Mortgage – HousingWire |

- PLS market struggling to clear backlog of loans locked at last year’s rates

- Opinion: FHA premiums and the elephant in the room

- How will rising rates affect new home construction?

- AmeriSave hires Sudhir Nair, loanDepot’s former tech leader

| PLS market struggling to clear backlog of loans locked at last year’s rates Posted: 17 Mar 2022 01:57 PM PDT  The rate volatility created by fast-rising inflation, now approaching 8% annualized, and the opposing flight to quality sparked by the war in Ukraine, is complicating an already challenging execution environment in the private-label securities market. Into March of this year, according to multiple market experts, the nonagency secondary market has been digesting a large backlog of mortgage collateral that was locked and originated last year during a much lower-rate environment than exists today. Most of the mortgages securitized in January and February and into March of this year, according to those observers, were originated last year at rates in the high 2% to low 3% range but are hitting the market this year at a time when rates have been climbing, reaching past 4% recently. If that sounds like a perfect storm, add yet another jolt in the form of a 0.25% increase to the Federal Reserve's benchmark federal funds rate announced this week, lifting it off near zero — with some six additional rate hikes planned yet for the balance of this year, until the benchmark rate reaches nearly 2%. (And three more hikes are planned for 2023.) These multiple market pressures have fueled rate volatility and accompanying pricing-execution pressures that have led to a difficult beginning of the year for the private-label securities (PLS) market, according to market experts, and, as a side effect, sparked a more robust market for whole-loan sales — with loans often being sold at a discount. Additional pressure on the PLS market has been created by the increase in agency conforming loan limits for 2022, a change that has pushed more high-balance loans toward Fannie Mae and Freddie Mac and away from the private label securitization market. Similarly, the Federal Housing Finance Agency's [FHFA's] suspension of the cap on agency purchases of investment properties and second homes this past September has continued to create a drag on those deals flowing into the PLS market. Atlanta-based MAXEX, a major aggregator of loans for secondary market offerings, in its March market report describes a challenging scene for the nonagency securitization market. "Rapidly rising rates and widening spreads limited securitization volume in February for both investor [investment property] and prime jumbo issuance," the report states. "… And, as we noted in last month's report, the price for loans traded through the exchange has fallen again as well." The MAXEX report notes that residential mortgage-backed securities (RMBS) deals backed by investment properties decreased "significantly in February," in large part due to the removal of the agency limit on purchasing those loans. "The removal of the FHFA cap in September allowed many originators to sell these loans directly to the agencies at a better execution than the nonagency RMBS market," the report states. David Pelka, head of RMBS business and a principal at Minneapolis-based CarVal Investors, said his firm is active in both the residential whole loan and RMBS markets, with 30 years of experience buying, managing and trading nonperforming, sub-performing and reperforming loans. CarVal has acquired some $10 billion in whole loans over the past decade and a half, he added, and securitized $5 billion in residential mortgages across some 14 offerings. Pelka agrees that the PLS market is under pressure. "In terms of prime jumbo residential mortgage-backed securities, I expect volume to be challenged due to interest rates and bank portfolio bids," Pelka said. "Credit, such as non-QM [nonprime mortgages], is under pressure from rates, spreads, and extension risk. "While there is increased interest from originators to access the non-QM market, this short-term period is very challenging." Pelka also points out that the rate volatility plaguing the market predates the war in Ukraine — unleashed late last year by the emergence in the U.S. of the Omicron variant of COVID-19. "The conflict [in Ukraine] is escalating the problem in RMBS, with continued weak execution on new deals, uncertainty around the path of interest rates and probably some concern with new-origination credit performance due to inflation," Pelka said. John Toohig, managing director of whole loan trading at Raymond James in Memphis, said his firm had a record month in February trading mortgages, adding that "it’s exceedingly rare that we get to see a lot of loans trade at discounts, and there was a pretty wide range of discounts, from 95 to par." "The loans that are coming online right now [in the PLS market] are the loans that were originated back in November and December [2021], as they’ve worked their way through the pipeline," Toohig added. "So, the coupons back then were quite a bit lower than market coupons [now]." He explained that part of the backlog in the securitization market is attributable to the ongoing underwriter shortage in the due-diligence review sector, resulting in many loans "waiting to get diligence and also underwater." "That's not a good combination," Toohig added. Another industry executive, who asked not to be named, said some clients have commented on the underwriter shortage, but "it has not significantly slowed the deal steamrollers I'm seeing." The executive added, however, that "some folks are taking back more bonds than they expected to, and pricing on some deals has not met expectations." "I worked one deal last month [February] that basically broke even," the executive added. Echoing the market woes, Justin Grant, director of investor services at Mortgage Capital Trading in San Diego, said at the start of this year, high-balance (HB) loan production was off by 25%. "I believe it is mainly due to the new conforming loan-limit increases, [which are] allowing some of that market to now fall into a regular-balance [agency] product," he explained. "That being said, rates from the nonagency lenders on HB loans were already right there with the agencies, so the new price adjustments from the agencies will only help to make a nonagency product more attractive for borrowers." That's the larger takeaway here: the resiliency of the PLS market and its ability to ride out rough patches in the rate environment. Even with the challenges facing it, PLS securitization volume is far ahead of last year's mark — which was a record year for the re-emerging PLS market. According to RMBS deals tracked by Kroll Bond Rating Agency, a total of 47 prime and nonprime private-label securitization deals valued in total at $24.6 billion closed through March 25 of this year. That's more than double the volume over the same period in 2021, the KBRA data shows, when 30 deals closed with a total value of $11.5 billion. The agency loan-level pricing bumps taking effect April 1 — and already appearing on originators' rate sheets — are expected to provide a boost to the PLS market at the very time that newer mortgages at more competitive market rates are finally starting to replace the lower-rate collateral that has dominated the first two and a half months of the PLS securitization market. "I think we’re probably in the later innings of this," said one expert on the securitization market who also asked not to be named. "We are starting to see securitizations with more of a current coupon. "I think that will help reset the market because it has largely been digesting paper backed by the lower-coupon stuff. If we can get to a spot where rates are a bit more range bound [less volatile], then I think we’re optimistic that PLS will pick up where it left off last year." The expert added that there is demand out there: "People have money to put to work, and you have investors who want the product." The Fed's plan to increase its key interest rate multiple times in the months ahead also will fuel further upward pressure on mortgage rates. That will likely compound volume challenges in the origination market in the year ahead, mainly by further decreasing demand for refinancing. Still, the fact that there is a road map for rates and stemming inflation now drawn out by the Fed also helps to foster more certainty in the market. "Anytime they [the Fed] can just map it out to the market, it can price it in, but anytime they just talk qualitatively about something, the market is going to run the worst outcome," the securitization-market expert stressed. Toohig of Raymond James agrees that the challenging execution environment the PLS market has faced so far this year is likely not a permanent feature, adding that we "will eventually revert back to a normal market as new production comes on and gets through." The fact that the PLS market is already well ahead of where it was last year at the same time, despite the rough launch into 2022, should bode well for securitization volume for the full year — absent another major market disruption like Russia's invasion of Ukraine or the sudden emergence of a new, troublesome COVID variant. "The market has to work through that old inventory first, and that’s kind of what’s been choking the system," Toohig added. "I think the real question for those people who are carrying loans during this period is, ‘Did they hedge?’ "Those that hedged are probably in a better spot than those that were carrying loans unhedged. Those are the ones that probably get hurt." The post PLS market struggling to clear backlog of loans locked at last year's rates appeared first on HousingWire. |

| Opinion: FHA premiums and the elephant in the room Posted: 17 Mar 2022 01:48 PM PDT As HUD considers mortgage insurance premium (MIP) changes in the aftermath of FHA's record-breaking FY 2021 performance with $100 billion of capital reserves and a capital ratio of 8%, it is time to address the "elephant in the room." Since the housing crisis, FHA premium policy has been more effective in "providing space for private capital" (as HUD referred to it in its FY 2011 Report to Congress) than providing fairness and equity to FHA borrowers. Instead of increasing the upfront premium to minimize the impact on FHA borrowers, HUD took the unprecedented step of increasing the annual premium significantly and later adding the life-of-loan requirement. Together they make it harder for borrowers to qualify, more expensive for each year the loan remains in effect and, most importantly, send a clear message to mortgage originators to avoid recommending FHA financing if at all possible. FHA's rising prominence "to fill the void left by the reduction of private capital," as HUD also said in the FY 2011 Report, had created a dilemma for those in Washington worried about FHA's growing market share. In the FY 2011 Report, HUD explained its "challenge" this way: "One of the challenges we face in the current environment is the balance between assuring mortgage credit flows for low-to-moderate income households, minorities and first-time homebuyers and providing space for private capital to return to supporting mortgage credit risk." [bolding added] The problem with HUD's solution to "providing space for private capital" was not that it raised FHA premiums. MIP increases were necessary back then to ensure FHA's actuarial soundness. What is disappointing was how HUD did it and the fact that these policies, to a large extent, still remain in effect today. Between 2010-2014, FHA raised annual premiums by 145%. Even with the 50 basis point reduction in January 2015, current annual premiums are still 50% higher than before the housing crisis ($70 per month higher on average for FY 2021 originations). For borrowers who obtained FHA loans last year, they are paying an additional $1 billion in the first year alone as a result of the higher monthly MIP. In June 2013, HUD went a step further in its effort "for providing space for private capital" when they added the life-of-loan requirement. This change increases "lifetime" premium costs for borrowers unable to refinance their FHA mortgages to more than $50,000 on an FHA mortgage of $200,000. To make matters worse, this "lifetime" burden will likely fall disproportionately on families of color. A June 2021 Federal Reserve Bank of Boston study found that minorities are "significantly less likely to refinance to take advantage of the large decline in interest rates." The life-of-loan change is also detrimental to the FHA Fund as it is giving borrowers a strong incentive to refinance out of the program as soon as possible, costing FHA billions of dollars in premium revenue. FHA's recapture rate (i.e. the percentage of loans that prepay and return as an FHA refinance) has plummeted since the life of loan provision was implemented falling from over 50% in the 2010 – 2012 period to 18% in the first four months of FY 2022. Let's also not forget who FHA borrowers are. Eighty-five percent of FHA purchasers were first-time homebuyers, and borrowers of color obtained over 40% of FHA loans in FY 2021. FHA also insured more than twice as many loans to Black and Hispanic borrowers last year as the rest of the mortgage market combined. The life-of-loan policy has always been at the heart of the debate about FHA premiums. Advocates maintain that FHA must charge premiums for as long as the loan remains in effect. They act like charging monthly premiums for the life of the loan is the only way that FHA can protect the fund and taxpayer from the "tail risk" of loans defaulting after 11+ years of borrowers making their payments. They must have forgotten that FHA's private sector counterparts offer several upfront premium plans and that the Reagan Administration even introduced an upfront-only premium to the FHA program in 1983. Of course, the life-of-loan requirement discourages borrowers from obtaining FHA loans in the first place. Just look at the marketing material of the private mortgage insurers highlighting the cancellability feature of their insurance. I am sympathetic to the private mortgage insurers' position since much of their competitive dilemma is dictated by the pricing policies of Fannie Mae and Freddie Mac. I just don't believe that FHA borrowers who already face their own financial challenges should be required to bear unnecessary and significant financial costs for the purpose of "providing space for private capital." Instead of FHA charging high annual premiums for the life of the loan, the mortgage insurers and their allies should direct their efforts to the source of the problem, namely the Federal Housing Finance Agency's (FHFA) pricing policies and Loan Level Price Adjustments (LLPAs) in particular. Acting Director Sandra Thompson has said that FHFA will be looking at pricing "holistically." That's encouraging, but regardless, families using FHA financing should no longer be victims in this debate. We are already seeing proposals encouraging additional targeting of any MIP reduction. Targeting would only deny excluded borrowers the premium reduction that they deserve and also increase risk for the Fund. It is important to remember that FHA was founded on fundamental insurance principles. Like any successful insurance program, FHA must spread its risk. At the same time, a cornerstone of the FHA program has always been charging all borrowers the same premium, in part to discourage borrowers with lower risk factors from using the program. However, to the extent those lower-risk borrowers do use FHA financing, their premiums certainly help offset losses projected for loans having higher risk characteristics (i.e. cross-subsidization). As Housing Wire reported recently, FHA's performance has gotten even better since the FY 2021 Report to Congress was published. Serious delinquencies have declined more than 20% in the first four months of FY 2022 on top of a 30% decline in FY 2021. FHA could now pay a claim on every serious delinquency and still have $70 billion in capital reserves and a capital ratio of 5.5% or more than 2 ½ times the statutory level of 2%. For 10+ years, FHA has been charging very high annual premiums on arguably its best credit quality portfolio in at least 50 years. Gone are the seller-funded downpayment assistance loans that cost the fund over $16 billion and FHA's low average credit scores in the run-up to the housing crisis that bottomed out at 630 for FY 2007. The strong house price appreciation numbers of the last two years only made FHA's financial performance even better. From Day One, the Biden Administration has made homeownership the cornerstone of its effort to reduce the racial wealth gap in our country. Eliminating the life of loan and lowering the annual premium will not solve all of the problems facing underserved borrowers, far from it. They will just remove unnecessary costs for millions of FHA borrowers who already face enough challenges in the pursuit of their American Dream. Brian Chappelle is a partner at Potomac Partners and a former director of single-family development at both the FHA and HUD. This column does not necessarily reflect the opinion of HousingWire's editorial department and its owners. To contact the author of this story: To contact the editor responsible for this story: The post Opinion: FHA premiums and the elephant in the room appeared first on HousingWire. |

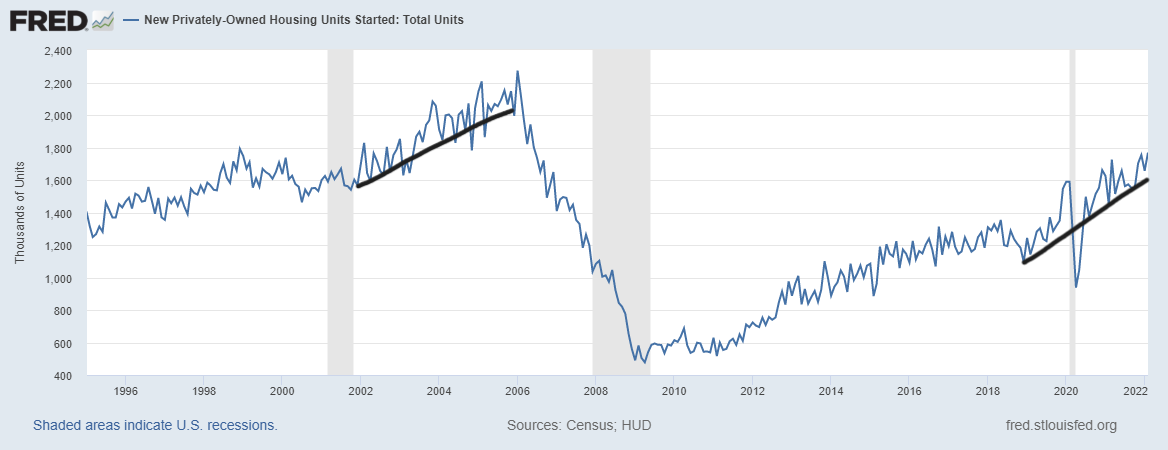

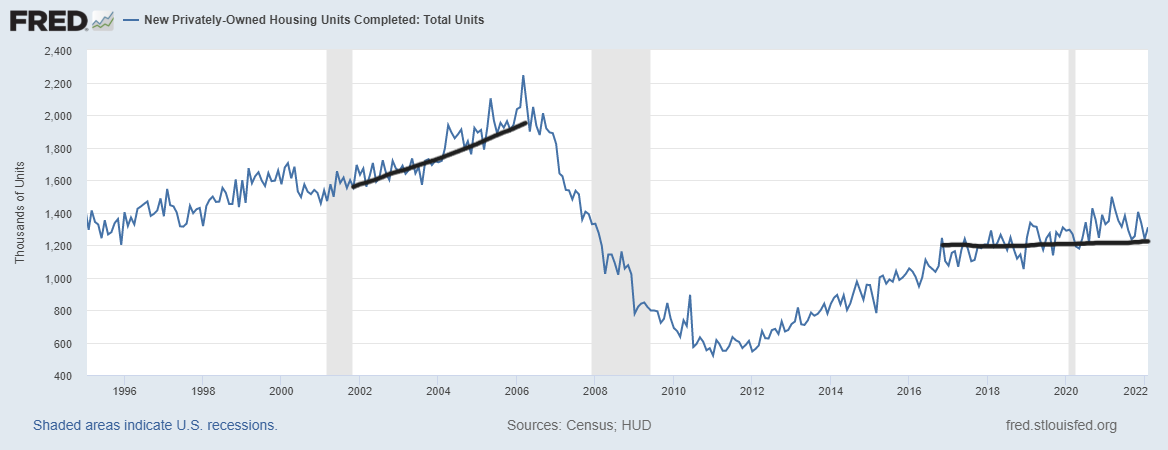

| How will rising rates affect new home construction? Posted: 17 Mar 2022 01:25 PM PDT  Today, the U.S. Census Bureau released their construction report for February, showing a positive trend in housing construction data with a lovely print in housing permits at 1,859,000 and housing starts at 1,769,000. The previous months of housing data have been positively revised higher as well, so this is a solid report on all fronts. Of course, that’s until you look at the housing completion data, which hasn't gone anywhere in years. In fact, considering the drop in builders’ confidence, now we have to watch for whether some people will cancel their building contracts because rates have jumped so much while they’ve been waiting for their new home to be built. Housing starts data, like new home sales data, can be wild month to month, so the trend is always more important than any one report and the revisions are critical. We can have one monthly report with an extremely positive or negative print that is revised higher or lower the next month. The fact that the headline number on this report was good and the revisions were positive is a good sign. So far, housing construction has done well during 2020-2022 considering the economic drama. The housing sector has had to deal with a global pandemic, shortages of products and skyrocketing lumber costs, but in the end, mother demographics wins. Housing startsFrom Census: Privately‐owned housing starts in February were at a seasonally adjusted annual rate of 1,769,000. This is 6.8 percent (±14.9 percent)* above the revised January estimate of 1,657,000 and is 22.3 percent (±14.3 percent) above the February 2021 rate of 1,447,000. Single‐family housing starts in February were at a rate of 1,215,000; this is 5.7 percent (±11.8 percent)* above the revised January figure of 1,150,000. The February rate for units in buildings with five units or more was 501,000. As we can see below, slow and steady wins this race. We had more housing starts during the bubble years because from 2002 to 2005 that demand curve was higher, but it was facilitated by unhealthy credit growth. The homebuyers of new homes today are very solid, but since we don't have a credit boom in housing, housing starts will move up slowly. This is a very positive thing because it's real. When you have a speculative credit bubble, you're prone to a massive correction. Remember that back in 2018, the new home sales and housing starts sector had a slowdown when mortgage rates got to 5%. It wasn't a crash in demand but a slowdown for sure. Since the previous expansion was slow and steady, we weren't ever working from an overheated new home sales sector, so the slowdown never created a crash. Since then, housing starts have been increasing as new home sales have been growing. Housing permitsFrom Census: Privately‐owned housing units authorized by building permits in February were at a seasonally adjusted annual rate of 1,859,000. This is 1.9 percent below the revised January rate of 1,895,000, but is 7.7 percent above the February 2021 rate of 1,726,000. Single‐family authorizations in February were at a rate of 1,207,000; this is 0.5 percent below the revised January figure of 1,213,000. Authorizations of units in buildings with five units or more were at a rate of 597,000 in February. I see a similar story here with housing permits: the trend is your friend and slow and steady wins the race. The big difference for me in the years 2020-2022 from 2008-2019 is that the low bar in housing starts is gone. The previous economic expansion had the weakest housing recovery ever; new home sales and housing starts were working from deficient levels and didn't have the boom that many people had hoped for. It looked pretty normal to me; I didn't anticipate housing starting a year at 1.5 million until 2020-2024 because then the demand for new homes would warrant that much construction. People forget that housing construction is built on the need for new homes, which are more expensive than the existing home sales market. So the meager inventory in the existing home sales market has benefited the builders because it makes their products more valuable. Housing completionsFrom Census: Privately‐owned housing completions in February were at a seasonally adjusted annual rate of 1,309,000. This is 5.9 percent (±13.3 percent)* above the revised January estimate of 1,236,000, but is 2.8 percent (±12.0 percent)* below the February 2021 rate of 1,347,000. Single‐family housing completions in February were at a rate of 1,034,000; this is 12.1 percent (±14.7 percent)* above the revised January rate of 922,000. The February rate for units in buildings with five units or more was 266,000. As you can see below, we haven't gone anywhere for years now. It's a shame that the housing market has to deal with so much drama while the U.S. has the most prolific housing demographic patch in history. Here is where we can talk about some risks looking out to the housing market. Mortgage rates have risen since the lows we saw last year. You can make a case that a few people, not many, might not want to buy their expensive new home now that rates have just moved higher. However, I will give a personal take on this after talking to a friend who sells new homes. The buyers are frustrated beyond belief with how long the process is taking while they watch rates rise. However, what my friend said was: What else are they going to do? The fact that total existing inventory is at all-time lows and it's been a madhouse trying to buy a house has kept some new home buyers in line. The recent builder's confidence data took a noticeable fall, and there is some concern about future sales. I believe the homebuilders confidence index showing you the directional changes in the housing market landscape is critical. In 2020, we had an abnormal surge in housing data which was just showing make-up demand toward the end of the year in 2021. Naturally, the housing data was going to moderate from this pace in 2021. The housing data to me outperformed toward the end of 2021, so look for some moderation in the data coming up as well. Regardless of that premise, keep an eye out on the builder's confidence and the monthly supply of new homes data to gauge the health of this sector of our economy. From NAHB: All in all, the Census Bureau’s construction report was solid and had positive revisions. However, we are still hampered by the limits of being able to finish building homes promptly. Now that rates have risen, we need to wait and see if that impacts buyers wanting their homes with much higher rates. The new home sales market is more sensitive to mortgage rates than the existing home sales market. History has shown us that when demand isn't growing, the builders will slow down the growth rate of construction. The post How will rising rates affect new home construction? appeared first on HousingWire. |

| AmeriSave hires Sudhir Nair, loanDepot’s former tech leader Posted: 17 Mar 2022 11:21 AM PDT Online home mortgage lender AmeriSave Mortgage Corporation announced on Thursday that Sudhir Nair, the former head of information and technology at loanDepot, has been tapped as its first-ever chief digital officer. Nair, who has worked in technology leadership roles at Bank of America, Xome/Mr. Cooper, CountryWide, Amazon and others, will help the lender become more efficient in delivering mortgage services, passing along savings to its customers in the form of low rates, AmeriSave said. Atlanta-based AmeriSave operates in 49 states and D.C. (the lender does not originate mortgages in New York), according to its website. The lender funded $36 billion in mortgages in 2021, according to Inside Mortgage Finance. That was good for 23rd most in America last year. IMF data shows that 92% of the company’s originations were refis, not unexpected for consumer direct lender. The company offers a standard mix of vanilla products, including conventional, jumbo, FHA, VA, and USDA loans. AmeriSave allows its customers to “self-serve” their loan transactions with its software, which it claims drives speed and greatly lowers the cost to produce a loan. "Having Sudhir join the AmeriSave team is a huge win for our company," Magesh Sarma, chief information officer and chief strategy officer, said in a statement. He added that Nair is well-known in the fintech industry as an innovator and a key player in providing solutions that impact a company's performance. Nair has the resume for a digital products job in mortgage. Before joining AmeriSave, he was chief information and technology officer at loanDepot, a position he held from 2019 through January 2021, according to his LinkedIn profile. Nair left loanDepot – which has prioritized tech infrastructure for lead generation – amid a restructuring of its operations. The lender announced on March 11 that it would segment a new division called mello, under the leadership of the digital technology veteran Zeenat Sidi. Sidi has held roles with Royal Bank of Canada, Capital One, and Sofi. Prior to joining loanDepot, she was at the fintech company Mission Lane. Mello's unit, which shares the name of the software platform loanDepot launched in 2017, will operate side-by-side with the company's mortgage origination and servicing division. The unit will include the customer contact center, the mello DataMart, and the performance marketing engine. Three adjacent businesses – mellohome Real Estate Services, melloinsurance, and mello title and escrow services – will also be under Sidi. The post AmeriSave hires Sudhir Nair, loanDepot’s former tech leader appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment