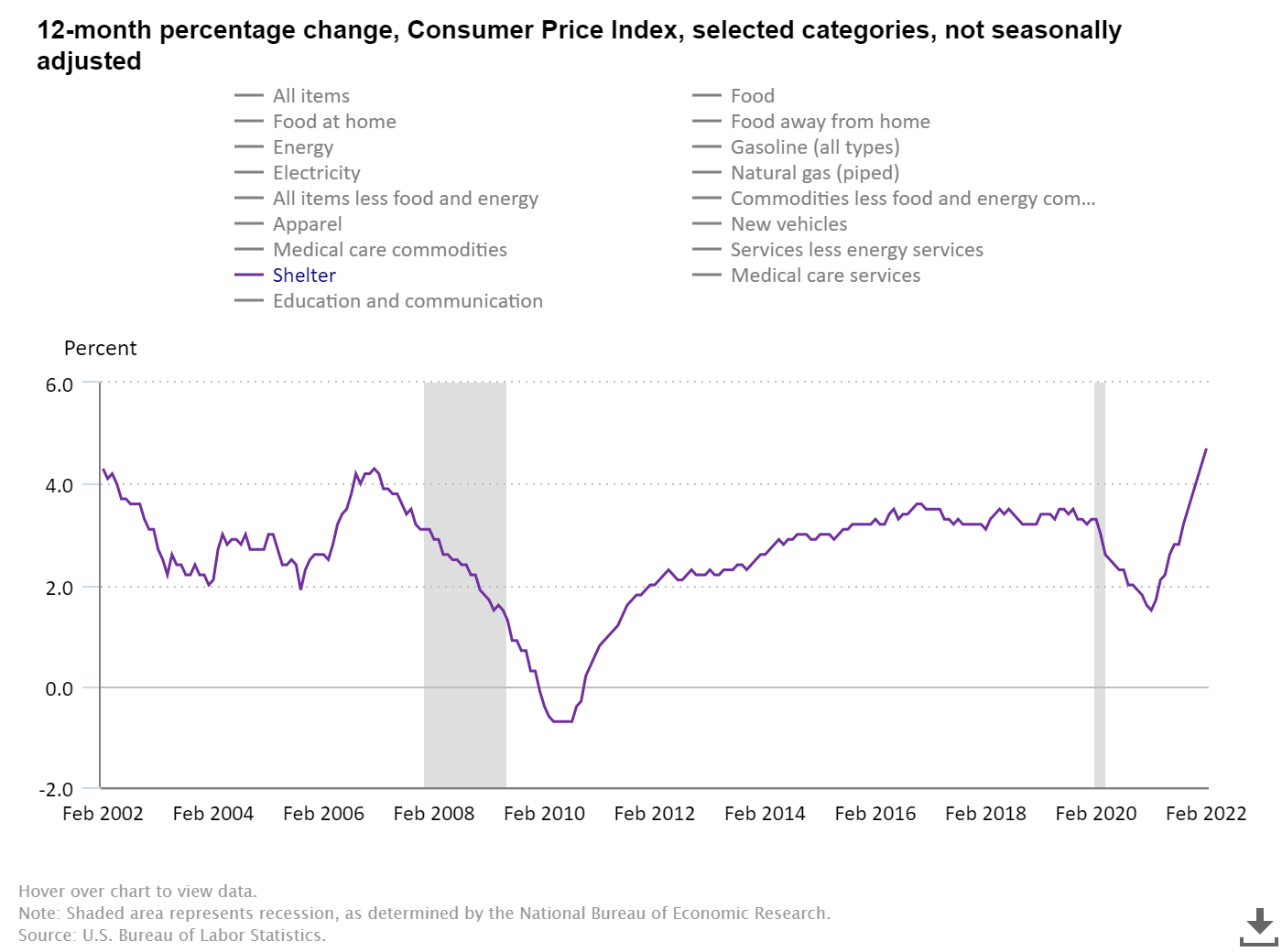

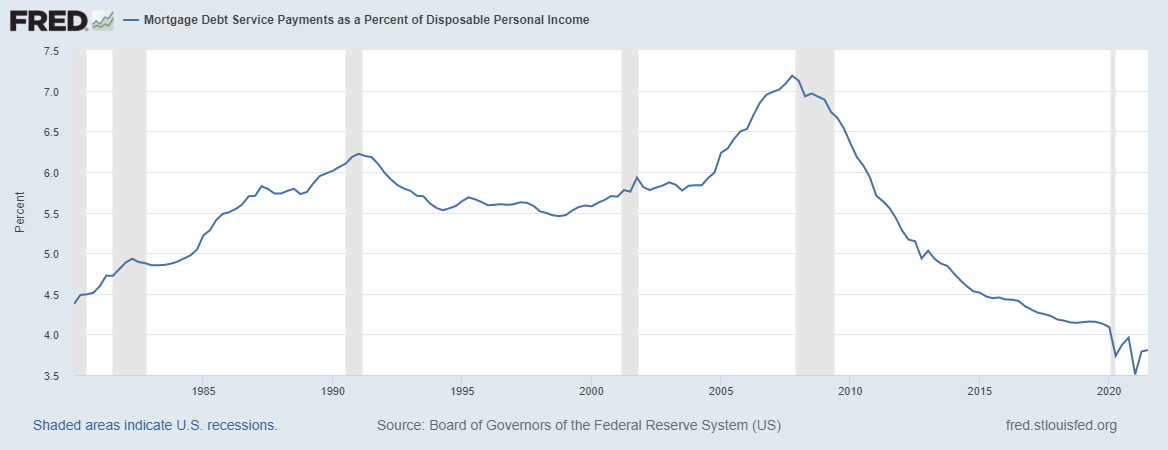

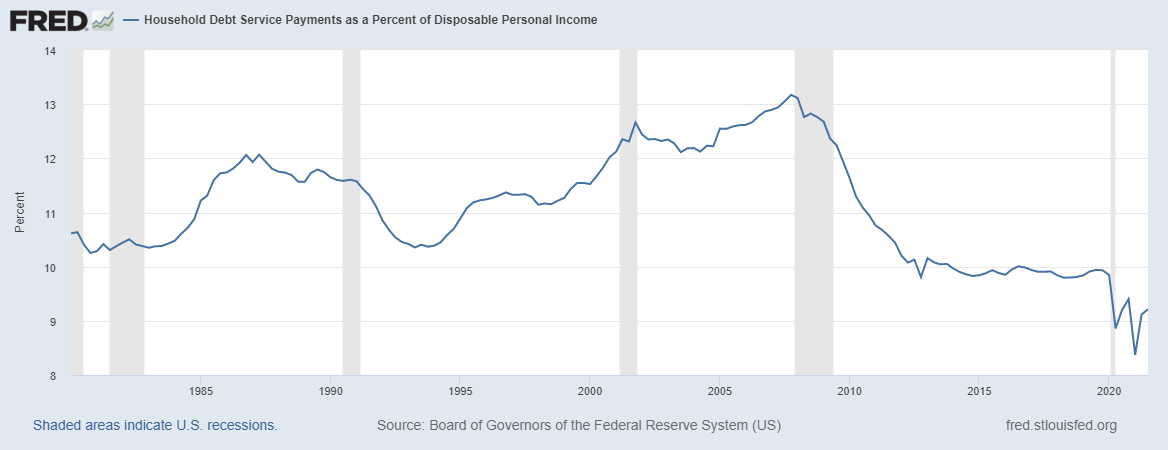

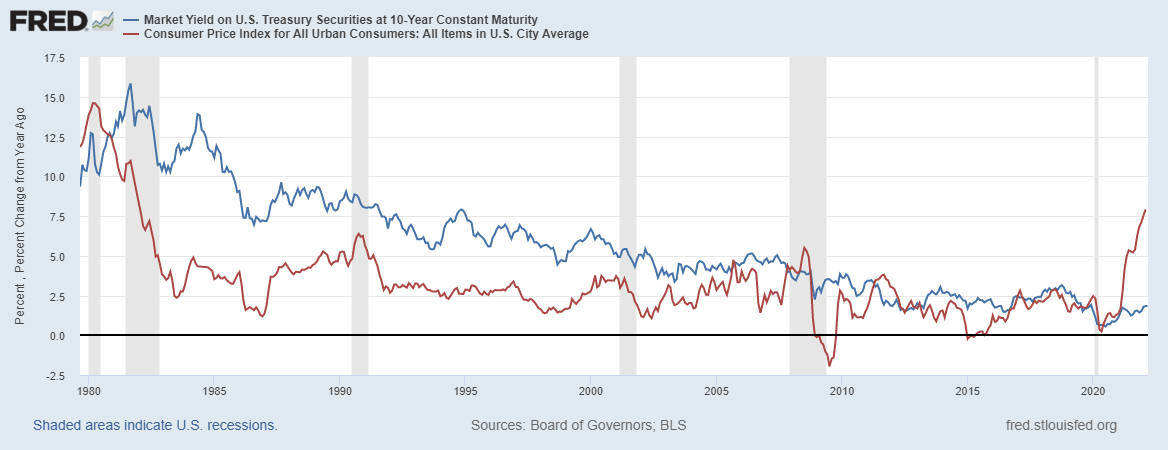

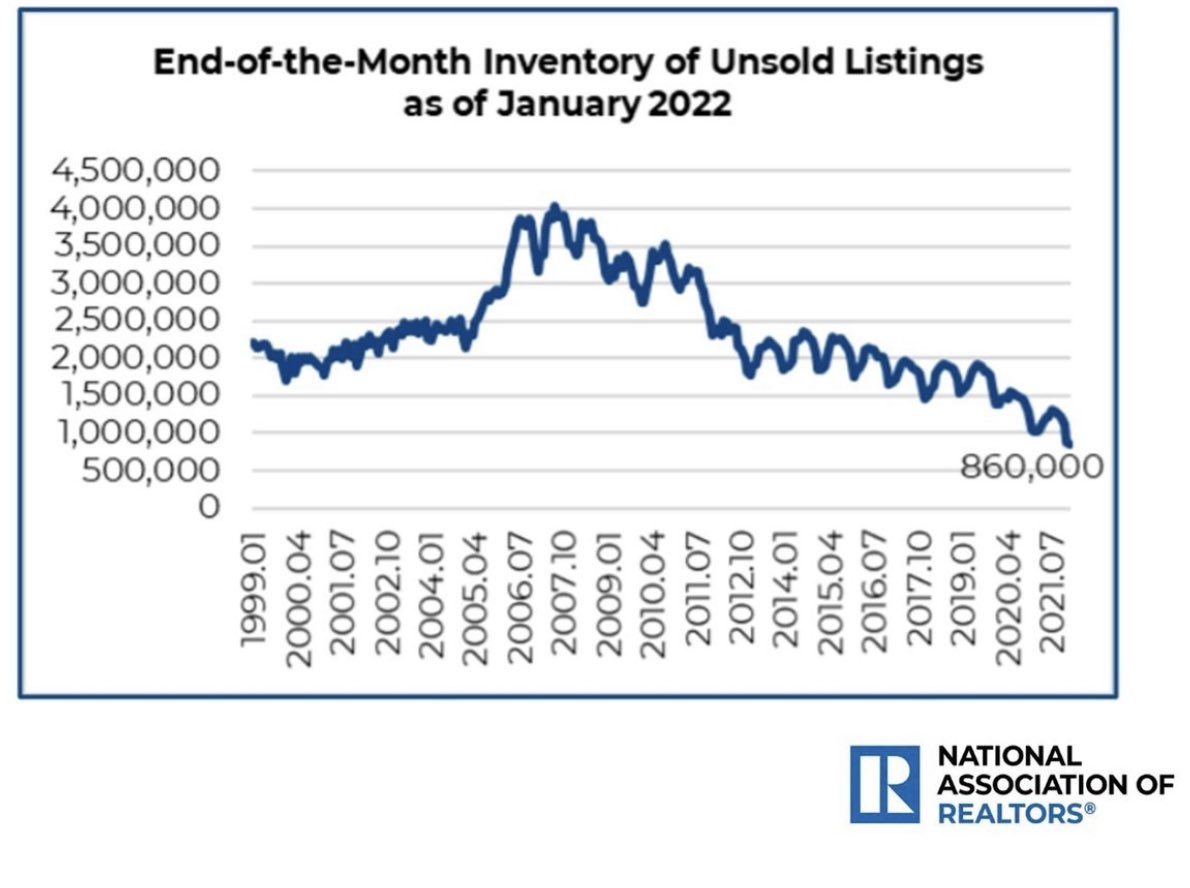

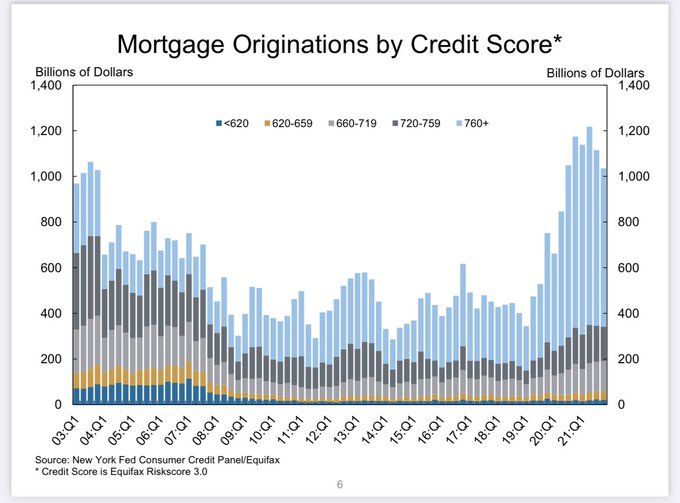

| Why owning a home is the best hedge against inflation Posted: 11 Apr 2022 11:34 AM PDT  On Thursday, the Bureau of Labor Statistics reported the same trend that all Americans have seen lately: the inflation rate of growth is rampant and doesn't show any sign of easing up due to the Russian Invasion of Ukraine. The Consumer Price Index for all Urban Consumers “increased 0.8 percent in February on a seasonally adjusted basis after rising 0.6 percent in January…. Over the last 12 months, the all items index increased 7.9 percent before seasonal adjustment.” During the COVID-19 recovery phase, I predicted that job openings would break over 10 million. This week, we just broke to an all-time high in job openings with near 11.3 million. What does that mean? Wage growth is going to kick up! Early in 2021, I told the Washington Post that rental inflation was about to take off and will take the consumer price index up faster and last longer. For me, it's always about demographics equal demand. Wages are rising, which means rent is about to get higher. Shelter inflation, the most significant component of CPI, is making its big push as people need to live somewhere and that shelter cost is a priority over most things. Rent inflation on a year-over-year basis has been extreme in certain cities, averaging over double digits. Now we can see that being a renter has been problematic because rent inflation is taking off, gas prices are taking off, and even though wages are up, the monthly items consumers spend money on have gone up in the most prominent fashion in recent history. In some cases, seeing this type of rental inflation can motivate consumers to buy a home because renting a home isn't as cheap as an option anymore. However, if you're a young renter and looking to buy a house a few years away, this makes savings for a downpayment much more of a problem. On top of all that, since inventory is at all-time lows, it's been harder and harder for first-time homebuyers to win some bids because they don't have more money to bring into the bidding process. As always, the marginal homebuyer gets hit with higher rates and higher home prices. Now, single household renters are paying more for their shelter, making the home-buying process more challenging financially. What can Americans do to hedge themselves against this? In reality, being a homeowner over the past decade has set consumers up nicely during this burst of inflation! How is that? Housing is the cost of shelter to your capacity to own the debt; it's not an investment. This has been my line for a decade now. Shelter cost is the primary driver of why you might want to own a home. The benefit of being a homeowner is that with a 30-year fixed mortgage rate, that mortgage payment is fixed for the life of the loan. Yes, your property tax or insurance might go up, but the mortgage payment is generally fixed. What has happened over the years is that American homeowners have refinanced time and time again to where their shelter cost got lower and lower as their wages rose over time. We can see this in the data. It has never looked better in history with the recent refinance boom we saw during the COVID-19 recovery, since mortgage debt is the most significant consumer debt we have in America. This would imply that household debt payments are at deficient levels as well. Which they are, as we can see below. In the last 10 years, the big difference is that we made American Mortgage Debt Great Again by making it dull. While wages rise, long-term fixed debt cost stays the same. It doesn't get any better than that. So how does this make being a homeowner a hedge against inflation? As the cost of living rises, wage growth has to match it, especially in a very tight labor market. Companies can no longer afford not to increase wages to lure employees to work and retain workers. Wages are going up! What doesn’t go up? Your mortgage payment as a homeowner. So, you can benefit from increasing wages while the most considerable payment stays the same. Why do I keep stressing that the homeownership benefit is a fixed low debt cost versus rising wages? While renters feel stressed about rental inflation and higher gas prices, homeowners never need to worry about their sub-3% mortgage rate increasing versus the 7.9% inflation rate of growth. Some people who are surprised by all this inflation we have had over the last year are now asking how the U.S. economy can keep pushing along. Not every household is the same. If you're a renter, your rents have gone up and that takes away from your disposable income and makes it harder to save for a downpayment as well. If you're a homeowner, the inflation cost isn't as bad, since you are benefiting from rising wages. That offsets the cost of living and you're safe in your home with that fixed product. This is great for a homeowner, but it contributes to a larger problem: The homeowner is doing a little too well and might have no motivation to move. Why would anyone want to give up a sub-3% mortgage rate and such a solid positive cash flow unless they’re buying something that will make their cost much cheaper? People move all the time for many different reasons. However, let’s be realistic here: housing inventory has been falling since 2014 and 2022 isn't looking any better. Also, investors that have bought homes for rental yield are enjoying the fact that wages are rising because it gives them a reason to raise the rent. In a low interest-rate environment, rental yield is a good source of income. We haven't had to deal with high inflation levels for many decades, and back in the late 1970s, mortgage rates were a lot higher, so it's not an apples-to-apples comparison anymore. This is a brand new ball game with how beneficial it has been to be a homeowner in America. It's not great news if you're worried about inventory getting low, as I am. I often make fun of my housing crash addict friends who have been wrong for a decade. However, now I tell them: you're implying educated homeowners who have excellent cash flow will, for some reason, sell their homes at a 40%, 50% or 60% discount just to rent a home at a higher cost than what would have been the case for many years. Human beings don't operate that way. However, there is a downside to homeowners having such good financials: they don't have a reason to give up a good thing. This is just another reason I keep saying this is the unhealthiest housing market post-2010. As you can see above with the FICO scores of homeowners, their cash flow looks great and against this burst of inflation, owning a home is a nice hedge. My concern has always been with inventory going lower and lower in the years 2020-2024. Currently, with homeowners looking so good on paper, we have entered uncharted territory where mortgage rates for current owners are at the lowest levels ever recorded in history, inventory levels are at the lowest levels ever and now the cost of living from a rise in inflation has taken off in an extreme way. The biggest problem I see here is that this can make the housing inventory situation much worse as homeowners now have even more incentive to never leave their homes. The post Why owning a home is the best hedge against inflation appeared first on HousingWire. |

| Profits for nonbanks shrink 44% in 2021 Posted: 11 Apr 2022 11:22 AM PDT Nonbanks and mortgage subsidiaries of chartered banks saw a big dip in profitability in 2021 amid rising interest rates, lower refinance originations, and higher expenses. In 2022 and beyond, industry observers believe it will only get worse. Net gains in 2021 declined to $2,339 on each loan originated, compared to a record $4,202 in the previous year, according to a report published by the Mortgage Bankers Association (MBA) on Monday. The data, compiled from 273 firms, shows that 96% of the firms posted a pre-tax net financial profit last year, down from 99% in the previous year. The average production profit went from 157 basis points in 2020, a record high, to 82 basis points in 2021. From 2008 through 2021, the average annual production profit was 60 basis points, or $1,456 per loan. Marina Walsh, vice president of industry analysis at the MBA, said in a statement that 2021 was another stellar year, with production profits well above average, however down 75 bps from the record-setting 2020. "Performance in the second half of 2021 declined relative to the first half of the year, which is an indication of where market conditions are heading in 2022." The report shows that average production volume came in at $4.9 billion per company last year, an increase from $4.5 billion in 2020. Volume count per company averaged 16,590 loans, up from the 16,198 loans made the previous year. The average loan balance for first mortgages reached a study-high $298,324 in 2021, compared to $278,725 in 2020, the largest single-year increase since the report started in 2008. 3 questions lenders should ask before implementing non-QM With refinance volumes anticipated to decrease by 62% this year and many originators experiencing layoffs, lenders are looking for a way to diversify their offerings with non-QM products and gain new business in order to maintain profits. Presented by: Acra LendingThe total mortgage production revenue dipped to 382 bps, down from 434 bps in 2020, the MBA said. On a per-loan basis, production revenue also took a hit, declining to $11,003 in 2021 compared to $11,780 in 2020. Meanwhile, per-loan production expenses have continued climbing and now hover at $8,664 per loan, compared to $7,578 in the prior year. This is the highest level since the inception of the report in 2008, according to Walsh. Personnel expenses for sales, fulfillment and production support functions also rose, climbing to an average of $5,971 per loan, up from $5,272 per loan in 2020, further eating into mortgage profits. Productivity was 2.5 loans per employee per month in 2021, compared to 3.3 loans in the previous year. Servicing net financial income went from a loss of $176 per loan in 2020 to a gain of $261 per loan in 2021. Servicing operations benefited from slower prepayments and low delinquencies that helped boost mortgage servicing rights (MSR) valuations. As a further indicator that the market is shifting from refis to purchase, the reported purchase share of total originations was at 46% in 2021, down from 55% in 2020. The trade group estimates that the cumulative purchase share for the mortgage industry went from 63% to 57% in the same period. In 2022 and beyond, Walsh said more difficult times are expected amid upward pressure on rates, which will diminish rate-term refinance volume. Also, housing inventory shortages pose challenges for purchase originations. "Staying profitable will require prudent cost management, as well as more reliance on servicing operations to serve as a hedge against production declines." The post Profits for nonbanks shrink 44% in 2021 appeared first on HousingWire. |

| Fannie Mae announces title insurance shake up Posted: 11 Apr 2022 10:34 AM PDT In a selling guide announcement released last week, Fannie Mae announced that it would be accepting written opinion letters from an attorney in lieu of a title insurance policy "in limited circumstances." According to the announcement, lenders "must ensure the loan is covered by either a title policy issued by an acceptable insurer (including any required endorsements) or a title opinion letter issued by an attorney." For an attorney opinion letter (AOL) to be approved by Fannie Mae, it must come from an attorney who is properly licensed and has malpractice insurance covering title opinions "in an amount commonly prevailing in the jurisdiction." In addition, letters must be addressed to the lender and all successors-in-interest, be commonly accepted in the property's jurisdiction, provide gap coverage for the duration between closing and recordation, and include certain other information. The AOL must also list "all other liens and the states in which they are subordinate," and "state the title condition of the property is acceptable and the mortgage constitutes a lien of the required priority on a fee simple estate in the property." If a lender receives an AOL in lieu of a title insurance policy, the lender must report Special Feature Code 155 when delivering the loan. In response to a request for comment on this announcement, the American Land Title Association wrote in an email: "We currently are reviewing this announcement, and, as always, continue to engage with the GSEs and our lender partners on the vital role our industry’s products and services play in a well-functioning housing finance market that serves the needs of a broad array of American homebuyers." Fannie Mae did not return a request for comment. RON is here to stay – Here’s what you need to know From understanding the importance of RON in the title industry and discovering the potential business benefits to learning how you can start offering RON closings to your clients, here's the need-to-know info to get started. Presented by: SoftProSo far, at least one company Voxtur Analytics has responded to this announcement by releasing a product that it says will be a "fully compliant alternative" to title insurance. According to Voxtur's annoucement, the AOL product provides lenders with an attorney's title opinion letter backed by transactional liability insurance "that follows the loan into the secondary market." Voxtur said that the product will be offered in select states before being rolled out nationwide. The company also claims that in some markets, the savings generated by using Voxtur's AOL product instead of a traditional title insurance policy, could save consumers up to an "entire mortgage payment." "Fannie Mae has identified closing costs as a barrier to homeownership,” Jim Albertelli, the CEO of Voxtur said in a statement. This is not the first time a firm has attempted to create an alternative to title insurance. In 2003, Radian attempted to launch a title insurance alternative called Radian Lien Protection Policy. However, after a California judge ruled that this product was title insurance, the mortgage and real estate services provider decided to change tactics and purchased its own title insurance underwriter. The post Fannie Mae announces title insurance shake up appeared first on HousingWire. |

| Buyers rush to lock mortgages as rates move fast and furious Posted: 11 Apr 2022 07:01 AM PDT Mortgage origination activity rose last month despite rapidly rising mortgage rates as prospective buyers sought to lock in their loans. Overall origination activity jumped 19% in March from the previous month, led by a 31% increase in purchase loan locks, according to the monthly Originations Market Monitor report from Black Knight. While cash-out refinance activity, which has been somewhat insulated due to strengthening home values, rose a mere 1.6% in March from February, rate-term refi originations fell 15.4% during the same period. Despite seeing the fastest one-month 30-year mortgage rate rise in nearly 13 years, an increase in purchase lock volume was "likely as prospective buyers moved to lock in their loans before rates climbed any higher," Scott Happ, president of Black Knight's Optimal Blue division, said in a statement. The 30-year mortgage rate rose 70 basis points to finish March at 4.79% to mark the highest level in more than three years, according to the Optimal Blue Mortgage Market Indices daily interest rate tracker. In the face of rapidly climbing mortgage rates, refinance comprised 28% of the mortgage market last month, the lowest level since November 2018. As home prices surged in the sellers' market, the average loan rose by more than 23% to just under $361,000 in March from February. Home prices across the country rose 20% year-over-year in February, marking 12 months of consecutive double-digit gains, according to CoreLogic. "In turn, non-conforming products, including both jumbos and loans with expanded guidelines, continued to take market share from conforming loans and accounted for a full 18% of the month's lock activity," said Happ. Creating a profitable and differentiated digital mortgage experience This white paper will cover how digitizing the whole end-to-end mortgage origination process improves customer satisfaction, builds trust with users and results in a more profitable loan fulfillment process. Presented by: Stewart TitleConforming loans comprise about 61% of last month's lock activity, a decline of 686 basis points from a year ago. The highest rate lock volume came from the Los Angeles-Long Beach-Anaheim, California region, where 38% of the country's refis were done last month. The New York, Newark, Jersey City region had the second highest lock volume rate at 4.3% and the Washington, Arlington, Alexandria trailed at 3.9%. The post Buyers rush to lock mortgages as rates move fast and furious appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment