Mortgage – HousingWire |

- Figure and Apollo complete ownership transfer via blockchain

- Mortgage rates rise 31 bps to 4.16%

- Shareholder sues loanDepot’s top executives

- What the Fed rate hike means for the economy

- The Fed makes its move – and more rate hikes are coming

- Opinion: How to attract and retain women in mortgage

- UWM rolls out bank statement loans for self-employed borrowers

- ICE integrates Maxwell and Roostify to eClose solution

- Angel Oak Mortgage REIT records solid earnings performance

- Mortgage applications drop as rates spike

| Figure and Apollo complete ownership transfer via blockchain Posted: 17 Mar 2022 09:00 AM PDT Figure, a blockchain-focused financial service company and Apollo, a global alternative asset manager, announced today completing a transaction involving the origination of digital mortgage loans and transfer of ownership via blockchain technology, according to a press release shared with FinLedger. The companies say the secure process was a “first of its kind” in the mortgage industry and has the potential to revolutionize the $3 trillion mortgage ecosystem. During the transactions, Apollo purchased eNote digital mortgage assets, originated by Figure on the Provenance Blockchain and registered on its Digital Asset Registration Technologies (DART) platform, via an investment vehicle it manages on a blockchain-based marketplace. The release says that when coupled with a connected digital currency account, this technology enables real-time, multi-party settlement that incurs less risk than traditional methods. "With technology impacting all areas of our lives, it is time for participants across the mortgage ecosystem to experience an improved process that simply works better and costs less," said Daniel Wallace, GM of Figure Lending. "Blockchain can provide enhanced protections and transparency in the ownership process for consumers and real-time settlement for investors, replacing trust with truth to create a faster, more efficient process for everyone. This important development demonstrates just one way that blockchains will provide significant improvements that streamline the mortgage lending space,” Wallace said. DART, a combined lien and eNote registry system developed by Figure, is used in place of the existing MERS (Mortgage Electronic Registration System) database. The system monitors blockchain-based asset transfers and enables an efficient alternative to the MERS loan tracking database, which often takes weeks to process settlements for paper promissory notes. The release adds that this system enables immediate and automated asset onboarding, real-time settlement for loan pledges and sales, and uses an integrated registration system that can automatically reflect transfers on loan interests. "When Apollo and Figure formed a strategic partnership, we saw the potential to apply the Provenance blockchain – built specifically for the financial services industry – to processes across the investment lifecycle. We are excited to have now completed our first use case with this mortgage transaction, executed in a way that we believe can dramatically improve efficiency in the mortgage and lending ecosystem,” said Apollo Partner Robert Bittencourt. In other recent proptech news, Baselane launched its property-focused banking platform to simplify rental property finances for individual landlords. JLL‘s Valuation Group also launched a new property intelligence and technology tool, Valorem, which gives clients the ability to organize and manage their portfolio’s property and valuation data. The post Figure and Apollo complete ownership transfer via blockchain appeared first on HousingWire. |

| Mortgage rates rise 31 bps to 4.16% Posted: 17 Mar 2022 07:27 AM PDT As the Federal Reserve raised short-term rates for the first time in years, mortgage rates climbed 31 basis points to 4.16%, according to data from Freddie Mac‘s PMMS survey. "The 30-year fixed-rate mortgage exceeded four percent for the first time since May of 2019," said Sam Khater, Freddie Mac's chief economist. "The Federal Reserve raising short-term rates and signaling further increases means mortgage rates should continue to rise over the course of the year. While home purchase demand has moderated, it remains competitive due to low existing inventory, suggesting high house price pressures will continue during the spring homebuying season." During a highly anticipated meeting on Wednesday, the Federal Reserve raised the benchmark rate a quarter of a percentage point. The Fed said there would likely be six more rate hikes in 2022 and three more in 2023, the primary tool the central bank is using to reduce inflation, which climbed to a 40-year high in February, at an annual rate of 7.9%. The 30-year-fixed rate rose 31 points from 3.85% for the week ending March 17, according to Freddie Mac. A year ago, the 30-year averaged 3.09%. Freddie Mac assumes borrowers bought 0.8 mortgage points on their loan. The 15-year fixed-rate mortgage averaged 3.39%, up from 3.09% last week. A year ago, the 15-year fixed-rate mortgage averaged 2.40%. The 5-year Treasury-indexed hybrid adjustable-rate mortgage averaged 3.19% with an average of 0.2 points purchase by borrowers, 22 basis points higher last week. A year ago, the 5-year ARM averaged 2.79%. The increase in rates in recent months has dramatically chilled refinancing activity in the mortgage market. According to the Mortgage Bankers Association, refi applications this week are down 49% from a year ago, and rate lock data from Black Knight found that refis in February were down to just about one-third of mortgages. Staying nimble in a fast-paced market with the right mortgage technology In the rapid-fire, volatile mortgage marketplace, lenders need technologies to help them remain nimble and successfully navigate constant change. Advanced product, pricing and eligibility technology creates efficiencies and helps lenders compete in a fast-paced market. Presented by: Black KnightThe seasonally adjusted purchase index increased 1% from one week earlier; the unadjusted purchase index increased 2% from the prior week but was 8% lower than the same week a year ago, largely due to a decline in inventory. Still, it remains to be seen whether the spoke in mortgage rates back to 2019 levels will chill the purchase market, which in many markets is still defined by low inventory, multiple offers and bidding wars. Zillow reported late last week that inventory dropped to 729,000 home listings in February, a 25% drop year-over-year and a 48% fall since February 2020. It was the fifth consecutive drop in inventory. While mortgage rates will chill the refi market, the Federal Reserve laying out a clear path ahead should stem some of the volatility with mortgage rates, which have been on a rollercoaster ride for over a month. The post Mortgage rates rise 31 bps to 4.16% appeared first on HousingWire. |

| Shareholder sues loanDepot’s top executives Posted: 16 Mar 2022 05:07 PM PDT  California-based nonbank lender loanDepot is the target of a new shareholder lawsuit. Investor Tuyet Vu accuses seven top executives and board members, including loanDepot's founder Anthony Hsieh, of making misleading statements and omitting information in connection with the company's initial public offering (IPO). LoanDepot debuted in the stock exchange in February 2021, raising just $54 million. The suit was filed in the U.S. District Court in Delaware on March 11. Two other federal securities fraud class action lawsuits are pending in the U.S. District Court for the Central District of California. The complaint lists as defendants Hsieh, the chief financial officer Patrick Flanagan and the chief accounting officer Nicole Carrillo. It also includes four board members: Andrew Dodson, John Dorman, Brian Golson, and Dawn Lepore. In the shareholder derivative lawsuit, Vu accuses the executives of unjust enrichment, abuse of control, gross mismanagement, waste of corporate assets and violations to the Securities Exchange Act. LoanDepot did not respond to requests for comment. According to the lawsuit, from February 2021 through August 2021, executives allegedly failed to disclose that loanDepot's refinance originations and margins had declined substantially at the time of the IPO, negatively impacting revenue and growth. In addition, management allegedly failed to disclose that "revenue and growth were artificially buoyed by overcharging of interest from at least 2016 to 2019 and by the closing of loans without proper documentation in the period preceding the IPO." Meanwhile, defendants benefitted from lucrative insider sales of $164,595, the suit claims. The complaint alleges that the "truth" about the company's poor performance emerged on August 3, 2021, when loanDepot reported disappointing earnings for the second quarter of 2021. As a consequence, the price per share of the loanDepot's Class A common stock fell to $8.07 by August 3, down 42% since the IPO. The shareholder complaint mentions another lawsuit, this one filed by Tammy Richards, formerly loanDepot's chief operations officer. In September, Richards dropped a bombshell in the mortgage industry alleging that, between at least 2016 and 2019, loanDepot and its subsidiary Closing USA had engaged in interest overcharging. According to the executive, the company was "charging loan refinance borrowers double daily interest during a period when CUSA had failed to timely pay off original loans, but new loans had already been originated." Richards also alleged that Hsieh directed individuals to close loans without proper documentation. The nonbank mortgage lender disputed the claims made by Richards, who worked in senior roles at Wells Fargo, Bank of America, Caliber Home Loans and Countrywide Financial (one of the bad actors in the subprime loan crisis) before joining loanDepot. "LoanDepot is committed to operating at all times according to ethical, responsible and compliant business practices," a statement from the company in September read. "The claims in the lawsuit, which we take very seriously, were previously thoroughly investigated by independent third parties and found to be without merit," loanDepot said, without providing further information about who conducted these investigations and when they occurred. "We intend to defend ourselves vigorously against these outlandish allegations…" The post Shareholder sues loanDepot’s top executives appeared first on HousingWire. |

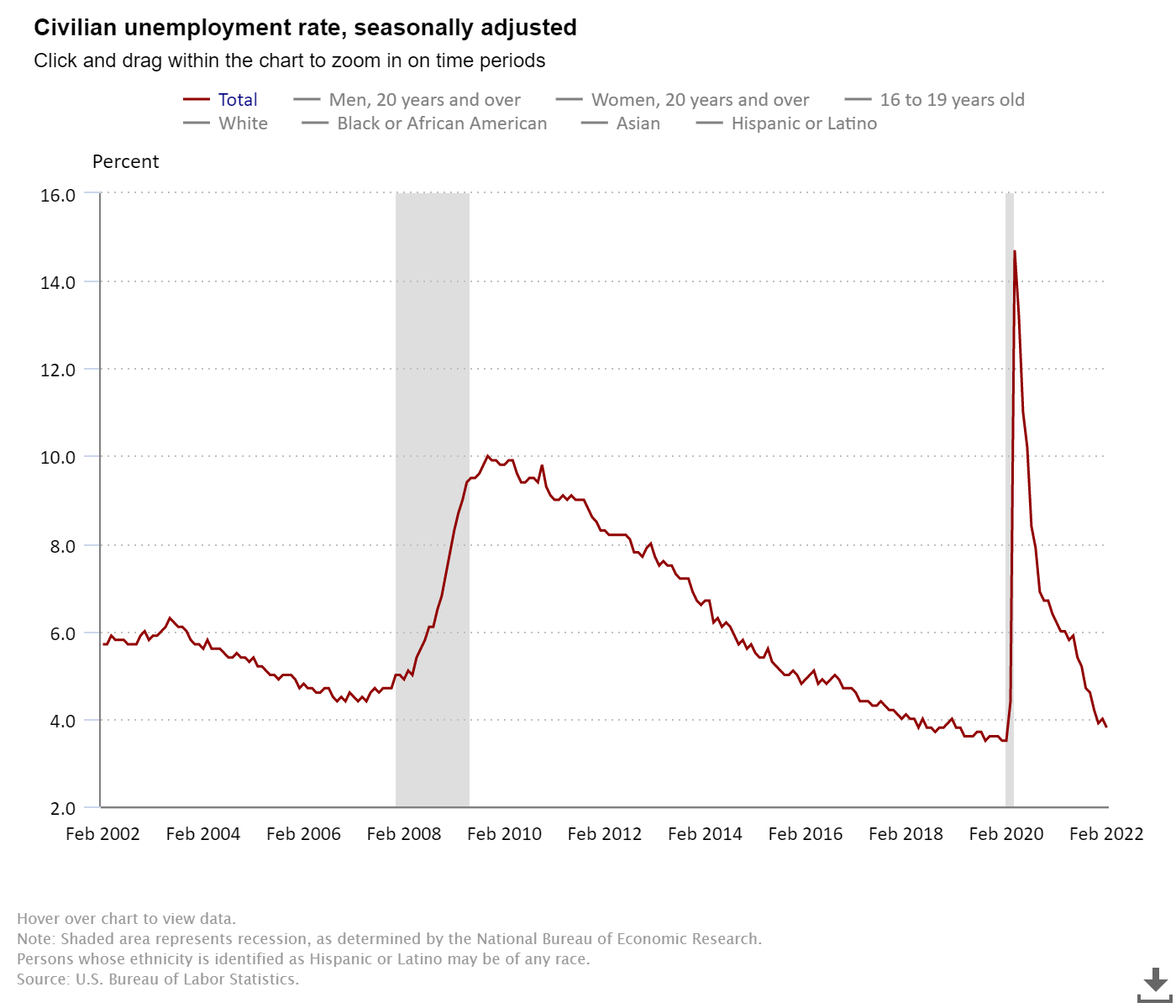

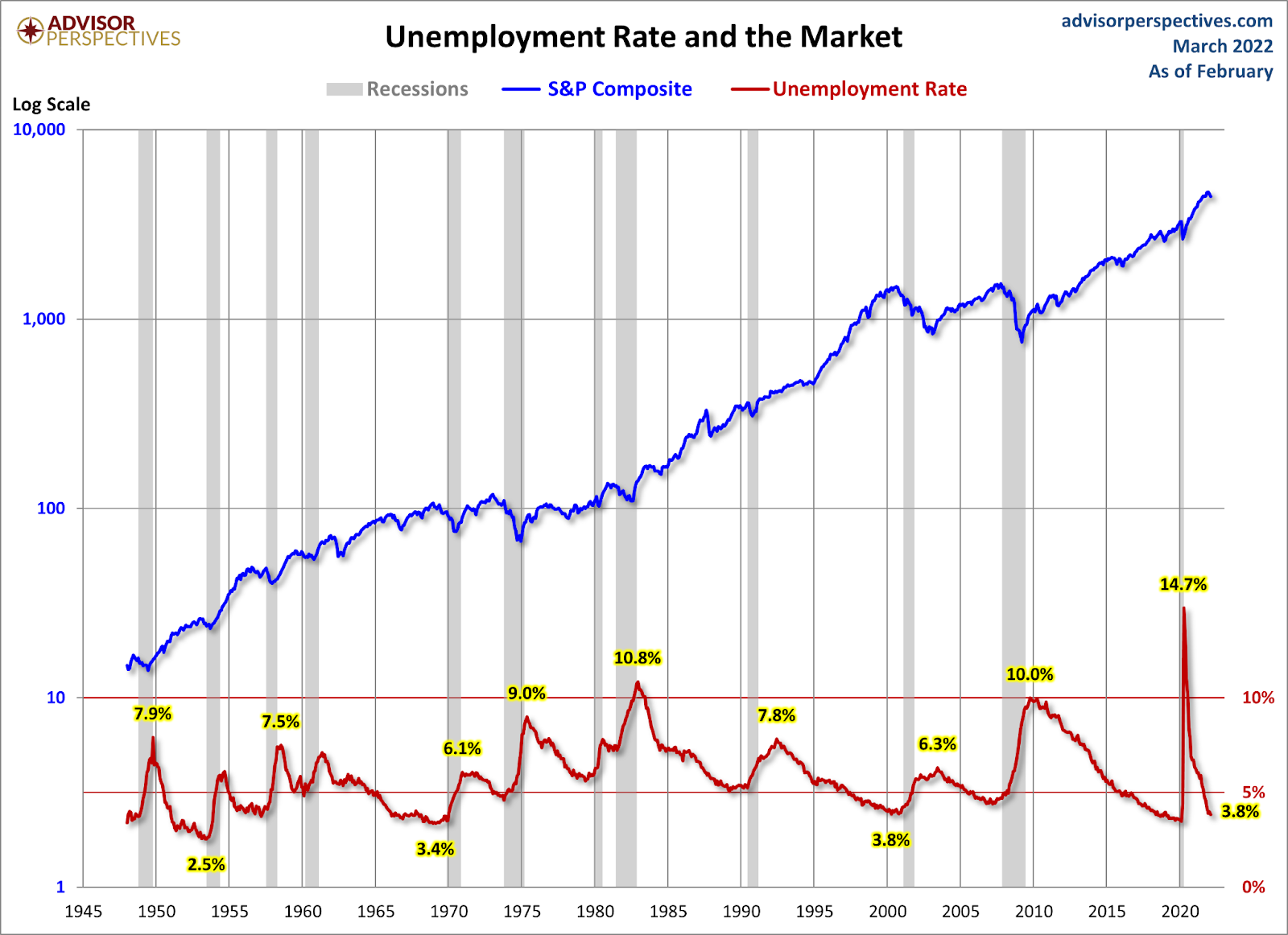

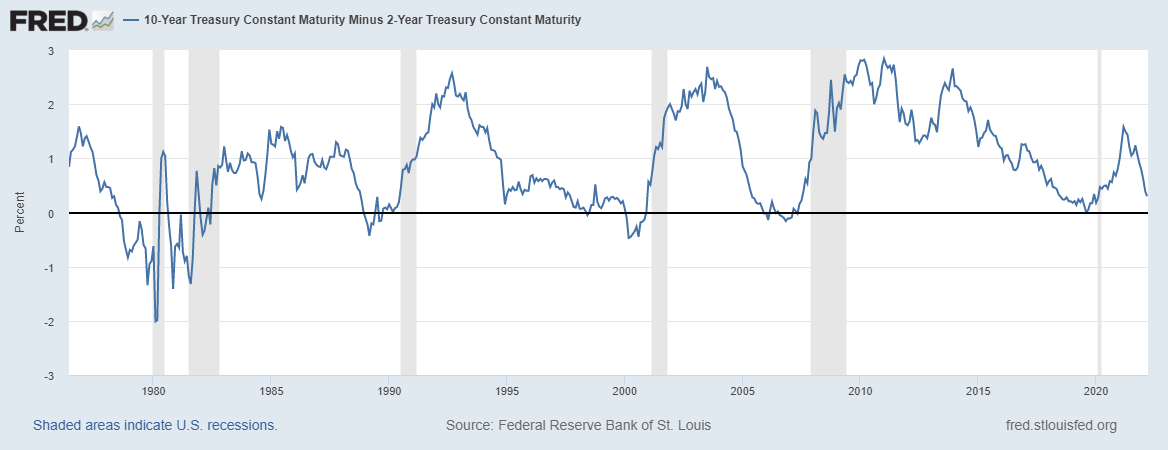

| What the Fed rate hike means for the economy Posted: 16 Mar 2022 04:13 PM PDT  On Wednesday the Federal Reserve hiked interest rates 0.25%, which has forced me to raise my second recession red flag on this historic economic recovery and expansion. The invasion of Ukraine by Russia is causing tremendous human and economic hardship. The implications for the U.S. economy are highly uncertain, but in the near term the invasion and related events are likely to create additional upward pressure on inflation and weigh on economic activity. The first Fed rate hike isn't going to take us into a recession, it just raises the second of the six flags we would need to go into a recession. But looking forward, the Federal Reserve has now started to pull back from their accommodative stance because they believe the economy is too strong and the concern right now is to fight inflation with rate hikes. From the Fed: The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With appropriate firming in the stance of monetary policy, the Committee expects inflation to return to its 2 percent objective and the labor market to remain strong. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent and anticipates that ongoing increases in the target range will be appropriate. In addition, the Committee expects to begin reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities at a coming meeting. I raised the first recession red flag when the unemployment rate got to 4% and the two-year yield got over 0.56%. Again, this red flag showed the progression of an economic expansion, and the recovery was so extreme that the unemployment rate fell very fast. The low unemployment rate isn't a recession factor, but all expansions end when the unemployment rate is at the lowest level. I am trying to show you the stages of an economic expansion into a recession, which is why I believe in the red-flag model. The Russian Invasion of Ukraine is a brand new variable shock to the global economy that needs to be monitored daily. Unlike COVID-19, there is no fiscal disaster relief and no rate cuts coming. The Federal Reserve's job is to cool down this hot economy, so the economy now has pressures on two fronts. Recession red flag No. 3: The inverted yield curveAs I am writing this article, the 10-year yield is 2.17% and the two-year yield is 1.94% which means the inversion spread is now 0.23%. Historically speaking, when the 10-year yield and the two-year yield meet to say hello and shake hands (the inversion), the recession isn't too far off. In the chart below, the grey shaded bars show when the economy is in a recession and the black in the middle is when the 10-year and 2-year yields shake hands. How we get to higher yieldsI am big fan of higher yields to create balance in the housing market. However, in 2021 I did not believe we had the capacity for the 10-year yield to break over 1.94%, which would get us to 4% plus mortgage rates. However, part of my 2022 forecast was that if global yields rise, especially in Japan and Germany, the 10-year can get up to 2.42% this year, which means 4% plus mortgage rates. From the forecast: "We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don't support this." The economy has been on fire for some time now, but only recently has the 10-year yield been able to breach over 1.94%. This is mainly due to global yields rising not so much of the U.S. We have the hottest economic and inflation data in decades and the 10-year yield is only at 2.17%. Now the tug of war begins: Can the U.S economic data can stay firm with all this inflation and higher rates, or will the weakening economy send yields lower again? As someone who has been rooting for higher rates because the housing market is savagely unhealthy, I hope it can create some balance. If economic data gets weaker, I am concerned rates will go back down again. We lose our only variable that can create balance in the housing market. I believe in economic models as they keep us in line. In this day and age of boom and bust 24/7 marketing for clicks, I understand that boring economic models might not be so sexy. However, economics isn't supposed to be a hot summer flick. I always want to be the detective and not the troll. The main reason I continued writing after 2015 wasn't because of the housing market work I have done — I wanted to be a source of information for the economic expansion and recession that wasn't predicated on extreme ideological or stock trader takes. This is why I wrote the America Is Back Recovery Model on April 7, 2020. So to wrap it all up, the second recession red flag is up, and I am keeping an eye out on the third one. Once that bridge is crossed, I will update the model accordingly. We will hold hands together as we continue this slow dance of information, and when something meaningful pops up, I will let you know about it. Buckle up for the rest of the year and root for more housing inventory; we need to get back to 1.52 – 1.93 million! The post What the Fed rate hike means for the economy appeared first on HousingWire. |

| The Fed makes its move – and more rate hikes are coming Posted: 16 Mar 2022 01:53 PM PDT The Federal Open Market Committee on Wednesday raised the federal funds rate for the first time in four years, marking an end to the easy money that gave rise to the hottest mortgage market in U.S. history. The FOMC, as was predicted, raised the federal funds rate by 25 basis points to 0.25-0.50 percent, the first time the FOMC has changed the federal funds rate in two years, and the first rate hike since March 2018. The move, designed to slow the pace of inflation, which reached 7.9% for the year that ended in February, is sure to increase the cost of mortgage borrowing. Whether it slows the frenetic pace of a housing market with historically low supply is yet unclear. “The Fed worked to ensure today's announcement would not be a surprise, with the rate hike following a series of foretelling decisions, including its acceleration of asset tapering in December through the end of its asset purchase program earlier this month,” Realtor.com‘s chief economist Danielle Hale said in a statement following the announcement. “The Fed's language in its public statements has also prepared markets for rate increases by consistently focusing on above-target inflation and progress against labor market goals. This also meant that mortgage rates have largely adjusted for the first hike, and I don't expect a spike following the latest announcement.” Beyond the initial 25 bps rate hike, the Fed also said it planned to raise rates six additional times in 2022 and three times in 2023, giving more certainty to investors in the secondary market, which should help ease overall volatility somewhat. How should the current market impact lenders’ tech adoption? HousingWire recently sat down with Polly CEO Adam Carmel to discuss how lenders can break old habits and redefine the mortgage process through innovation and modern, advanced technology. Presented by: Polly"With the unemployment rate below 4%, inflation nearing 8% and the war in Ukraine likely to put even more upward pressure on prices, this is what the Fed needs to do to bring inflation under control,” said Mike Fratantoni, chief economist of the Mortgage Bankers Association. “The FOMC economic projections indicate slower growth and higher inflation than had been the expectation at their December meeting. Note that they do not expect to be back at 2% inflation until after 2024." Big questions remain, however. It’s still not entirely clear how quickly the Fed will unwind its $9 trillion balance sheet. The Federal Reserve said it would "begin reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities at a coming meeting," but did not get more specific. "Although we anticipate that shrinking the balance sheet will begin this summer, we will be looking for details regarding the pace of the runoff and whether they would consider active MBS sales at some point to return to an all-Treasury portfolio," said Fratantoni. The purchases of Treasuries and MBS, which ended this month and were designed to support the economy during the Covid-19 pandemic, helped the housing and mortgage markets reach never-before-seen heights. Fueled by a sharp drop in mortgage rates during the pandemic, the U.S. mortgage industry funded $4.1 trillion in new loans in 2020 (64% refis, 36% purchases), and $3.9 trillion in 2021 (57% refis, 43% purchases), according to the MBA. But refi applications fell to about one-third of rate locks in February, and lenders have switched gears to serve a heavy purchase market. And that market is largely defined by a dearth of inventory. On Friday, Zillow reported that overall housing inventory dropped to 729,000 home listings in February, a 25% drop year-over-year and a 48% fall since February 2020. It was the fifth consecutive drop in inventory. Though the rise of mortgage rates – the MBA anticipates rates to hover around 4.5% for the next year – will force some would-be buyers out of the purchase market, other factors appear more important. "Mortgage rates have already been increasing for many reasons — improving economy, higher inflation expectations and Fed tightening,” said Odeta Kushi, deputy chief economist of First American Financial. “As rates rise, some buyers on the margin will pull back from the market and sellers will adjust price expectations, resulting in a moderation in house price appreciation." But, Kushi added: "The other implication of a rising mortgage rate environment is the rate lock-in effect. Many homeowners have locked into historically low rates, and are less likely to move as rates move higher — this does not bode well for housing supply." The post The Fed makes its move – and more rate hikes are coming appeared first on HousingWire. |

| Opinion: How to attract and retain women in mortgage Posted: 16 Mar 2022 01:41 PM PDT Women have, undoubtedly, made great strides in earning coveted leadership positions in the workplace. According to data from McKinsey and LeanIn.org's 2021 Women in the Workplace Study, the share of women in senior vice president and C-suite positions has grown in recent years – up six percentage points for SVP roles (23 to 29%) and four percentage points for C-suite roles (17 to 21%) between 2015 and 2020. While this data is promising, for many women in corporate America, their future in the workplace hangs in the balance due to the disproportionate impact the COVID-19 pandemic has had on them. As women often bear the brunt of unpaid domestic work, child and elder care, and schooling from home due to pandemic lockdowns — all while trying to juggle their careers — they have reported feeling higher levels of burnout than their male counterparts. In fact, the same McKinsey and LeanIn.org study revealed that one in three women have even contemplated downshifting or leaving the workforce altogether (and, nearly 1.8 million of them have already left). This mass exodus could have serious, long-term implications on the number of women in leadership roles. While we cannot flip a switch and undo the damage done overnight, we can and should be mindful of these statistics and take actionable measures to promote and attract women to a career in the mortgage industry in addition to retaining women within our own workplaces. How can we attract and retain women? As a woman leader in the mortgage industry — an historically male-dominated field — I, along with my colleagues, understand how critically important it is to foster diverse and inclusive workspaces where women can thrive. And, not only is it the right thing to do, it makes good business sense: a 2019 analysis from McKinsey found that "companies in the top quartile for gender diversity on executive teams were 25 percent more likely to have above-average profitability than companies in the fourth quartile." We've put our heads together to come up with a few ways to promote the industry to women, as well as thought starters on how to retain the women already in our ranks. Spread the wordWhile not all areas of the housing sector have had a hard time attracting women – for example, the majority of today's Realtors, 65%, are women – others have, historically, lagged behind. Unfortunately, a general awareness issue could be partly to blame. One way to address this issue could be to increase our visibility in high school and university settings where young women are considering different career paths. Some ideas include calling up your alma mater and asking to speak to a business class about career options and your experience in the mortgage industry, sponsoring your own mentorship program at your workplace, mentoring a young woman who is interested in the mortgage industry, hosting a webinar about mortgage industry career paths and so much more. Additionally, there are many exciting things happening in the industry that could intrigue tech-savvy students who want to work in fast-paced, innovative fields. From hybrid appraisals to AI and machine learning infused throughout the homebuying journey, the mortgage industry has a lot to offer young women. Be visibleAs a woman leader in the industry, it is crucial that you be visible — whether virtually or at in-person events — to others who could be inspired by your experience and career journey. Representation matters and being open and willing to share your experiences with others through speaking engagements at conferences or, even though posts on your own LinkedIn page could serve as source of inspiration to a young woman in your network. For women already moving up the corporate ladder in the mortgage industry, it can be easy for them to feel like an "only" if their organization is lacking women leaders at the top. Hearing your story could be a difference maker for them and encourage them to keep climbing the ladder. Show up for womenFor women, mentorship, sponsorship and allyship is key to making their experiences in the workplace more enjoyable (and equitable). First, understanding the difference between the three is key: —Mentorship. Dedicating your time and sharing career wisdom with a mentee — either through regular meetups or, on a more informal basis — can make a big, lasting impact on their life. I'll never forget some of the sage advice my mentors shared with me over the years. And the best part about mentorship? It's a two-way street. Mentors can also gain a lot from a mentee's perspective, too. —Sponsorship. Have you ever heard the saying "surround yourself with people who would mention your name in a room full of opportunities”? That, in a nutshell, is sponsorship. If you are already in a leadership role and serve in a mentorship capacity to another young woman, be sure to promote and amplify her good work to others who could have a hand in supporting her next big career move. —Allyship. Having strong allies at work can help boost the morale of women employees on the receiving end of that support. Being an ally, or "a person or group that provides assistance and support in an ongoing effort, activity or struggle," per Merriam-Webster, is often used to describe a scenario when a person who is not a member of a marginalized group vocalizes and offers support to that group. Being a vocal ally to women and women of color, and speaking up when you witness microaggressions taking place, is key to "showing" and not just "telling" someone you are their ally. What's more, allyship is more important than ever to women of color: according to the 2021 Women in the Workplace Study, "when women of color have strong allies at work, they are happier in their jobs, less likely to be burned out and less likely to consider leaving their companies." Amy Daniel is a senior vice president within ServiceLink's Default Division. This column does not necessarily reflect the opinion of HousingWire's editorial department and its owners. To contact the author of this story: To contact the editor responsible for this story: The post Opinion: How to attract and retain women in mortgage appeared first on HousingWire. |

| UWM rolls out bank statement loans for self-employed borrowers Posted: 16 Mar 2022 10:54 AM PDT United Wholesale Mortgage (UWM), the nation's largest wholesale lender, announced on Wednesday it will accept personal or business bank statements in self-employed borrowers' loan applications. The step comes as rising interest rates slow the flood of refinances, reduce lenders' origination volume, and companies prepare to boost their non-qualified mortgage (non-QM) products. According to UWM, only self-employed borrowers will be able to send bank statements to qualify for a loan, instead of income documents or tax transcripts. The product is available for loans up to $3 million and up to 90% loan to value. No mortgage insurance will be required. The company said in a statement that the product "will give independent mortgage brokers another competitive edge when it comes to working with non-W2 borrowers." UWM also announced it is extending its no-cost appraisals for primary purchases until the end of April. In January, the company announced a credit up to $600 for borrowers appraisal costs for the next two months. The non-QM sector is expected to take off in a higher interest rate landscape, when lenders are looking to reach borrowers outside Fannie Mae and Freddie Mac‘s credit boxes. How to serve today's unique borrower Today, more borrowers are self-employed, work remotely and have multiple streams of income. HousingWire recently spoke with Bill Dallas, President of Finance of America Mortgage, to discuss how brokers can leverage technology to accommodate today’s average homebuyer. Presented by: Finance of AmericaSelf-employed borrowers and those who work in the gig economy need homes. But current government-sponsored enterprise guidelines make it difficult for these borrowers who don't have a traditional salary to qualify for agency-backed loans. "We are going to see an increase in some of the non-QM lending. I don’t think it’ll ever be a significant chunk. But you need to be able to serve all of these customers," Bob Broeksmit, Mortgage Bankers Association's president and CEO, said on Wednesday morning during the ICE Experience Conference in Las Vegas. Some lenders, however, are closely eyeing regulatory changes that could dampen the non-QM market by expanding the pool of loans able to get QM status. The Consumer Financial Protection Bureau's new General QM Final Rule replaced the 43% debt-to-income ratio limit in favor of more flexible pricing guidelines, allowed jumbo loans to get QM status and provided additional ways to verify income or assets. The new rule is slated to be implemented on Oct. 1, 2022. The post UWM rolls out bank statement loans for self-employed borrowers appeared first on HousingWire. |

| ICE integrates Maxwell and Roostify to eClose solution Posted: 16 Mar 2022 06:00 AM PDT California-based ICE Mortgage Technology announced this week two enterprise agreements to integrate its eClose solution to Maxwell and Roostify platforms, enabling a more streamlined closing process for lenders and borrowers. Encompass eClose will be part of the mortgage fintech Maxwell’s point-of-sale platform. Roostify, a mortgage technology provider, will integrate the solution to its digital home lending platform. Parvesh Sahi, senior vice president of business and client development at ICE Mortgage Technology, said that lenders will have a true digital experience that provides efficiency, speed, and cost savings. "We are making it easy for lenders to adopt automation and start gaining the competitive advantages that come with our eClose solution," Sahi said in a statement. Maxwell connected the popular Encompass LOS to its point-of-sale platform in 2019. But the new partnership will bring the eClosing workflow electronically, securing valuable savings on lenders per loan costs, the company said. "With today's tight margins, lenders need to optimize each step of their process for profitability and success," John Paasonen, CEO and co-founder of Maxwell, said in a statement. Founded in 2015, Maxwell uses artificial intelligence to accelerate the mortgage process for over 300 community lenders, banks, and credit unions. The company claims that they close loans 13 days faster and enable their loan officers to close around 15% more loans per month. Are digital closings really worth it? Many lenders are familiar with digital closings (eClosings), but they might not know just how valuable they can be to their business. A recent study found that digital closings shorten the time it takes to close, reduce errors and increase ROI — all while improving customer experience. Presented by: NotarizeMaxwell looks to digitize the entire mortgage transaction with fulfillment, payments, and due diligence solutions. Through its point-of-sale platform, lenders can synchronize documents, send a notification to borrowers and real estate agents, and manage disclosures. Regarding ICE’s partnership with Roostify, when the closing package is created in the Encompass loan origination system, Roostify's system will be notified, authenticate the task, and send the requirements to the borrower. Borrowers who sign into their lender's instance of the Roostify portal will easily review and sign the documentation directly from the platform. Rajesh Bhat, Roostify's CEO and co-founder, said the goal is "to create a simpler home lending experience that's both smooth and transparent for lenders and borrowers." San Francisco-based Roostify, founded in 2012, said it helped lenders process more than $50 billion in loans each month, among them enterprise banks and independent brokerages. The post ICE integrates Maxwell and Roostify to eClose solution appeared first on HousingWire. |

| Angel Oak Mortgage REIT records solid earnings performance Posted: 16 Mar 2022 05:00 AM PDT Angel Oak Mortgage Inc., a real estate investment trust focused on investing in nonqualified mortgages, announced that it recorded net income of $21.1 million for the year ended December 31, 2021, and $3.1 million for the final quarter of last year, on net interest income of $49.1 million and $16.6 million, respectively. The earnings performance of AOMR in 2021 represents a big bump from 2020, when REIT reported annual net income of only $736,000 on net interest income of $33.3 million. The company's total assets over the period, propelled by loan purchases, also skyrocketed, from $509.7 million to $2.6 billion. "The fourth quarter of 2021 capped off a truly transformative year for the company, as we continued to capitalize on strong demand for non-QM loans [nonqualified mortgages] and the power of the Angel Oak franchise," said the company's president and CEO, Robert Williams. "Since our IPO [in June 2021], we purchased $1.4 billion of loans, bringing our total loan portfolio to over $1.1 billion at year end." AOMR is a publicly traded REIT that is part of Angel Oak Cos., a long-term player in the non-QM mortgage market. It is externally managed and advised by an affiliate of Angel Oak Capital Advisors. AOMR's affiliated mortgage companies are expected to originate more than $7.5 billion in non-QM loans in 2022, compared to $3.9 billion in 2021, the family of companies recently announced. Over the last six months of 2021, since going public, AOMR has purchased $1.4 billion worth of residential mortgage loans, bringing its total portfolio of residential mortgages and other assets to $2.6 billion as of year-end 2021. That represents 77% growth since its June IPO, AOMR's earnings statement reveals. In addition, at year-end 2021, the company was party to six financing lines that allow borrowings in an aggregate amount of up to $1.25 billion. Since year-end, the company has extended the maturity date with respect to multiple facilities and added $50 million of additional committed financing capacity, according to its earnings release. 3 questions lenders should ask before implementing non-QM With refinance volumes anticipated to decrease by 62% this year and many originators experiencing layoffs, lenders are looking for a way to diversify their offerings with non-QM products and gain new business in order to maintain profits. Presented by: Acra Lending"We also completed two residential non-QM securitizations during the year, totaling $703.5 million," Williams said. AOMR also closed on its third sole securitization under the Angel Oak Mortgage Trust (AOMT) shelf in late February — a $537.6 million offering. A total of some $4 billion in securitization volume across 10 deals has been completed through the AOMT shelf since March 2021, data from Kroll Bond Rating Agency shows. That includes the three sole securitizations — valued at $1.2 billion — that were completed since this past June by the Angel Oak Cos. public REIT, AOMR. The REIT declared a fourth-quarter 2021 dividend of $0.45 per share, which is payable on March 31 to shareholders of record on March 22. "We are pleased with our accomplishments in our first year as a public company, benefiting from the support of the Angel Oak platform, and remain steadfast in our charge to deliver attractive, risk-adjusted returns for our shareholders as we execute on our long-term strategic growth plans," Williams said. Angel Oak Mortgage Solutions recently announced that it is allowing short-term rental properties as eligible collateral for its investor cashflow program, though it is not permitting “condotels” to be used as collateral. The post Angel Oak Mortgage REIT records solid earnings performance appeared first on HousingWire. |

| Mortgage applications drop as rates spike Posted: 16 Mar 2022 04:00 AM PDT Interest in residential mortgages fell 1.2% for the week ending March 11 as mortgage rates rose to their highest levels since May 2019, according to the Mortgage Bankers Association‘s latest survey. "Mortgage rates continue to be volatile due to the significant uncertainty regarding Federal Reserve policy and the situation in Ukraine,” said Joel Kan, associate vice president of economic and industry forecasting for the MBA. “Investors are weighing the impacts of rapidly increasing inflation in the U.S. and many other parts of the world against the potential for a slowdown in economic growth due to a renewed bout of supply-chain constraints." Mortgage rates, which recently hit 4.27% for 30-year-fixed rate mortgages, are now a full percentage point higher than a year ago. That’s led to a significant decline in refinance activity, both for conventional and government loans. According to the MBA, refi applications fell 3% from the prior week and were down 49% from a year ago. The seasonally adjusted purchase index increased 1% from one week earlier; the unadjusted purchase index increased 2% from the prior week but was 8% lower than the same week a year ago, largely due to a decline in inventory. "Purchase applications slightly increased, with both conventional and VA loan applications seeing gains,” said Kan. “The average purchase application loan size remained elevated at $453,200 – the second- highest amount in MBA's survey." The MBA found that the adjustable-rate mortgage share of the activity increased to 5.6% of total applications. Lenders, are you prepared for 2022's challenges? As lenders navigate through increased competition and fraud risk, it's crucial they find solutions that balance workflow improvement. Presented by: DataVerifyThe FHA share of total applications remained unchanged at 8.7% from the week prior, and the share of VA applications increased to 10.5% from 10.4%. The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $647,200) increased to 4.02% from 3.79%, with points decreasing to 0.37 from 0.39 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week. The survey showed that the refi share of mortgage activity decreased to 48.4% of total applications last week, from 49.5% the previous week. The post Mortgage applications drop as rates spike appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment