Mortgage – HousingWire |

- Inside the Walmart, Lenders One mortgage deal

- Impac Mortgage Holdings increasingly bets on non-QM

- What about mortgage application fallout rates?

- Inside Fairway’s bold plan to boost reverse purchase business

- Opinion: Affordable lending requires creative thinking

- As the market turns, Guild says it’s better prepared than its rivals

- Fannie Mae: Policymakers should look elsewhere to improve affordability

- Why owning a home is the best hedge against inflation

- LoanDepot restructuring creates new digital products/services unit

- Lakeview readies rare securitization backed by nonperforming mortgages

| Inside the Walmart, Lenders One mortgage deal Posted: 11 Mar 2022 02:40 PM PST  Lenders One Cooperative and Walmart want mortgages in your shopping cart. On Monday, the cooperative announced that it has struck a deal to lease space in Walmart stores to sell purchase mortgages, refinances, and home equity loans. Lenders One did not disclose the financial terms of the contract. This is not the first deal amongst mortgage lenders and big-box retailers: Costco has a partnership with Ohio-based CrossCountry Mortgage, which in 2020 acquired First Choice Loan Services, inheriting Costco’s mortgage program. But the Lenders One deal is structured quite differently, so let’s break it down. The negotiations between Lenders One and Walmart started more than a year ago. During the process, it became clear that the retailer was resistant to leasing its space for only one mortgage lender, said Justin Demola, president of Lenders One Cooperative. “We don’t believe they would give it to a single mortgage company, based upon what discussions we’ve had over the past 18 months or so,” he told HousingWire. Leasing retail store-within-a-store spaces to a range of different mortgage lenders is a way of diversifying risk – should one lender faces financial difficulties, the others can keep doing business. The cooperative's value proposition is it can bring more financial stability in dealing with different mortgage lenders at the same time, Demola said. Lenders One will be responsible financially for the leases. However, the cooperative will sublease the space to its members interested in offering their mortgage products to Walmart customers. “They came to us because of our size, scope, and structure,” Demola said. Founded in 2000, Lenders One Cooperative has a network of more than 250 independent mortgage bankers, banks, credit unions, correspondent lenders, and suppliers of mortgage products and services. The platform is managed by a subsidiary of Altisource Portfolio Solutions, a service provider and marketplace for the real estate and mortgage industries. The cooperative members cover the entire lending spectrum, originating between $50 million and $25 billion per year. Collectively, their origination volume reached around $780 billion in 2020. Rocket Mortgage, the largest mortgage lender in America, originated about $320 billion in 2020. Walmart branches will have a Lenders One brand identification but refer to the mortgage lender as the provider of products and services. Demona said whichever co-op member chooses a location first and shows it can begin doing business will operate the branch. “It is like our children – all members are equal,” he said. Why sell mortgages in Walmart stores? Most of Lenders One’s members have a branch-centric model and are purchase-oriented, a good thing considering the current mortgage environment. Owing to a rapid increase in mortgage rates, the Mortgage Bankers Association believes 2022 and 2023 will predominantly be strong purchase years for the mortgage industry. Of the $2.60 trillion forecast to be originated this year, 67% is expected to be purchase. In 2023, 73% of mortgages in America are expected to be for new home purchases, according to the MBA. The cooperative’s aim is to make members more profitable, reduce costs, and increase efficiencies to compete with the larger, well-funded mortgage originators in the country. “One of the things that our members have asked for is helping them get better execution on the sale of their loans,” said Demola. “But for the first time, we’re helping our members fill the top of their sales funnel with potential borrowers to purchase or refinance a home.” In this first phase, Lenders One inked deals for three Walmart locations in Florida and New Jersey. The target is to reach 20 Walmart stores by the end of 2022, Demola said. The lenders will start offering purchases, refinances, and home equity but expect a fully diversified product set for Walmart customers. By setting up stores within Walmarts, Lenders One members would be putting their products in front of a diverse customer base. That could be helpful in avoiding fair lending claims through state Community Reinvestment Act (CRA) laws, Demola said. “We feel Walmart will give our members an advantage when it comes to answering questions from regulators to put themselves in markets that they may not normally be in for fair lending.” Demola said that the Walmart deal is just the start. Partnering other retail companies is not off the table. “This is a very large, detailed project. It’s not necessarily easy. We are in a pilot phase. So, we want to see proof of concept. If we succeed here, I believe that we can duplicate it in other retailers.” The post Inside the Walmart, Lenders One mortgage deal appeared first on HousingWire. |

| Impac Mortgage Holdings increasingly bets on non-QM Posted: 11 Mar 2022 01:39 PM PST  Despite significant market volatility, nonbank lender Impac Mortgage Holdings appears to be long on non-QM. The California-based company reported non-QM originations of $382.1 million in the fourth quarter, roughly double that of the third quarter, and positioned the company for an annualized run rate of approximately $1.5 billion. In total, Impac originated nearly $700 million in non-QM mortgages in 2021, more than double 2020’s output. “Further context, the company originated less than $15 million in NonQM in the four quarters post-COVID in the second quarter of 2020 through the first quarter of 2021,” company CEO George Mangiaracina said on the earnings call Thursday. The non-QM boost came at a time when Fannie Mae and Freddie Mac-backed originations fell to $377 million – down from $497 million in Q3 – and margin compression took its toll on the company’s balance sheet. However, Mangiaracina told investors that the non-QM segment of the mortgage market experienced “significant market pressure” beginning in the fourth quarter of 2021, with conditions deteriorating in the first quarter of 2022. “Expectations related to rising short-term interest rates, as expressed in the two and three year swap rates have resulted in concerns over extension risk and more expensive structured financing terms,” he said. Mangiaracina added: “The company continues to believe that the addressable market for NonQM will expand once markets normalize.” In total, Impac posted a net profit in the fourth quarter of $3.6 million, a sequential improvement of nearly 72% from the third quarter, which executives attributed to a change in the fair value of net trust assets and long-term debt. Total net revenue checked in at $14.9 million, a decline from the $19.8 million in revenue reported in the third quarter. Mangiaracina cited Russia’s invasion of Ukraine as the cause of widespread challenges for Impac Mortgage Holdings. “Some of us were cutting our teeth in the business back in October of 1998, at the advent of the Russian debt crisis, which triggered a flight to safety rally in US treasuries and a concurrent sell-off in credit-based assets,” he said. “Especially, finance companies at that time experienced losses and liquidity calls on their Treasury short hedge positions and also faced warehouse margin calls and market value declines in their subprime and loss gain mortgage loan portfolios.” The challenges will force Impac to tinker with its hedge strategies, namely Treasury swaps and forward sale agreements in lieu of aggregating non-QM for bulk sale. “We will continue to remain disciplined in our origination and capital markets activities and remain undeterred in our belief that the addressable market for NonQM will expand to our benefit once markets normalize with respect to volume and margin,” Mangiaracina said. As for agency product, which is primarily originated from Impac’s direct-to-consumer call center, things will get worse before they get better. “We anticipate that market conditions will continue to be challenging for the foreseeable future in our rates business and have adjusted our capacity models, marketing spend and headcount accordingly,” Mangiaracina said. The post Impac Mortgage Holdings increasingly bets on non-QM appeared first on HousingWire. |

| What about mortgage application fallout rates? Posted: 11 Mar 2022 12:12 PM PST As lender concerns about margin compression rise, why aren't we seeking to better understand our mortgage application fallout rates to increase revenue? For mortgage originators of all sizes, "fallout" is a word that induces headaches and nausea at roughly the same level as terms like "repurchase demand" or "regulatory audit." We don't often talk about it, but it's a fact of mortgage lending. Far too many loan applications never make it to closing, falling out of a lender's pipeline even after rate lock. And far too often, the response is a shrug of the shoulders and back to work finding new leads. The MBA's Quarterly Mortgage Bankers Performance Report for the first quarter of 2021 tells us that "the average pull-through rate (loan closings to applications) was 76% in the first quarter, down from 78% in the fourth quarter [of 2020]." So, mortgage lenders saw 24% of loan applications received fall out of their pipelines before closing. The same report tells us that "total loan production expenses – commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations – increased to $7,964 per loan in the first quarter, up from $7,938 per loan in the fourth quarter. From the third quarter of 2008 to last quarter, loan production expenses have averaged $6,621 per loan." It remains expensive to produce a loan, and it's even getting more expensive.As the overall mortgage market begins to shift from one dominated by refinance volume to one dominated by purchase mortgage volume — especially with some decline in overall volume expected —we're already hearing about margin compression. Discussion will revolve around how lenders can better compete for market share; or how lenders can use technology or other strategies to attack the production costs seemingly rising to meet declining revenue. All of this is merited and even prudent. Are you analyzing and attacking fallout ratesWhy aren't more lenders seriously considering more systemic and consistent ways to analyze and attack mortgage application fallout rates, perhaps even finding ways to recapture (or never lose in the first place) their wayward applicants? Wouldn't this be a productive and effective way to nudge volume and revenue upward? There is no warmer sales lead than a loan application. For the thousands (or even millions) lenders spend on creating new leads through lists, marketing campaigns and networking, there's obviously no greater sign of interest in a lender's product than a loan application. And yet, most lenders know little to nothing about why applicants are bailing out on their products before closing. Instead, they go back to the start, casting new nets for colder leads. As an industry, we've upped our game (although there's more to be done) in two areas of the transactional process. First, it's admittedly much easier for a potential borrower to apply in the first place. Any number of online solutions allow borrowers to shop rates and lenders online, not to mention adding lending marketers and loan originators (LOs) to identify solid leads. Second, although the overall mortgage process has a long way to go, loan origination systems (LOS) technology has advanced rapidly in just a few years, better integrating with other elements of the tech stack and automating a number of functions that not long ago were manual or shopped out to third-party providers. The result has been a better overall mortgage lending process. We have a long way to goOne of the glaring shortfalls in terms of technology adoption in our industry is the use of technology to support the consumer experience. While other industries push forward to make closing a transaction as easy as the initial shopping, our industry still tends to rely on telephones, emails, letters and third parties to attend to the consumer as they wade through the complexities of closing a loan. One extension of that shortfall applies directly to mortgage application fallout rates. We tend to assume that when an applicant drops out of the process, that applicant has either found a better rate or decided not to pursue the transaction at this time. But more lenders than not don't actually verify that systematically. No survey. No follow-up. No solution to automatically measure variables indicating any kind of pattern in the type of applicant that tends to fall out, and where in the process that happens. While it's likely that market movement or changed life circumstances could make up a significant number of lost applications, many lenders don't take the time or effort to find out, choosing instead to apply their marketing dollars and investments to procuring and converting cold leads. This would seem to fly in the face of an avalanche of existing research that it's easier and more profitable to keep an existing client (or a lead familiar with your brand) than to find a new one. We know, for example, that increasing customer retention rates by 5% increases profits by 25% to 95%, according to research done by Frederick Reichheld of Bain & Company. It wouldn't be a stretch to apply that same principle to loan applicants who fall out of the mortgage pipeline if the lender better understood why that fall out occurred. All indications are that the mortgage industry will be a far more competitive space in 2022. Many lenders are already gearing up their marketing machines to win new borrowers as origination volume leans more toward purchase mortgages. Competition often drives innovation, and in this purchase market, it would seem that comprehensively addressing lenders' fallout rates would be as worthy as any other marketing investment, if not more so. This column does not necessarily reflect the opinion of HousingWire's editorial department and its owners. Jim Paolino is CEO and Co-Founder of LodeStar Software Solutions. To contact the author of this story: To contact the editor responsible for this story: The post What about mortgage application fallout rates? appeared first on HousingWire. |

| Inside Fairway’s bold plan to boost reverse purchase business Posted: 11 Mar 2022 11:46 AM PST Last week, Fairway Independent Mortgage Corporation announced the hiring of Tane Cabe as its new reverse business development manager with a focus on Home Equity Conversion Mortgage (HECM) for Purchase (H4P) business. In relation other top 10 reverse mortgage lenders, Fairway stands out by making a concerted effort to cultivate more H4P business in an environment where many other reverse mortgage companies have spent much of the past 12-18 months focused on HECM-to-HECM (H2H) refinances, according to data compiled by Reverse Market Insight (RMI). H4P is a major company initiative for Fairway, which hopes to increase its reverse for purchase volume in the short-term with hopes of transformation in the space over a 10-year period, and with a level of speed the lender claims is unmatched in the H4P arena compared to competitors. To get a better idea about how big a role H4P will play in Fairway's plans, RMD sat down with its National Reverse Mortgage Director Harlan Accola and its National Reverse Sales Training Specialist Dan Hultquist to learn more about H4P's importance to Fairway's future plans. Diagnosing low H4P uptakeAccording to data compiled by RMI, total share of H4P volume across the entire reverse mortgage industry made up only 4.2% of all endorsements in 2021. Because Fairway gets most of its reverse mortgage business from referral partnerships, extending to the purchase market made sense for Fairway because of the partnerships that its loan officer corps has spent so much time developing, according to Hultquist.  "Most of our loan originators have built referral partnerships over decades in some cases," Hultquist says of Fairway’s LO corps. "And so, they know the local real estate agents. A lot of the business in our industry is generated through call centers, but call centers don’t have the ability to build relationships with local real estate professionals. Some of them have boots on the ground [and] feet on the street. But for the most part, we already have those relationships, so it’s natural for us." Since a lot of reverse mortgage business is generated using call centers, that creates a natural aversion for some real estate agents to even engage with the reverse mortgage category, Accola adds. "Real estate agents hate dealing with call centers," he says. "[They also] don’t like FHA loans, because now that creates the amendatory clause, and more inspections and stuff like that. So real estate agents automatically get nervous [about a HECM being] an FHA loan. And then, they get nervous if somebody is trying to do this loan from a phone room somewhere who doesn’t have as much skin in the game as somebody that’s in the community that they can see by going over to their office." As with many aspects of the reverse mortgage industry, it also comes down to general awareness, Hultquist adds. Not only are real estate agents largely unaware of the fact that the H4P program exists, but they are also underinformed when it comes to the HECM program itself. Fairway H4P: differentiation through speedSome other leading reverse mortgage lenders maintain that H4P uptake will continue to be low until real estate professionals and home builders can come to understand that such loans need to take a longer time to originate. However, Fairway says that in order to be competitive with its forward mortgage business arm, they can close their H4P loans in as few as 17 calendar days instead of the more typical 45-60 day timeframe.  "Fairway has several things in place which allow us to move that fast," Hultquist says. "Our referral partnerships are set on the forward side as well, and we have to protect those partnerships. So if there’s a HECM for Purchase, they’re alerted immediately. Our operations team has streamlined it to the point where we can do it, even sometimes with a second appraisal coming through. Now, we can’t do it every time. But the goal is to close it in 17 days, except in North Carolina, which you can’t by law." Due diligence is also a priority for Fairway, Hultquist says, and certain necessities are encouraged by the lender. "We also enforce certain protocol for purchase transactions," he says. "For instance, why would you wait to get your counseling done while you’re looking for a house? Get your counseling completed. We insist that if a client is looking at buying a home, get the counseling done and get it done today. Because we don’t want to take an application, send them out the counseling instructions, and then have another week’s delay. We can’t afford it if we’re going to stick to 17 days." Competitiveness in U.S. real estate marketsBecause of the reality in real estate markets across the country, speed is of paramount concern in order to make a reverse purchase a viable consideration when competing with buyers who may have cash on hand for a home purchase, Accola explains. "The issue is that must be done [quickly], especially in a competitive market," he explains. "Who’s going to accept a [slower H4P] offer when they’ve got cash offers and forward offers that will close in three weeks? We can't [make an offer that will take] six or eight weeks." The nature of competition among homebuyers necessitates a quicker approach in H4P business and informs the headway that Fairway has made in this segment, Accola explains. "The reason that we came up with a 17-day [timeline] was not to compete with anybody else, it was to compete with our forward side because that side is fast," Accola says. "And so, we couldn’t get our loan officers to talk about reverse purchases because if it took 45 to 60 days, they wouldn’t talk about it. One of our 10 values is speed. And so, we’re very concerned about closing on time and getting the documents there before, so we’ve closed hundreds of them in 17 days or less." Look for more about Fairway's efforts in H4P business next week on RMD. The post Inside Fairway’s bold plan to boost reverse purchase business appeared first on HousingWire. |

| Opinion: Affordable lending requires creative thinking Posted: 11 Mar 2022 07:51 AM PST Each fall, trendsetters at Pantone decide on the next year's "color of the year," which they feel will define and influence the upcoming year. Whether the "color of the year" is a self-fulfilling prophecy or the trendsetters really are that on trend is currently unknown. Similarly, the mortgage industry has no shortage of trend predictions being made each month, quarter and year. Unfortunately for lenders, these are never anything more than predictions as only time will tell how the markets will play out. However, the mortgage industry is facing a shift in trend predictions this year, as experts unofficially name a "color of the year" in mortgage. Current buzzwords in the mortgage industry include affordable, underserved, accessible and equity. With the increasing regulatory focus on expanding affordable lending programs, mortgage lenders need to have a plan to serve the underserved. Many lenders have historically shied away from offering a robust affordable lending product line, including down payment assistance (DPA) programs and ITIN mortgages. Surprisingly, risk isn't the main factor affecting lenders' appetite for DPA and affordable lending products today. What's really holding lenders back are the challenges associated with DPA and affordable lending products. Owning a house with the white picket fence may be a key part of the American dream, but lenders still need to make money in order to stay in business. At the end of the day, there must be a better balance between doing good for their communities and themselves at the same time. Finding the 'why' The benefits of a lively and contemporary DPA and affordable lending program are far-reaching and untold, brightening the lives of many. However, those terms don't always reflect well on a profit and loss statement, and many lenders need to define the benefits of offering these programs in terms other than pure numbers. While not the most altruistic motivation, meeting regulatory expectations is one advantage to offering DPA and affordable lending programs, as this would help align lenders with current federal-level directives to address the racial homeownership gap. How Mortgage as a Service Levels the Playing Field for Minority and First-Time Homeowners This white paper explores the benefits of closing the homeownership gap, systemic mortgage industry issues, and how Salesforce is partnering with Rocket Mortgage to enable mortgage as a service and increase minority and first-time homeownership. Presented by: SalesforceThrough DPA and affordable lending programs, lenders have an expanded ability to fulfill their desire to help low-to-moderate income borrowers obtain the goal of homeownership, but these programs also allow lenders to reach borrowers that may otherwise be ignored or rejected, which can be the key to success in a contracting market. For some lenders, this could mean introducing new products, such as ITIN mortgages, aimed at providing homeownership opportunities to non-U.S. citizens with an ITIN, or individual tax identification number. As evidenced by these two examples, doing good while deriving value need not be mutually exclusive aims when it comes to offering DPA and other affordable lending programs. Where the rubber meets the roadblock For many lenders, the challenges of offering DPA and affordable lending programs have long outweighed the potential benefits. The most prevalent arguments against DPA and affordable lending programs are they're hard to do and require an inordinate amount of resources, ultimately resulting in nearly no profit for the lender. Additionally, state housing finance authorities are the primary sources of most DPA and affordable lending programs, resulting in 50 different programs and 50 different sets of guidelines. Those 50 different guidelines lead to confusion, errors, delayed closings and lock extensions, all of which cost the lender money. While Ginnie Mae loan programs offer another avenue for lenders to offer loan programs geared towards low-to-moderate income borrowers, the onerous approval process to become an approved Ginnie Mae issuer make this strategy a non-starter for many lenders. Thus, lenders need to think beyond the obvious strategies and outlets if they truly want to add DPA and affordable lending programs to their product line-up. Think outside the box One emerging source for DPA and affordable lending products is the correspondent channel. Correspondent programs are often well suited to offer these programs because they can go deeper and wider in credit offerings than state programs while still fitting Fannie Mae and Freddie Mac requirements. Furthermore, correspondents are in a position to minimize overlays on DPA and affordable lending products, making them more efficient and more profitable. One common misconception is that DPA and affordable lending products can only be used for low-income borrowers. With expanded credit offerings, these products can help a multitude of next gen borrowers. Loan originators need to fully understand their options and how to get creative within the programs in order to help their borrowers. For example, some DPA programs are based off the area or state median income (AMI or SMI), not the borrower's income. With a DPA program based off AMI and an informed loan originator, a recent pharmacy school graduate with a 620 FICO score and a salary of $128,000 could purchase their first home with a DPA program. Yet, a less informed loan originator could think this borrower is not eligible for any of the state-sponsored DPA programs due to their income and look no further. The goals of expanding homeownership and closing the racial gap in homeownership have taken center stage in the mortgage industry of late. As affordable housing becomes the topic that defines and influences the industry this year, lenders will have to reevaluate their DPA and affordable lending programs and get creative. Roland Weedon is president and CEO of Essex Mortgage. This column does not necessarily reflect the opinion of HousingWire's editorial department and its owners. To contact the author of this story: To contact the editor responsible for this story: The post Opinion: Affordable lending requires creative thinking appeared first on HousingWire. |

| As the market turns, Guild says it’s better prepared than its rivals Posted: 10 Mar 2022 03:36 PM PST  California-based Guild Mortgage can be added to the growing list of lenders with waning profitability. But Guild’s executives believe the retail lender is well positioned to succeed in a lower-volume environment, whether it’s organically or through acquisitions. The nonbank mortgage lender increased its total originations in 2021, despite a reduction in the fourth quarter. But margins under pressure due to higher rates reduced the company’s earnings. Guild, a purchase-focused lender with a distributed retail model, reported on Thursday a $36.8 billion in origination volume in 2021, up 5% from 2020, with purchases representing 54.6% of the total. In the fourth quarter, volume checked in at $8.8 billion, down 15% year-over-year and 12% quarter-over-quarter, with a 62% purchase mix. The gain-on-sale margin on originations declined from 5% in 2020 to 4.02% in 2021, but at the end of the fourth quarter, it had fallen to 3.47%, generally consistent with industry trends. The company’s net income declined to $283.8 million in 2021 from $370.6 million in 2020, a 23% decrease. The profit plunge was especially pronounced in the fourth quarter, where it was down 46% year-over-year and 41% quarter-over-quarter, to $42.2 million. Though profits have shrank, executives asked analysts to look at Guild in relation to its competitors. “Compared to 2020, consistent with the industry trends, sales margins softened, but we maintained higher margins relative to those typically generated in the wholesale or correspondent channels, in part driven by our focused product,” Mary Ann McGarry, Guild’s CEO, said in a conference call. She added: “Some of our peers have recently started shifting focus to purchases. We have been building the scale, relationship, and expertise in purchase over the last years.” Part of the profit in 2021 came from the servicing portfolio. The company’s unpaid principal balance increased 18% last year to $70.9 billion, partially offsetting a decline in originations. “Our underlying servicing portfolio consists primarily of MSRs originated through our retail channel. In 2021, we retained servicing rights for 84% of total loans sold,” Terry Schmidt, Guild’s president, told analysts. According to Schmidt, the company notched a 22% increase in total servicing fees in 2021. Guild had $243 million in cash and $1.5 billion of unutilized loan funding capacity as of December 31, 2021. The liquidity, according to executives, may support mergers and acquisitions, mainly targeting businesses that have a decent market share in their areas, so Guild can keep its focus on building local infrastructure. “While we remain focused on funding originations and reinvesting in the business, we maintain ample excess cash to capitalize on strategically and financially compelling M&A opportunities, as we have done in the past, most recently with the RMS acquisition,” Amber Kramer, Guild’s CFO, said during the conference call. In May, Guild announced the acquisition of Maine-headquartered retail lender Residential Mortgage Services Holdings for $196.7 million. The target company, founded in 1991, had 70 offices across 14 New England and Mid-Atlantic states. For the first two months of 2022, Guild delivered $3.9 billion in loan originations, at a gain on sale margin of 4.15%. Kramer said during the conference call that the company is seeing competitive pressures on margins but is looking at a locally disciplined pricing approach to remain competitive. Guild shares closed on Thursday at $11.59, down 2.28% from the prior day. The stocks were up 2.94% in the aftermarket following the earnings report. The post As the market turns, Guild says it’s better prepared than its rivals appeared first on HousingWire. |

| Fannie Mae: Policymakers should look elsewhere to improve affordability Posted: 10 Mar 2022 02:26 PM PST  How much does a typical low-income first-time homebuyer with a Fannie Mae-backed mortgage bring to the closing table? According to Fannie Mae, in a working paper entitled “Mortgage costs as a share of housing costs—placing the cost of credit in broader context,” the average low-income, first-time homebuyer has about $28,000 for a down payment. The typical low-income first-time homebuyer with a Fannie Mae-backed mortgage also has a 747 credit score, the research paper shows. That's significantly higher than 670, the average score of first-time homebuyers with an FHA-backed mortgage, or 677, the average FICO score of a Black borrower in 2021. In 2020, about 4% of Fannie Mae-acquired purchase loans went to Black borrowers. Mark Palim, Fannie Mae deputy chief economist, said that he preferred not to "speculate" on "alternative borrower" profiles, and that the credit score in the profile is drawn from only those loans that were delivered to Fannie Mae in 2020. "If you look at the credit profile, these are really strong loans in terms of credit score dimension," Palim said. "I would be very happy with that credit score." Palim also noted that the research did not break out borrower profiles further, to examine pricing for Black borrowers or low-income borrowers with lower credit scores, because the search sought to explain complex concepts to people in disciplines other than housing, such as urban planning. "We felt this was already a lot of detail for them to absorb, so we stayed at a high level for these groups," Palim said. An affordable housing advocate, who requested anonymity, called the report “stunning,” because it indicates Fannie Mae is only lending to low-income borrowers with the most pristine of credit histories. "A low-income credit score of 747 is an indictment," the person said. Several fair housing experts interviewed declined to speak on the record, citing the need to study the report more closely. Some raised initial concerns, however, that the research does not include a fair lending analysis, did not break out borrower profiles by race, and focused on long-term housing costs, which is outside of Fannie Mae's sphere of influence, rather than initial access to credit, of which it is a major driver. Palim said that a fair lending analysis was outside of the scope of the research paper. While the researchers cite a number of outside experts it consulted, including the American Enterprise Institute and economists from both the Federal Housing Finance Agency and Fannie Mae, it did not consult with any fair lending experts. An FHFA spokesperson declined to comment on the research. The paper argues that while mortgage costs — including mortgage insurance, guaranty fees and loan-level price adjustments — are often the focus of policymakers looking to address affordability, other costs make up most of the overall cost of housing. The Fannie Mae research shows that guaranty fees, including loan-level price adjustments, make up about 4% of the total cost of homeownership. Private mortgage insurance makes up about one to three percent of total costs, the report found. Policymakers have focused on mortgage costs as a tool to increase credit availability for low-income borrowers and borrowers of color. Instead, according to Fannie Mae researchers, policymakers should turn their attention to other drivers of housing costs besides mortgage costs. "First, our decomposition shows that policy efforts to ameliorate housing costs would be most effective by focusing on ways to reduce the largest components of overall costs," the researchers write. "For ongoing non-mortgage costs in particular, expanding programs that help to reduce utility costs and limit property tax burdens for low-income households are obvious solutions." The federal government has no simple mechanism to reduce local property taxes or utility costs. The FHFA, which under Acting Director Sandra Thompson has had a renewed focus on affordability, has already taken a number of steps to address affordability through its oversight of the GSEs. Those steps include requiring the GSEs to submit equitable housing finance plans, and rejecting its Duty to Serve underserved market plans. Thompson's plans to address affordability also include a holistic review of GSE loan pricing. In January, FHFA said it would increase fees for second home loans and high-balance conforming loans. Upfront fees for high balance loans will increase between 0.25% and 0.75%, tiered by loan-to-value ratio. For second home loans, the upfront fees will increase between 1.125% and 3.875%, also tiered by loan-to-value ratio. The increases are set to take effect in April. Bob Broeksmit, CEO of the Mortgage Bankers Association, said at the time the pricing changes "should provide an opportunity for the GSEs to lower fees on the mission-centric portions of their businesses that primarily serve first-time and low- to moderate-income borrowers." Palim said that he "always hopes research informs policy decisions," but that the research, which he started in 2018, was not prompted by FHFA or related to the review of GSE loan pricing. The post Fannie Mae: Policymakers should look elsewhere to improve affordability appeared first on HousingWire. |

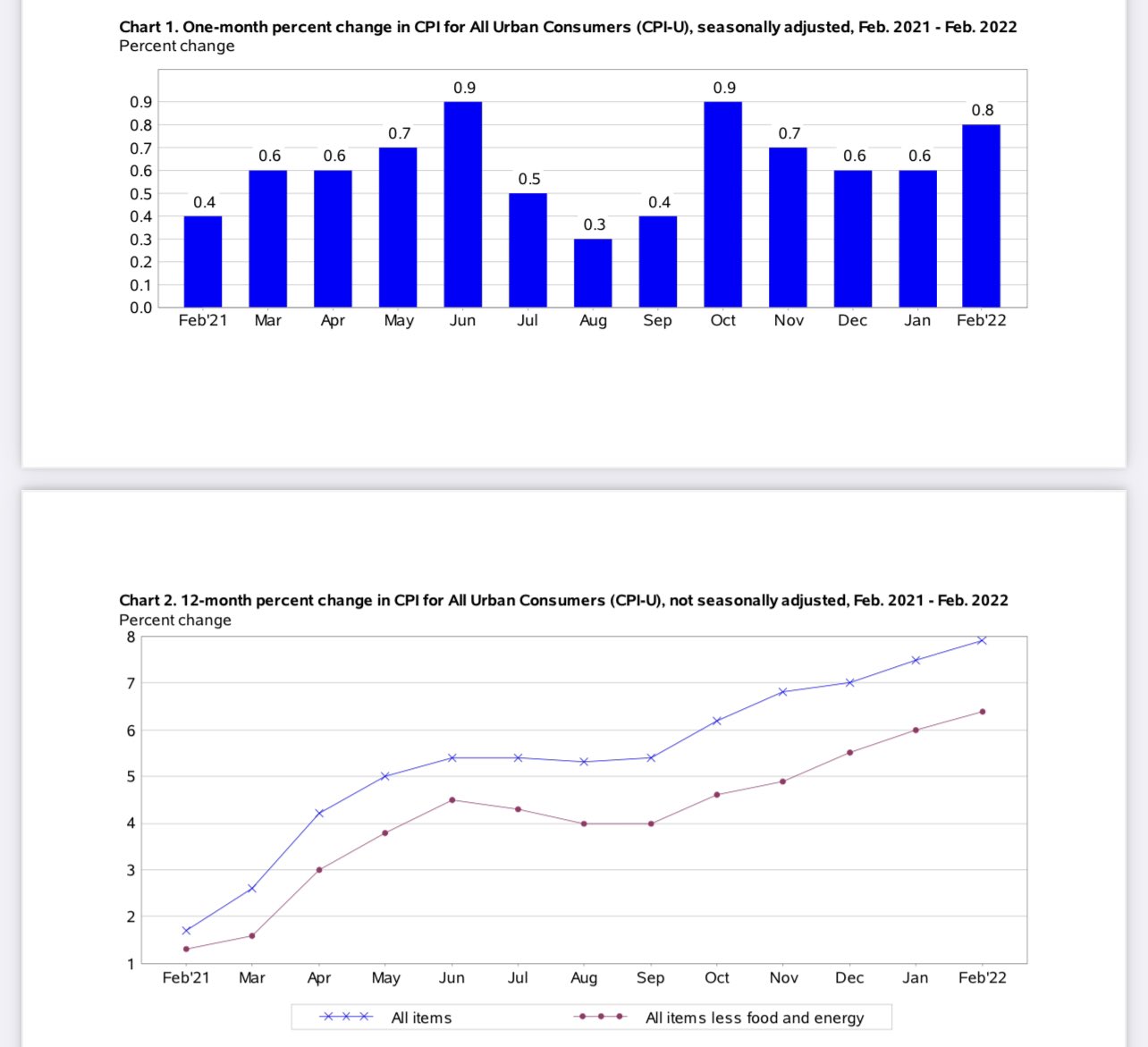

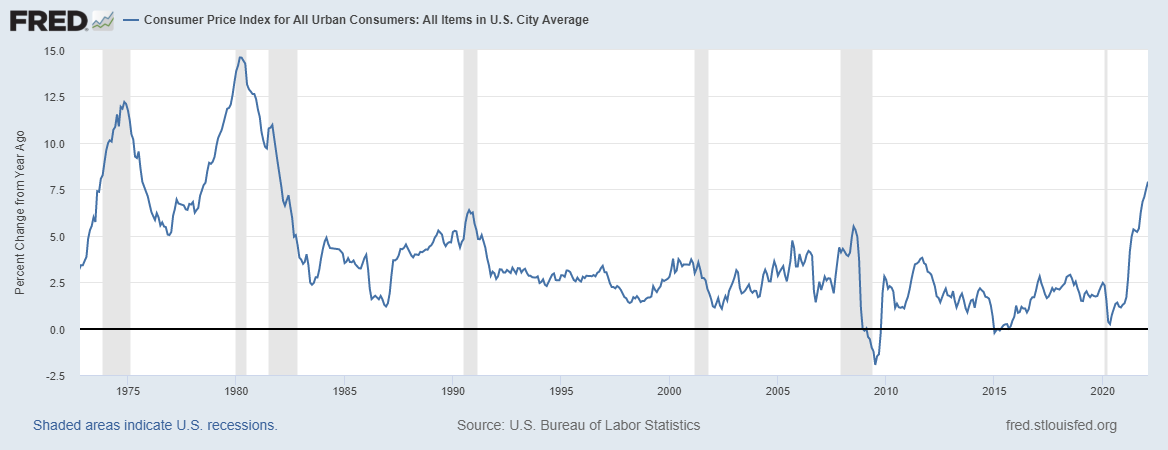

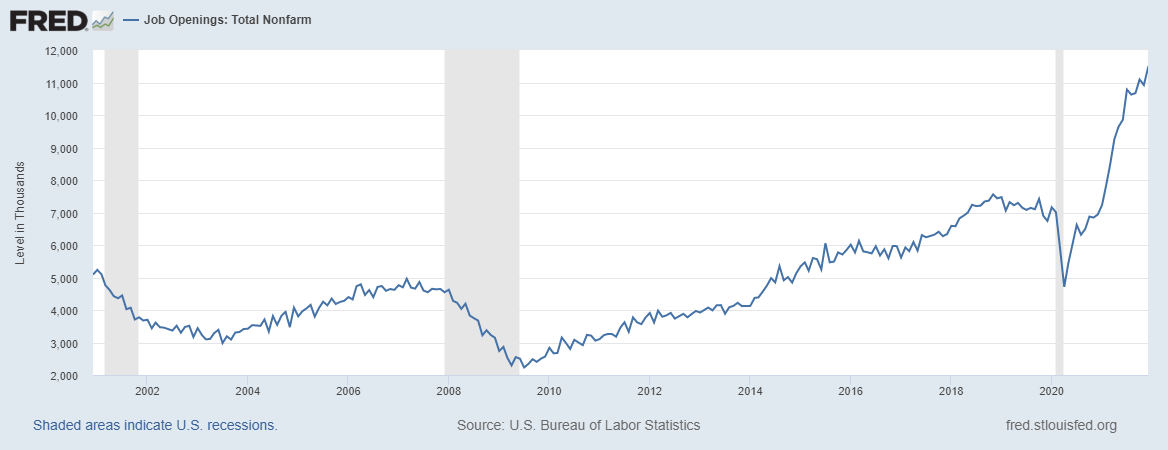

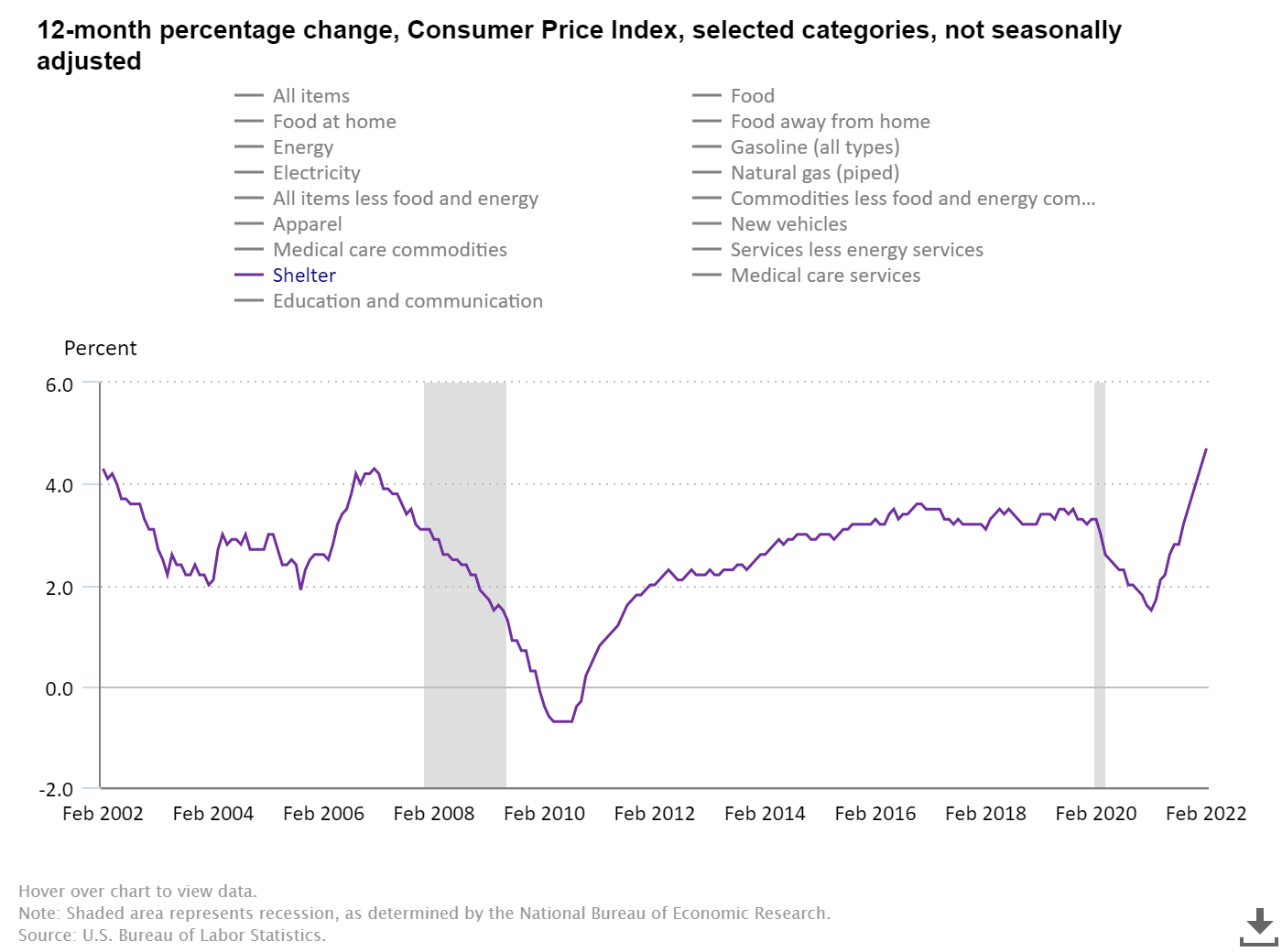

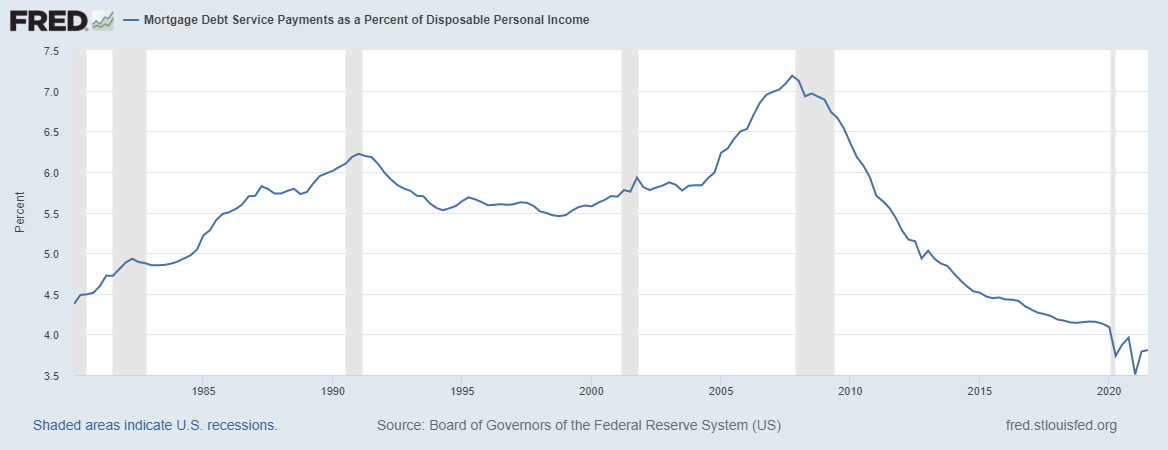

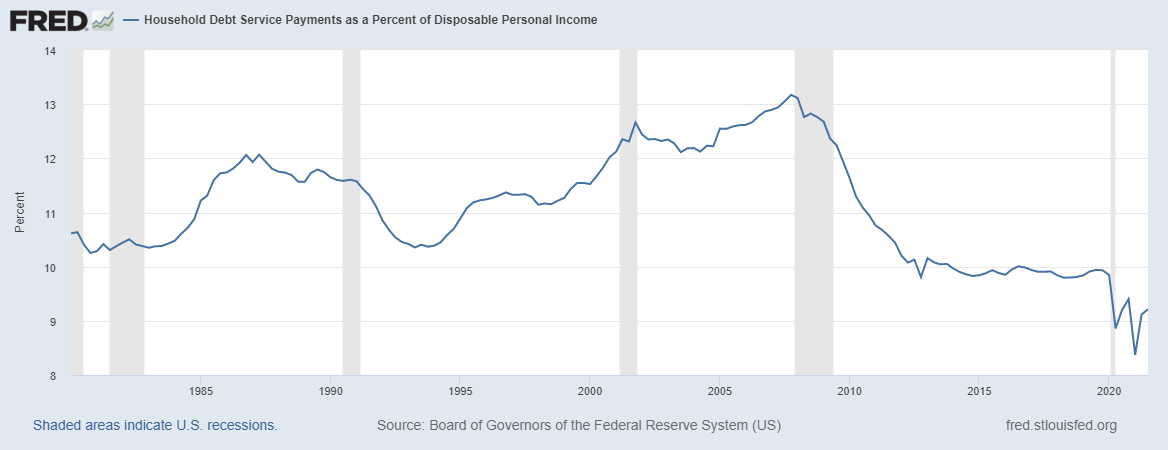

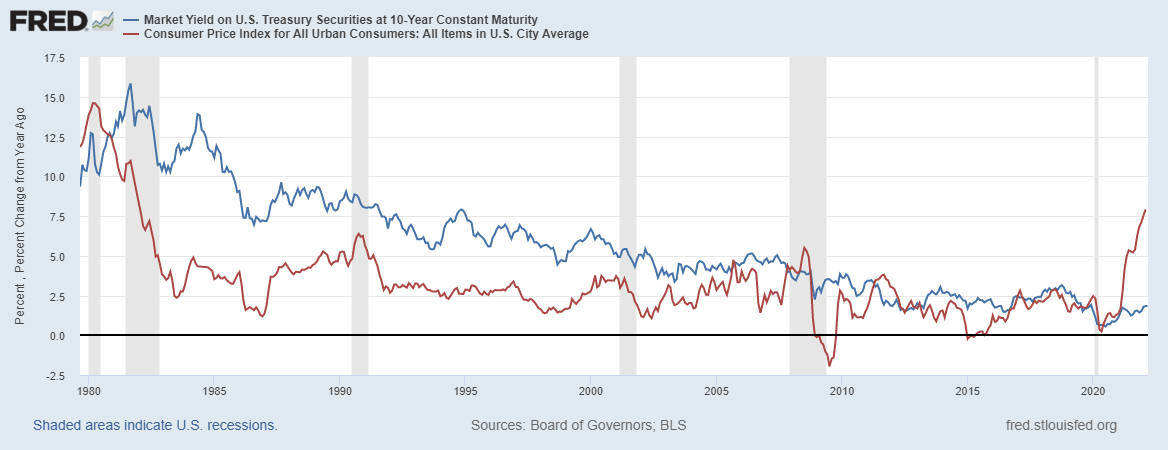

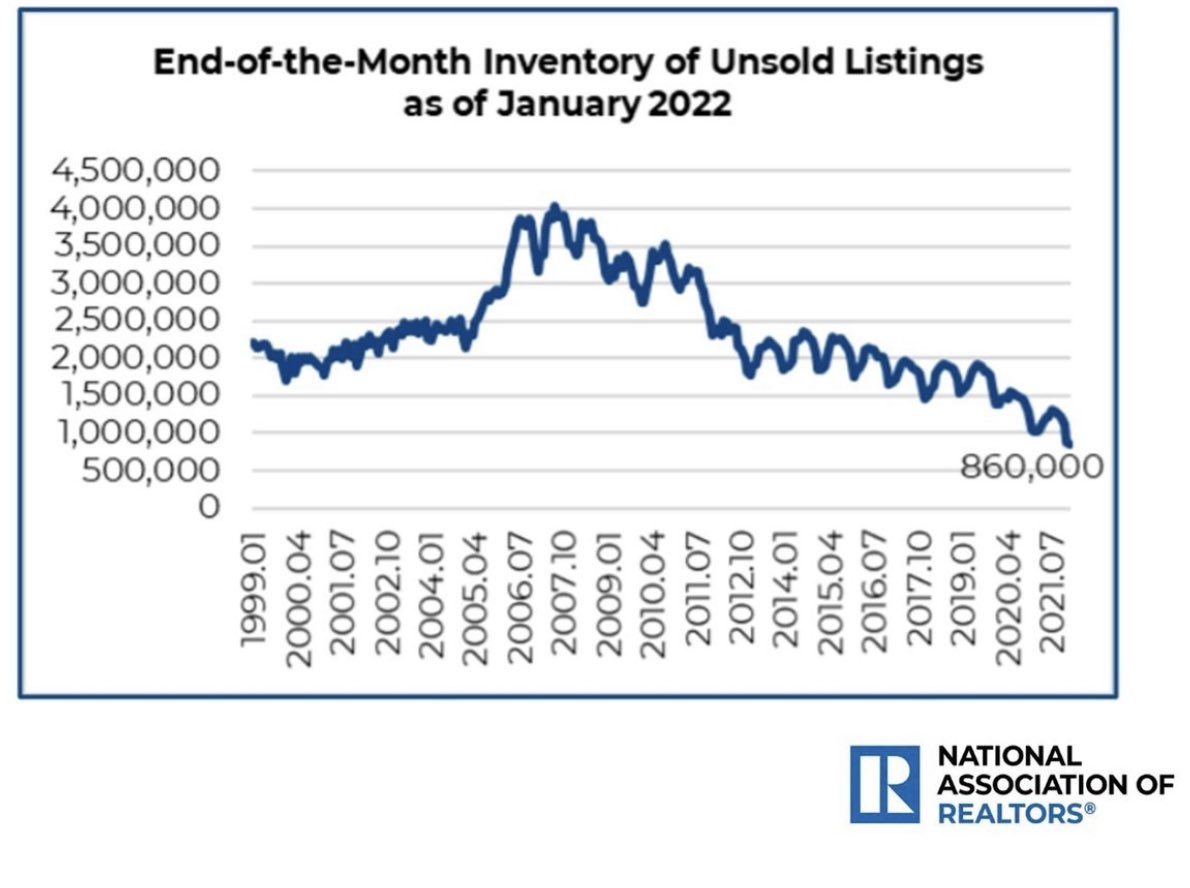

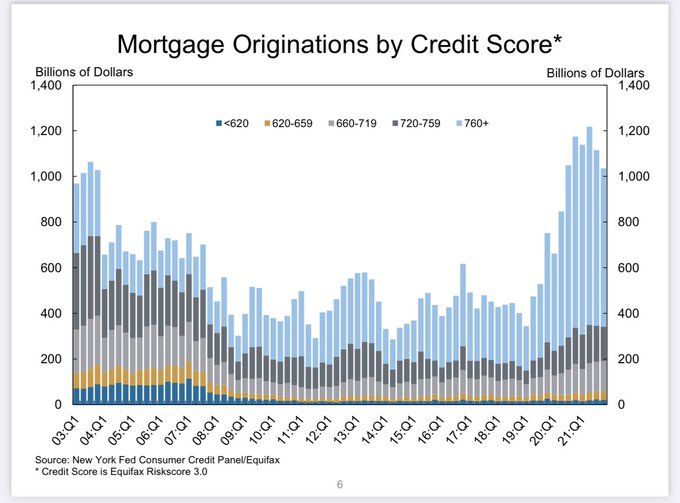

| Why owning a home is the best hedge against inflation Posted: 10 Mar 2022 11:34 AM PST  On Thursday, the Bureau of Labor Statistics reported the same trend that all Americans have seen lately: the inflation rate of growth is rampant and doesn't show any sign of easing up due to the Russian Invasion of Ukraine. The Consumer Price Index for all Urban Consumers “increased 0.8 percent in February on a seasonally adjusted basis after rising 0.6 percent in January…. Over the last 12 months, the all items index increased 7.9 percent before seasonal adjustment.” During the COVID-19 recovery phase, I predicted that job openings would break over 10 million. This week, we just broke to an all-time high in job openings with near 11.3 million. What does that mean? Wage growth is going to kick up! Early in 2021, I told the Washington Post that rental inflation was about to take off and will take the consumer price index up faster and last longer. For me, it's always about demographics equal demand. Wages are rising, which means rent is about to get higher. Shelter inflation, the most significant component of CPI, is making its big push as people need to live somewhere and that shelter cost is a priority over most things. Rent inflation on a year-over-year basis has been extreme in certain cities, averaging over double digits. Now we can see that being a renter has been problematic because rent inflation is taking off, gas prices are taking off, and even though wages are up, the monthly items consumers spend money on have gone up in the most prominent fashion in recent history. In some cases, seeing this type of rental inflation can motivate consumers to buy a home because renting a home isn't as cheap as an option anymore. However, if you're a young renter and looking to buy a house a few years away, this makes savings for a downpayment much more of a problem. On top of all that, since inventory is at all-time lows, it's been harder and harder for first-time homebuyers to win some bids because they don't have more money to bring into the bidding process. As always, the marginal homebuyer gets hit with higher rates and higher home prices. Now, single household renters are paying more for their shelter, making the home-buying process more challenging financially. What can Americans do to hedge themselves against this? In reality, being a homeowner over the past decade has set consumers up nicely during this burst of inflation! How is that? Housing is the cost of shelter to your capacity to own the debt; it's not an investment. This has been my line for a decade now. Shelter cost is the primary driver of why you might want to own a home. The benefit of being a homeowner is that with a 30-year fixed mortgage rate, that mortgage payment is fixed for the life of the loan. Yes, your property tax or insurance might go up, but the mortgage payment is generally fixed. What has happened over the years is that American homeowners have refinanced time and time again to where their shelter cost got lower and lower as their wages rose over time. We can see this in the data. It has never looked better in history with the recent refinance boom we saw during the COVID-19 recovery, since mortgage debt is the most significant consumer debt we have in America. This would imply that household debt payments are at deficient levels as well. Which they are, as we can see below. In the last 10 years, the big difference is that we made American Mortgage Debt Great Again by making it dull. While wages rise, long-term fixed debt cost stays the same. It doesn't get any better than that. So how does this make being a homeowner a hedge against inflation? As the cost of living rises, wage growth has to match it, especially in a very tight labor market. Companies can no longer afford not to increase wages to lure employees to work and retain workers. Wages are going up! What doesn’t go up? Your mortgage payment as a homeowner. So, you can benefit from increasing wages while the most considerable payment stays the same. Why do I keep stressing that the homeownership benefit is a fixed low debt cost versus rising wages? While renters feel stressed about rental inflation and higher gas prices, homeowners never need to worry about their sub-3% mortgage rate increasing versus the 7.9% inflation rate of growth. Some people who are surprised by all this inflation we have had over the last year are now asking how the U.S. economy can keep pushing along. Not every household is the same. If you're a renter, your rents have gone up and that takes away from your disposable income and makes it harder to save for a downpayment as well. If you're a homeowner, the inflation cost isn't as bad, since you are benefiting from rising wages. That offsets the cost of living and you're safe in your home with that fixed product. This is great for a homeowner, but it contributes to a larger problem: The homeowner is doing a little too well and might have no motivation to move. Why would anyone want to give up a sub-3% mortgage rate and such a solid positive cash flow unless they’re buying something that will make their cost much cheaper? People move all the time for many different reasons. However, let’s be realistic here: housing inventory has been falling since 2014 and 2022 isn't looking any better.

We haven't had to deal with high inflation levels for many decades, and back in the late 1970s, mortgage rates were a lot higher, so it's not an apples-to-apples comparison anymore. This is a brand new ball game with how beneficial it has been to be a homeowner in America. It's not great news if you're worried about inventory getting low, as I am. I often make fun of my housing crash addict friends who have been wrong for a decade. However, now I tell them: you're implying educated homeowners who have excellent cash flow will, for some reason, sell their homes at a 40%, 50% or 60% discount just to rent a home at a higher cost than what would have been the case for many years. Human beings don't operate that way. However, there is a downside to homeowners having such good financials: they don't have a reason to give up a good thing. This is just another reason I keep saying this is the unhealthiest housing market post-2010. As you can see above with the FICO scores of homeowners, their cash flow looks great and against this burst of inflation, owning a home is a nice hedge. My concern has always been with inventory going lower and lower in the years 2020-2024. Currently, with homeowners looking so good on paper, we have entered uncharted territory where mortgage rates for current owners are at the lowest levels ever recorded in history, inventory levels are at the lowest levels ever and now the cost of living from a rise in inflation has taken off in an extreme way. The biggest problem I see here is that this can make the housing inventory situation much worse as homeowners now have even more incentive to never leave their homes. The post Why owning a home is the best hedge against inflation appeared first on HousingWire. |

| LoanDepot restructuring creates new digital products/services unit Posted: 10 Mar 2022 09:08 AM PST Nonbank heavyweight loanDepot announced on Thursday an operational restructuring with the creation of a new business division called mello, under the leadership of the digital technology veteran Zeenat Sidi. The California-based lender plans to use mello to boost the development of innovative products and services in a market that has gotten ultra-competitive, with power buyers, real estate brokerage, mortgage lenders and fintechs all vying to create an end-to-end platform. Mello’s unit, which shares the name of the software platform loanDepot launched in 2017, will operate side-by-side with the company’s mortgage origination and servicing division. Both units will report directly to Anthony Hsieh, loanDepot’s chairman and CEO. “Accelerating the delivery of multiple new products and services – above and beyond mortgage products – through our mello operating unit will allow us to give consumers access to a complete suite of digital-first homeownership,” Hsieh said in a statement. The new operations unit will include the customer contact center, the mello DataMart, and the performance marketing engine. These units are responsible for distributing 10 million data-enriched leads annually and connecting more than a million customers daily, according to loanDepot. Three adjacent businesses – mellohome Real Estate Services, melloinsurance, and mello title and escrow services – will also be under Sidi. Last year, loanDepot’s origination volume topped $137 billion in 2021, an increase of 36% from the previous year, though gain-on-sale margins, profitability and the company stock price all fell. The company achieved 3.4% market share for the full year, up from 2.5% in 2020. A key strategic focus for loanDepot in the next few years is realizing business from its lead generation operations. In January, Hsieh said in a statement that the industry is a cyclical one, but loanDepot’s business was "purpose-built with period of pressure in mind," considering its proprietary tech stack, diverse mix of channels, and a marketing machine. "We control our lead flow, our customer contact strategy and the point of loan origination. This is a critical competitive advantage, enabling us to pivot and adjust our production as market trends demand," he said Sidi has the resume for a digital products and services job. She has held roles with Royal Bank of Canada, Capital One, and Sofi, which she joined in 2018 to build the home loans business but ended as the head of enterprise lending and investment for Galileo (a company SoFi acquired in 2020). Prior to joining loanDepot, she was at the fintech company Mission Lane. LoanDepot also recently hired George Brady, a longtime executive at Capital One, as chief digital officer. He’ll focus on refining and building out the lender’s technology stack. LoanDepot’s former chief information officer, Sudhir Nair, left in January. The reorganization comes about six months after loanDepot’s former head of operations, Tammy Richards, dropped a bombshell lawsuit that alleged that loanDepot, in a bid to drum up money during the refi boom and in preparation for its initial public offering, closed 8,000 loans without proper documentation at Hsieh’s behest. Richards claimed she was demoted for not complying with Hsieh’s alleged demands to close loans without credit reports. After a stint on medical leave, Richards, who once oversaw 4,000 employees, resigned in March 2021. LoanDepot disputed the claims made by Richards, who worked in senior roles at Wells Fargo, Bank of America, Caliber Home Loans and Countrywide Financial (one of the bad actors in the subprime loan crisis) before joining loanDepot. The post LoanDepot restructuring creates new digital products/services unit appeared first on HousingWire. |

| Lakeview readies rare securitization backed by nonperforming mortgages Posted: 10 Mar 2022 08:28 AM PST  Lakeview Loan Servicing, one of the nation's largest issuers of Ginnie Mae securities, is making a play in the private-label securities market by sponsoring an offering backed by a pool of 2,192 Federal Housing Administration-guaranteed mortgages valued at $423.6 million. The offering, via a conduit called Lakeview Trust 2022-EBO1, is a rare transaction involving mostly delinquent mortgages, according to Kroll Bond Rating Agency's (KBRA's) report on the offering, which is slated to close March 15. "The [current Lakeview] transaction is the fourth publicly rated non-agency securitization of its kind to be introduced to the market in over a decade," KBRA's report noted. Two similar past issuances, one in 2015 and another last year, also were sponsored by Lakeview, according to a US Bank trust investor report. A fourth such transaction, a $370.7 million offering of nonperforming Federal Housing Administration (FHA) loans, closed this past July and was sponsored by Waterfall Victoria Master Fund, with Carrington Mortgage Services acting as the loan servicer, according to a separate KBRA ratings report. The bulk of the mortgages (97%) in Lakeview's current private-label securities (PLS) offering involve FHA-insured mortgages 90 days or more past due that have been purchased out of Ginnie Mae (GNMA) loan pools via the agency's early buy-out, or EBO, program. "EBO strategies are expected to become more prevalent as a function of the size of the overall GNMA market," the KBRA report analyzing Lakeview's pending offering stated, "with GNMA outstanding MBS [mortgage-backed securities] at approximately $2.1 trillion in 2021 vs. approximately $400 billion in 2007." Ginnie Mae makes it possible for lenders to originate qualifying mortgages that they can then securitize through the government-sponsored agency. Ginnie, however, guarantees only the principal and interest payments to purchasers of its bonds, which are sold worldwide. The underlying loans carry guarantees, or a mortgage insurance certification, from the housing agencies approving the loans — which include single-family mortgages backed by the FHA, the Department of Veterans Affairs and the U.S. Department of Agriculture. Under Ginnie's EBO program, after the mortgages acquired by lenders become current for six consecutive months, often through modifications, they are eligible to be re-securitized as part of a new Ginnie Mae loan pool. "Once a loan goes 90 days delinquent, and the servicer has made two [required] principal and interest advances, Ginnie Mae allows the [servicer] to buy that loan out at par," said Tom Piercy, managing director of Incenter Mortgage Advisors. "The benefit of this a [the lender] immediately stops advancing the principal and interest each month. "If I [as the owner of the loan] can get the borrower to make six monthly payments in a row, then I can reissue that loan into a Ginnie Mae security. And what am I getting? A 103% to 105% [potential return], and I bought it out at par [100% of face value]." That reperforming path and subsequent Ginnie Mae re-pooling represents the highest income-generating potential for the EBO offering, given it provides six months of uninterrupted payments on the pooled mortgage and the option for a cash-out of the loan at the end of that period via the Ginnie Mae re-securitization. "KBRA generally views the reperforming path as the most beneficial to the transaction as it is generally the shortest resolution path," the bond-rating report stated. The downside risk is an ultimate loan default, kicking in the underlying loan insurance provided through FHA, which is part of the U.S. Department of Housing and Urban Development (HUD). Although principal recovery is guaranteed through FHA in the event of a default, there often is a bureaucratic time lag in obtaining interest due, KBRA noted. In addition, interest rate recoveries are at the HUD debenture rate, "which is typically substantially below the loan note rate," according to KBRA. "There is a time lag for obtaining such interest recoveries, creating associated negative carry," the KBRA report explained. "The portion of unreimbursed expenses for typical foreclosure expenses, including property preservation and attorney's fees, can differ depending on servicer competency." Lakeview's EBO private-label offering includes an interest-rate reserve account to cover potential bond-interest shortfalls. Lakeview is part of the Bayview Companies and a subsidiary of Bayview MSR Opportunity Master Fund LP. It also is an affiliate of Bayview Asset Management, a certified minority-owned and private equity firm with hedge fund holdings. As of March 6, Lakeview ranked as the third largest issuer of Ginnie Mae securities, controlling 10.5% of the agency's servicing book of business — with a $210.6 billion portfolio comprised of both new-issuance securitizations and net purchases, according to a recent report from mortgage-data analytics firm Recursion. Ahead of Lakeview at the No. 1 position is Freedom Mortgage, with a 12.9% market share, followed by Pennymac, 11.4%. For the month of February, however, Lakeview ranked as the second largest issuer of Ginnie Mae securities, with some 16,000 mortgages securitized with a total value of $3.8 billion, according to Recursion. Pennymac ranked first, with 24,000 loans securitized via Ginnie Mae valued at $6.76 billion. Rocket Mortgage was third, with 15,000 loans valued at $3.5 billion — followed by UWM, 8,000 mortgages valued at $2.97 billion; and Freedom Mortgage, 12,000 loans valued at $2.94 billion. In total for the month, mortgage lenders delivered to Ginnie Mae pools some 476,000 loans for a combined value of $138 billion. Issuance volume, however, was down by $41 billion from January 2022, Recursion reported. The post Lakeview readies rare securitization backed by nonperforming mortgages appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment