Mortgage – HousingWire |

- Carrington looks to attract brokers with new technology

- Even with blow-out jobs report, mortgage rates still falling

- Longbridge acquisition a positive sign for the reverse mortgage industry

- Fannie Mae transfers $771 million in credit risk to private insurers

- Union Home Mortgage promotes three to retail leadership positions

| Carrington looks to attract brokers with new technology Posted: 04 Mar 2022 02:35 PM PST California-based nonbank lender Carrington Mortgage Services has invested in boosting the growth of its wholesale channel, with the latest announcements including a new loan processing technology and plans to increase the sales team. The attention to broker shops comes at a moment in the mortgage industry when the retail channel is losing origination volume, particularly refinance volume, due to higher rates. “We put a lot of effort and energy into developing a program to help brokers grow. And we are hoping that with this program, we will be able to attract more brokers to work with us,” Jeff Gillis, executive vice president for operations, strategy, and governance at CMS, told HousingWire. CMS focuses on government – Federal Housing Administration, Department of Veteran Affairs, and U.S. Department of Agriculture – and non-qualified mortgages (non-QM) loans. In February, the company announced a technology called ProcessIQ to assist brokers in processing these complicated and time-sensitive loans through their pipelines more easily. The ProcessIQ team handles logistics and works directly with the borrower, but brokers manage all licensable activities. CMS said the technology costs $200, added to the underwriting fee, which is $699 in most states for government loans and $750 for non-QM. According to Gillis, third-party processing companies charge $1,000 for the same service. The technology is available only for full-doc government and non-QM loans. “Many brokers don’t have the staff or the processing expertise to devote to the more time-intensive government and non-QM loans. Sometimes, they have to turn down these loans, or put them on the back burner, to focus their employees on conforming loans that are a little bit easier and faster to originate,” Gillis explained. To support the wholesale channel, the company is also increasing its salesforce. CMS has 70 account executives and expects to reach 200 over this year. The mortgage lender is attracting professionals from the industry and developing its account executives and loan officers in-house, selecting people without experience in the mortgage industry. Gillis said the wholesale channel represents about 40% of its origination volume, but the company goal is to increase the share by building lasting partnerships with brokers. “If we grow retail and wholesale, it’s a win-win. But certainly, I think that there’s an opportunity for us to grow our footprint on the wholesale side. I’d love to be at 50-50% or maybe even 60-40%.” According to Inside Mortgage Finance, CMS is the 24th-largest mortgage servicer in the country. In 2021, the company’s servicing portfolio increased 6.8% compared to the previous year, to $68 billion. Origination data is not available. The company targets underserved borrowers, such as those with lower credit scores, higher debt ratios, or who are self-employed. Gillis believes these borrowers were left behind during the refi boom but will gain attention from brokers and other lenders in the current competitive environment. “We expect to see some lenders jump into our space a bit,” he said. Gillis said he expects the non-QM market to double in 2021, to $50 billion in origination volume. The post Carrington looks to attract brokers with new technology appeared first on HousingWire. |

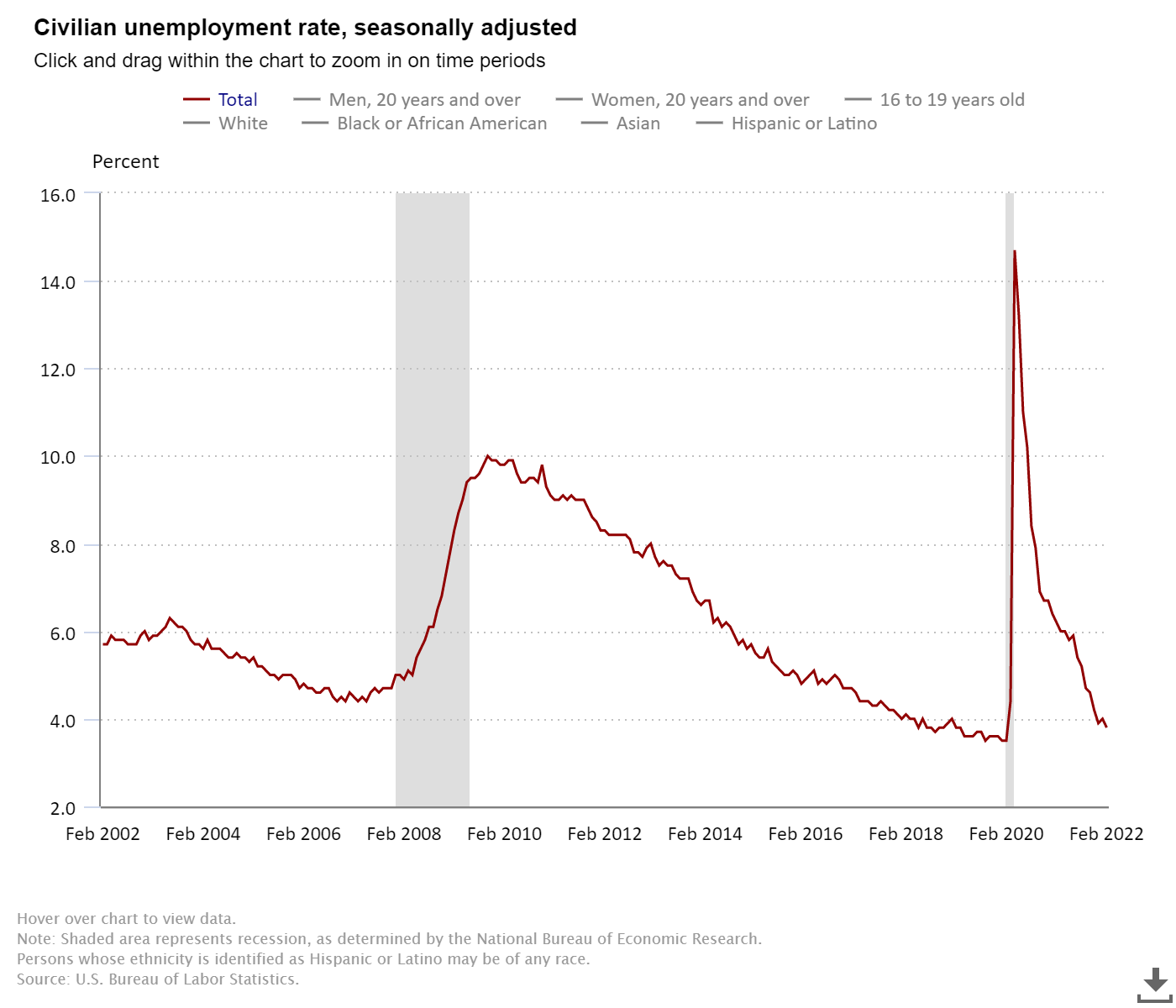

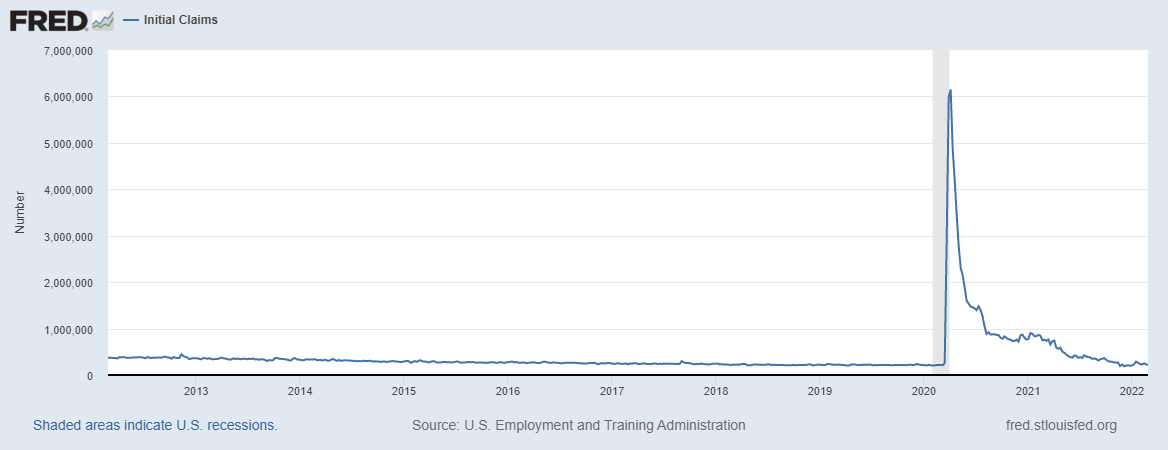

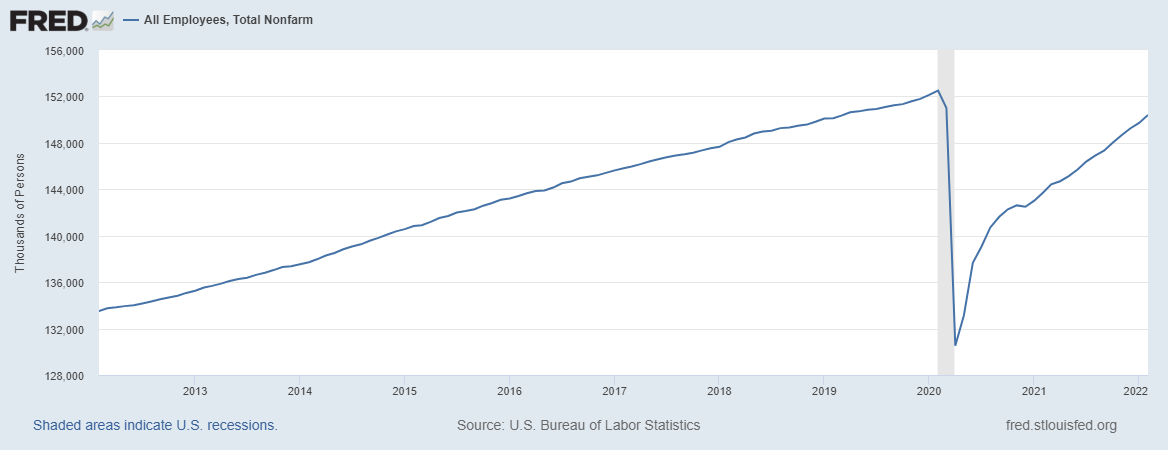

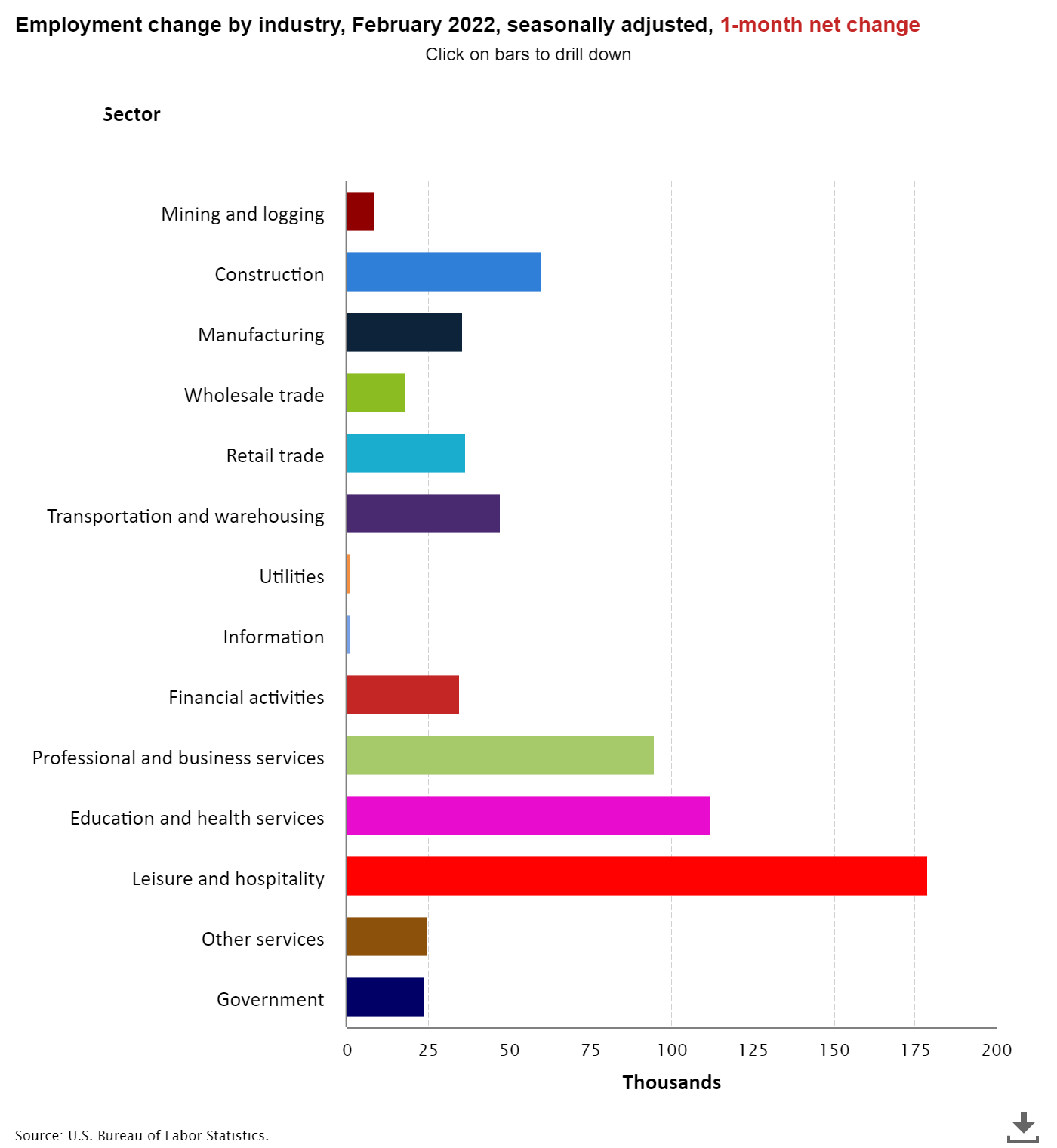

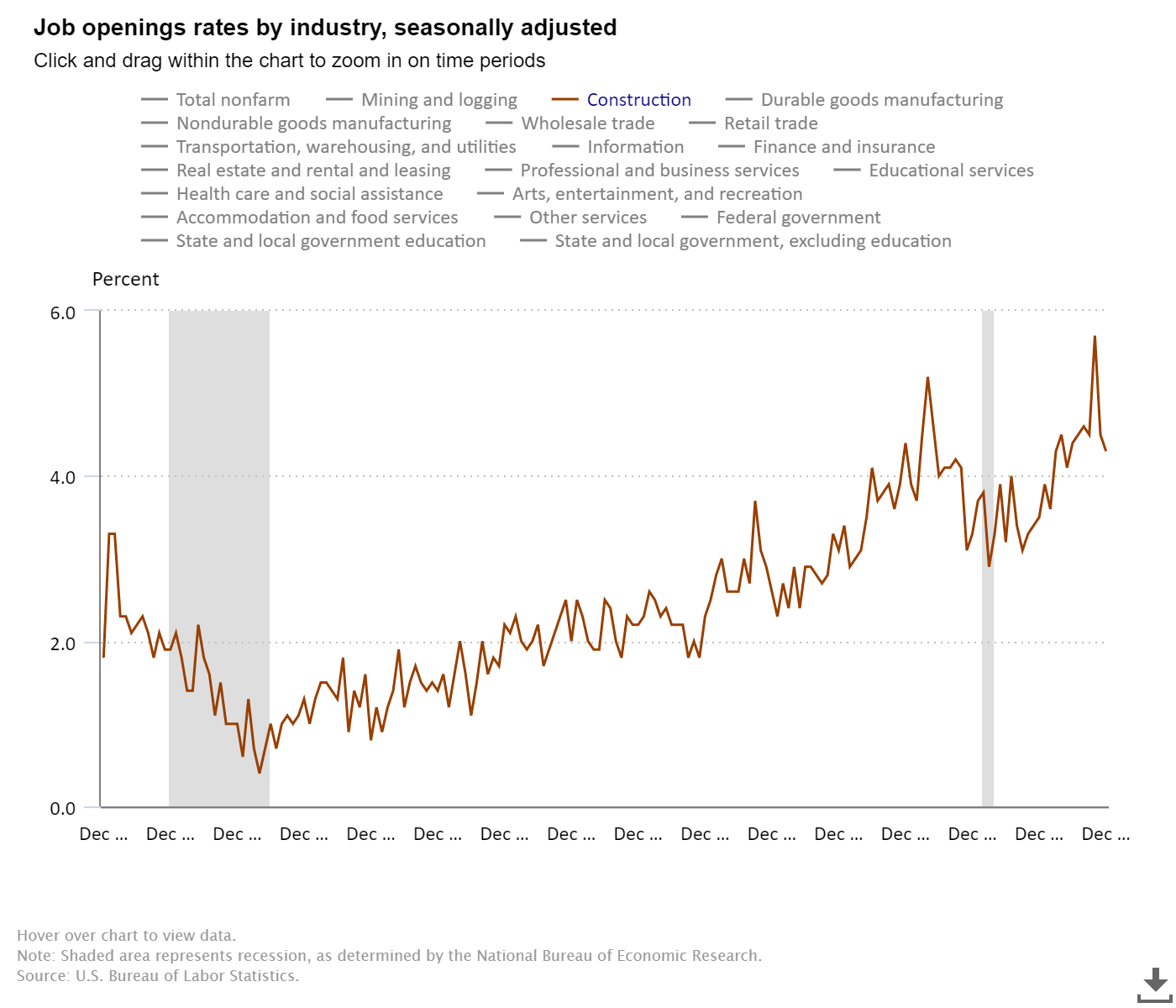

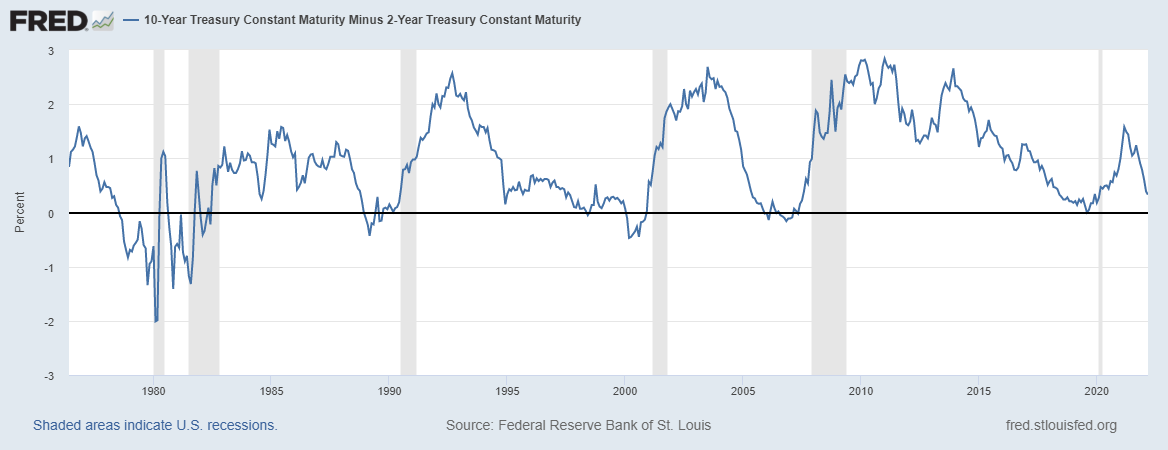

| Even with blow-out jobs report, mortgage rates still falling Posted: 04 Mar 2022 12:36 PM PST  Today, the Bureau of Labor Statistics reported that the United States Of America created 678,000 jobs in February. We also had 92,000 in positive revisions, and this report was a beat of estimates coming off a strong January report as well. The U.S unemployment rate stands at 3.8%, and we are getting closer and closer to my September 2022 forecast of getting all the jobs back that we lost due to COVID-19. During this epic recovery, which started on April 7, 2020, I was very adamant on Twitter that job openings would hit 10 million soon. Today, job openings are now trending near 11 million. As you see from the chart below, the labor market dynamics from the end of the great financial crisis, where job openings were just a tad over 2 million, is much different today. People forget that we had near 7 million job openings before COVID-19 hit us. The trend was always your friend with this data line that many people often ignore. Jobless claims data looks solid. As the baby boomers retire, we need labor to replace them and grow jobs. —Feb 2020: 152,553,000 jobs That leaves us with 2,163,000 jobs left to make up with seven months to go, which means we need to average adding 309,000 jobs per month. The unemployment rate currently stands at 3.8%.

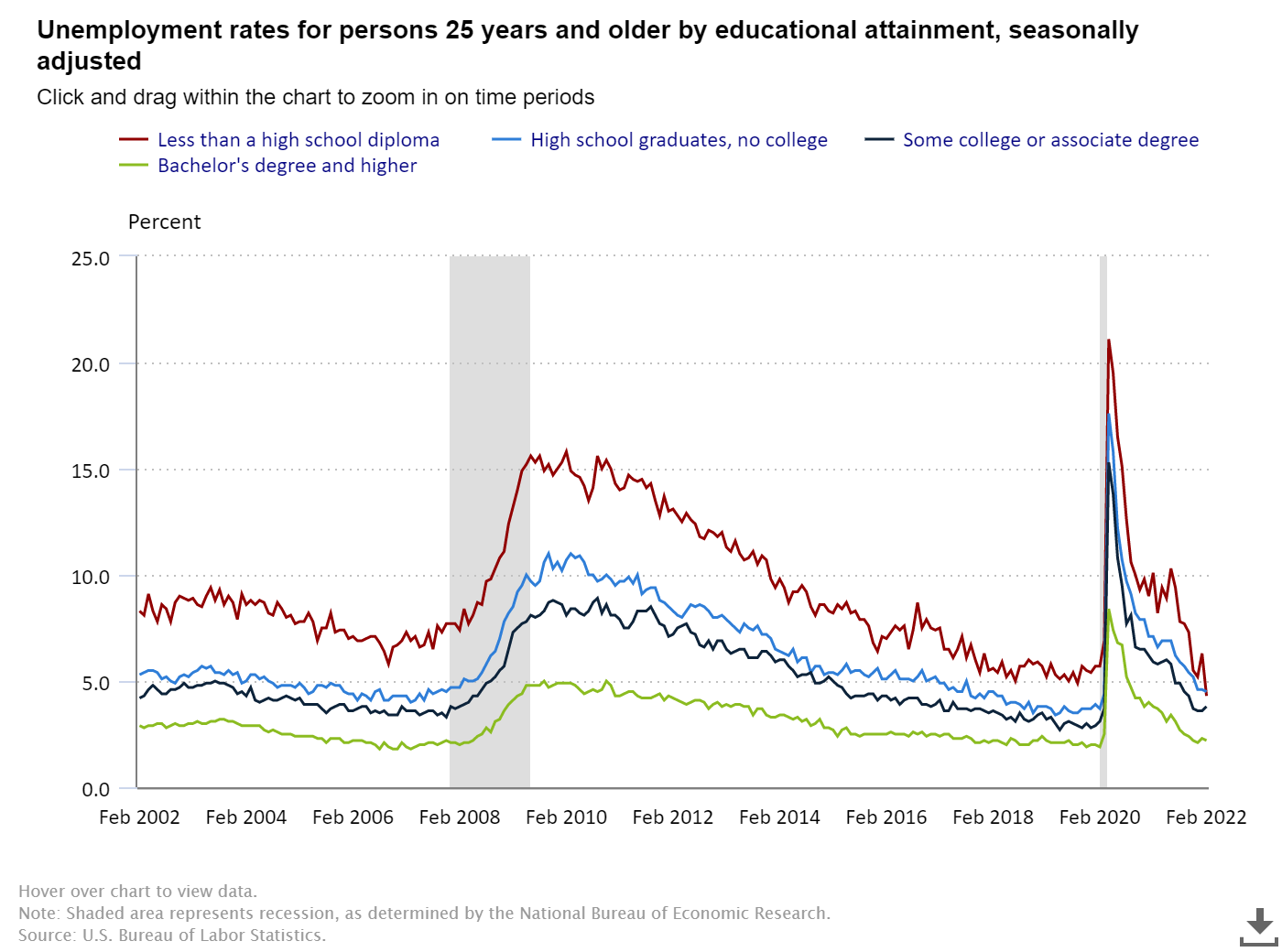

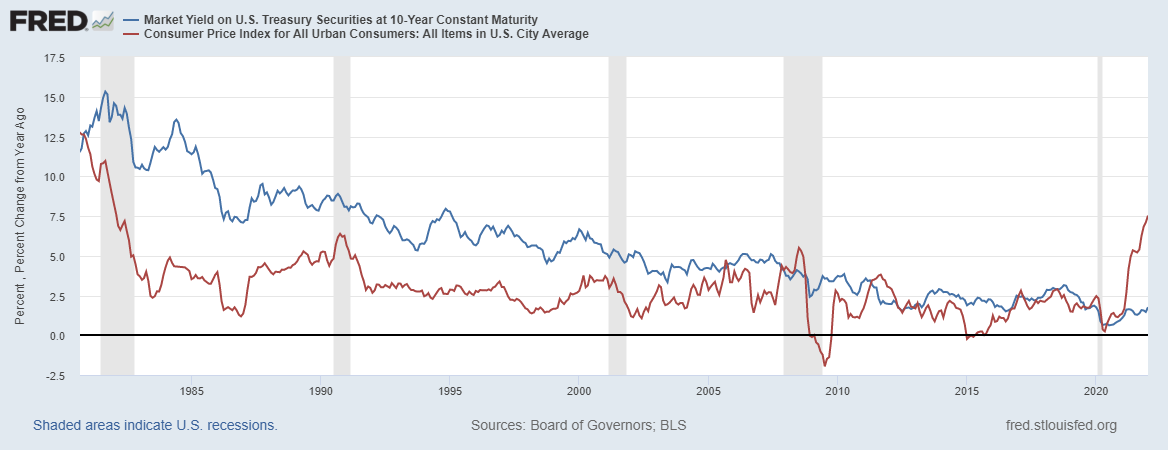

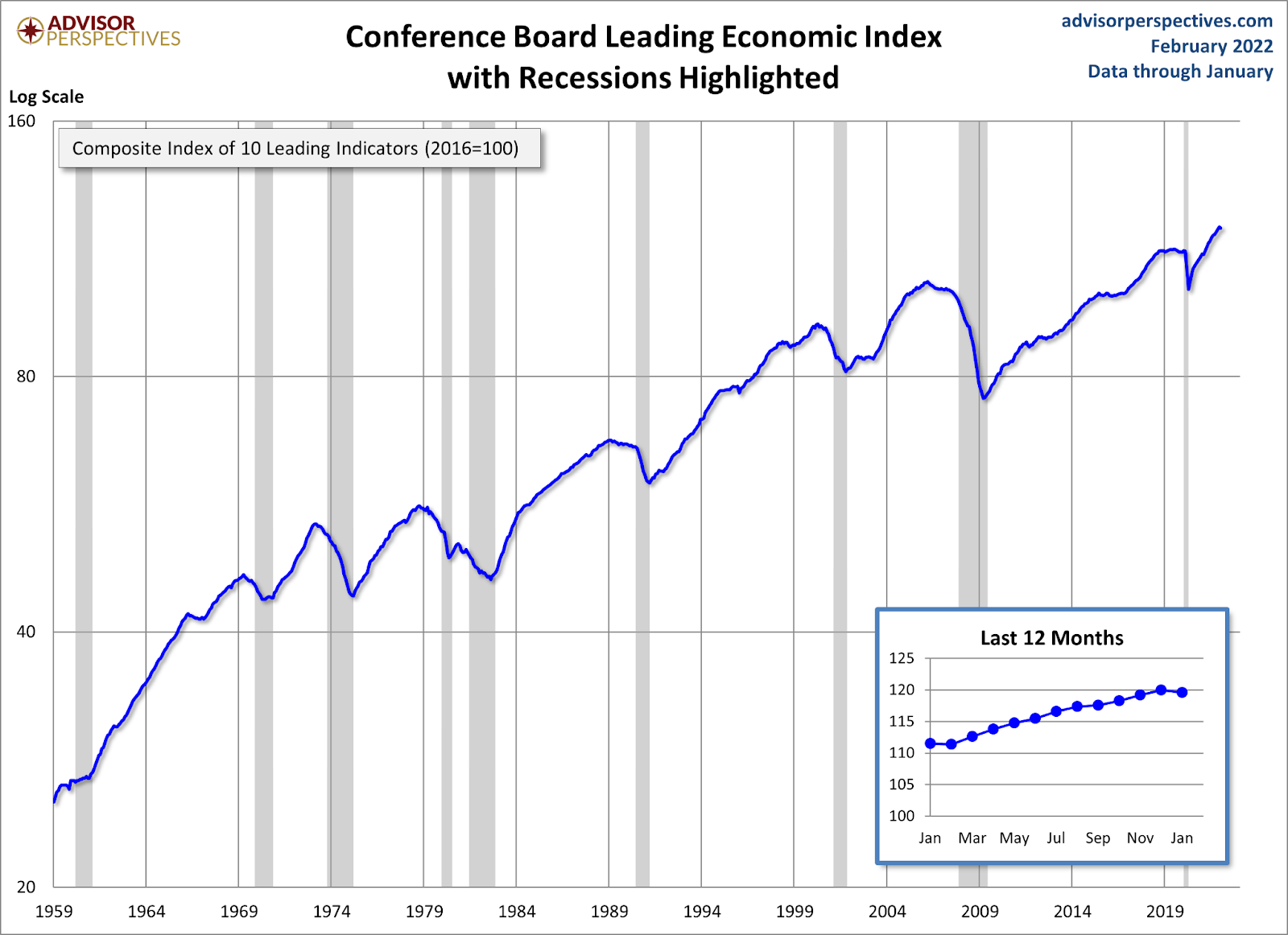

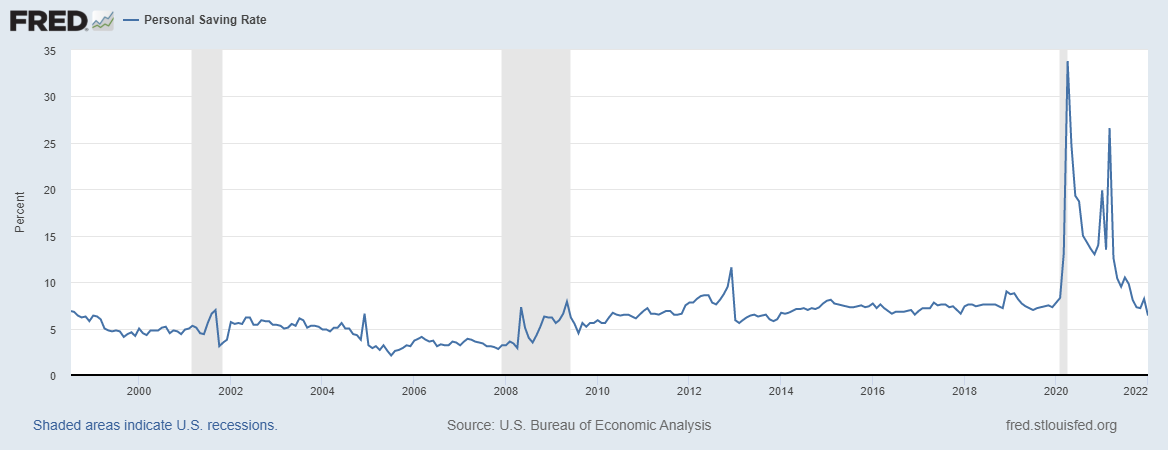

Education and employment Most Americans have always been working, even if they're not college-educated. The labor force with the least educational attainment tends to have a higher unemployment rate. I started the hashtag A Tighter Labor Market Is A Good Thing to remind everyone that the economy runs hot when we have a tighter labor market. We want to see the kind of unemployment rates that college-educated people have spread to everyone because we have tons of jobs that don't need a college education. Here is a breakdown of the unemployment rate and educational attainment for those 25 years and older: —Less than a high school diploma: 4.3%. The 10-year yield and mortgage rates My 2022 forecast said: For 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper end range in mortgage rates is 3.375%-3.625% and the lower end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981. We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don't support this. We have seen mortgage rates fall recently with the moves lower in the 10-year yield. If economic growth gets weaker toward the second half of 2022, it will be tough to have the 10-year yield getting above 1.94% and staying above that level. As you can see now, global yields need to rise for this to happen. Now for an economic update. Some of the economic data has been cooling off as expected, but staying firm. We can't replicate the same economic growth coming out of COVID-19. Eventually, we get back to our normal slow but steady economic growth patterns. Economics is demographics and productivity, and population growth is slowing here in the U.S., and productivity growth hasn't been strong for a while now. We have limits to what we can do here in the U.S. The leading economic index has had an epic recovery from the lows of April. However, last month it didn't show any growth. When this data line falls four to six months, a recession red flag is raised. We aren't there yet, but I am keeping an eye on this. Americans’ personal savings rate and disposable income are healthy enough to keep the expansion going! Even though the disaster relief has faded from the economic discussion, both these levels are good to go as employment has picked up a lot from the COVID-19 lows with wage growth. We have to remember, households have more cash, more net wealth, and have refinanced their mortgages to have lower payments. Once the Fed raises rates, the second recession red flag will be presented. This will most likely happen this month. The third recession red flag is getting very close; the 2/10s are getting very close to inverting. I have been on an inverted yield curve watch since Thanksgiving 2021, and now it's almost here. Typically we see an inverted curve before every recession. This red flag is very complicated, and once it is raised, I will go into more detail on how I look at this. My job is to show you the progress of the economic expansion into the next recession and out — over and over again. Each economic expansion is unique, and with the Russian Invasion and massive price increases on oil and wheat, I have incorporated those factors into the equation. We have to take this one day at a time because the news can get better or worse with each passing day. The post Even with blow-out jobs report, mortgage rates still falling appeared first on HousingWire. |

| Longbridge acquisition a positive sign for the reverse mortgage industry Posted: 04 Mar 2022 07:39 AM PST Last week, mortgage investment firm Ellington Financial announced that it had reached a deal to acquire leading reverse mortgage lender Longbridge Financial from Home Point Capital, in a deal valued at roughly $75 million for a 49.6% stake. Since EFC had already maintained a stake in Longbridge, the deal will basically serve to close the remaining gap in ownership and situate EFC as wholly owning Longbridge. Soon after the deal was announced, EFC outlined its reasons for wholly acquiring Longbridge: generally favorable demographics for the reverse mortgage industry; Longbridge's portfolio of mortgage servicing rights (MSRs); and well-established confidence in the lender's financial standing. To gain a clearer understanding of what this deal means for the reverse mortgage industry, RMD spoke to multiple mortgage industry analysts. Positive signsReaction from analysts and watchers of the reverse space has been largely positive. "I was surprised, but to a certain extent just because there was already an existing ownership stake there, it’s a pretty natural next step from that perspective," John Lunde, president of Reverse Market Insight (RMI), told RMD in an interview. "I think that’s a vote of confidence. They’ve obviously had a significant ownership stake for a while and have been pleased with it enough to put more money to work there, and take additional ownership. So, I think that it’s a really positive thing." The deal could have positive reputational effects for the reverse industry. Reverse mortgage lenders, brokers and other participants celebrate any time a mainstream company says anything good about reverse mortgages. Lunde bisects the reputational impact into two buckets: reputation among consumers, and reputation among investors. "On the consumer side, and I don’t know that this deal really changes anything from that perspective only because I don’t know that Ellington is a really well-known brand name," Lunde said. "I think they’re more of a financial institution on the back-end and in financing, and are active behind the scenes a little bit more as opposed to a direct, public-facing consumer brand." As such, it might legitimize the perception that the reverse mortgage business as a good one in the eye of other potential investors, Lunde said. "On that front, this deal is certainly a positive thing," he said. "When I think about acquisitions and how they might help the industry, I think this is a good one. We’ve seen some others that are a little bit similar, with Starwood coming in and backing RMF. The other key piece and the thing that’s been lacking for 10 years in the industry is that big, retail brand presence of some of the big banks or others that have a much more direct-consumer brand." On the investor side, this deal also gives a major reverse mortgage lender potential access to new investor markets, said Michael McCully, partner at New View Advisors. "Ellington has a multi-decade history as a successful mortgage capital markets investor," McCully tells RMD. "Having Ellington consolidate its ownership of Longbridge not only helps Longbridge, it brings additional well-placed intellectual capital to our industry." Upside for EFCThe deal is also a smart move for Ellington, said Douglas Harter, a market analyst at Credit Suisse who covers EFC and also covers Finance of America Companies, another big player in the reverse space. "[I’m] familiar with the favorable demographics and the favorable environment that has been [prevalent in] the past year or two, with the strong home price appreciation helping volumes," Harter said. "I think the backdrop and the investment case to be made in Longbridge is favorable. For EFC specifically, the fact that [Longbridge] is still about 10% or so of their equity even with this deal, I think it fits very much into what they are looking to do." EFC’s goal is to have a diversified model by investing in certain niche areas to bolster its available sourcing channels, according to Harter. Another major factor is Home Point’s precarious position in the forward market. The company, which controls wholesale lender Homepoint, has been selling off parts of its business amid significant margin pressures and strong competition. "[Home Point was] looking to sell their non-strategic or non-core assets in order to improve their liquidity," Harter said. "I think if you put all those pieces together, you have an attractive return to EFC and a partner looking to raise liquidity. I think that when you put those two together, it makes sense for EFC to have acquired the remaining stock." The fact that this is a pre-existing, longstanding relationship between EFC and Longbridge also plays into the perceptions surrounding this deal for Harter. "[EFC is] optimistic about its continuous ability to drive returns from the reverse business," he said. "Both in the ownership of the MSRs, but also the ability to continue to write new business and wanting to own the entity as opposed to just the asset. So, I think it would express a management-favorable view on the outlook for the industry." The post Longbridge acquisition a positive sign for the reverse mortgage industry appeared first on HousingWire. |

| Fannie Mae transfers $771 million in credit risk to private insurers Posted: 04 Mar 2022 07:10 AM PST  Fannie Mae this week completed its first credit insurance risk transfer (CIRT) deal of the year as part of the agency's ongoing efforts to share mortgage risk with the private sector. The deal transferred millions of dollars of credit risk to a group of 22 private insurers and reinsurers. That credit risk is tied to a $26.1 billion reference pool of single-family mortgages. "This credit risk transfer … has increased the role of private capital by transferring $770.7 million of mortgage credit risk to private insurers and reinsurers," the Structured Finance Association states in a brief about the deal. The covered loan pool for the transaction, CIRT 2002-1, includes some 87,600 loans with loan-to-value ratios ranging from 60.01% to 80%. As part of the deal, Fannie Mae will retain risk for the first 25 basis points of any loss on the $26.1 billion loan pool. If that $65.3 million retention layer is tapped, then the 22 insurers and reinsurers will cover the next 295 basis point of loss on the pool, up to $770.7 million. The coverage is based on actual losses over a 12.5-year term. The aggregate amount of coverage can be reduced at the one-year anniversary of the effective date of the deal, and each month thereafter, depending on the paydown of the loans in the mortgage pool and the principal amount of insured loans that move into serious delinquency. In addition, the coverage can be canceled by Fannie Mae after five years with payment of a cancellation fee. “CIRT 2022-1 begins a new, active year of CIRT issuance for Fannie Mae," said Fannie Mae's vice president of capital markets, Rob Schaefer. "We appreciate our continued partnership with the 22 insurers and reinsurers that wrote coverage for this deal,” As of year-end 2021, some $750 billion in Fannie Mae-backed single-family mortgages were included in a reference pool for a credit-risk transfer transaction. Fannie Mae has been revving up its credit-risk transfer machinery in recent months. The GSE has said it plans to do $15 billion in CRT deals in 2022. In early February, HousingWire reported that Fannie Mae unveiled its second CRT deal of 2022, a $1.2 billion note offering through its Connecticut Avenue Securities real estate investment conduit. The post Fannie Mae transfers $771 million in credit risk to private insurers appeared first on HousingWire. |

| Union Home Mortgage promotes three to retail leadership positions Posted: 03 Mar 2022 11:00 AM PST Ohio-based lender Union Home Mortgage made changes to its leadership group, promoting three executives to vice president positions as the company seeks to boost its growth. The company announced on Wednesday that Bryan Wright will be the vice president of national sales and Cyndi Garza, the vice president of national business development, a new position created in the company. Meanwhile, Steve Runnels will hold the role of vice president of retail sales, east division. According to Inside Mortgage Finance, the company is the 49th-largest mortgage lender in the country. UHM's origination volume increased 25.8% in 2021, to $13 billion. In the fourth quarter, the volume was $4.2 billion, up 65.5% compared to the prior quarter. Bill Cosgrove, president and CEO, said in a statement that "through the elevation to these new roles, there is increased opportunity for all to recruit and support talent on a broader level, furthering the growth of the company." Wright, a veteran with over 30 years in the mortgage industry, joined Union Home Mortgage in 2012. Garza began her career at the company in 2011 with the establishment of its first branch in Michigan. Runnels also has three decades in the industry – with a special focus on productive teams and customer fulfillment – and has been a UHM partner for over seven years. In his new role, Wright will be responsible for amplifying the growth of the company's retail division. Garza's efforts are expected to be on developing and identifying new opportunities, working with regional teams to attract and retain partners, and integrating social media into branches across the company. Runnels will expand the growth of the company's east division. The changes in Union Home Mortgage's leadership are happening during a more competitive environment in the mortgage industry. Rates increased to 3.76% for the week ending March 3, amid the geopolitical tensions caused by Russia's war in Ukraine, up from 3.02% a year ago. Meanwhile, lenders' margins are under pressure, mainly in the retail channel. Consequently, some lenders are laying off. California-based WinnPointe Corporation, doing business as Interactive Mortgage, has started a reduction in its workforce of around 180 employees, after suffering more than $1 million in losses. Consumer direct lender Wyndham Capital Mortgage announced the layoff of 35 LOs in January, while refi shops Better.com and Interfirst Mortgage both laid off significant portions of their workforces. Santander Bank announced earlier this month that it would be shutting down its mortgage lending business and laying off its divisional staff. The post Union Home Mortgage promotes three to retail leadership positions appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment