Mortgage – HousingWire |

| UWM sues broker shop for sending loans to Rocket, Fairway Posted: 04 Feb 2022 12:14 PM PST United Wholesale Mortgage (UWM) is making good on its threat to take legal action against partnering broker shops that also send business to Rocket Mortgage and Fairway Independent Mortgage, a violation of the wholesaler’s controversial broker agreement. UWM filed a lawsuit in Michigan federal court late Thursday that claims America’s MoneyLine, a high-volume mortgage brokerage based in Southern California, owes it $2.8 million for repeatedly violating the terms of the agreement. The broker agreement was modified just under a year ago to prevent broker shops from doing business with Rocket and Fairway, an initiative UWM dubbed “All-In.” In March 2021, UWM CEO Mat Ishbia announced on Facebook Live that mortgage brokers who did business with Rocket Mortgage or Fairway Independent Mortgage could not also send loans to UWM as of March 15. Any broker who did so would face fines upwards of $5,000 per loan or $50,000, whichever violation sum was greater. Ishbia told HousingWire at the time that Rocket and Fairway were “undermining” the wholesale channel, and the wholesale lender's decision was based on a need to protect mortgage brokers from bad actors. Critics, meanwhile, argued it wasn’t high-minded in the least. It was no more than a brazen attempt to kneecap competitors, they said. (Rocket and Fairway, however, both said UWM’s strategy ended up generating an uptick in wholesale business for them.) The lawsuit claims that since signing the “All-In” addendum, America’s MoneyLine has submitted at least 560 mortgage loans to Rocket and Fairway. It goes on to say that if America’s MoneyLine — which is licensed in 20 states and originated $1 billion over the last two years — wanted to do business with the two lenders, they could have done so, but only after terminating the agreement with UWM. Ishbia said UWM had a conversation with America’s MoneyLine about violating the agreement before the lawsuit was filed. Shawn John Nevin, the CEO of Orange County-based AML, declined to comment. However, in a statement he provided HousingWire Friday afternoon, he described UWM’s move as “anticompetitive, anti-American” and said it won’t survive judicial scrutiny. “We will outline and prove in court how we were misled by ongoing assurances of nonenforcement of this non-American antitrust provision,” he wrote. “We have lost and will continue to lose millions of dollars because of these unfounded tactics, of which we will pursue. Moreover, the broker community will get a glimpse into UWM's true goal of seeking to control independent brokers to such an extent that they ultimately become effective arms of UWM; something we simply cannot and will not agree to do. This is why we are brokers — to have the right of choice. As independent brokers we need to be able to shop for the best terms and best programs for our clients, the American people.” Nevin also said that “many brokers” are using both Rocket and UWM “without incident” but his firm is being made an example of. In an interview with HousingWire, Ishbia, whose firm controls about one-third of the wholesale market, said that they discovered that a “handful” of brokers who signed the addendum were also sending loans to Rocket and/or Fairway. “What we found was a couple had like two loans or four loans,” he said. “This company had hundreds of loans. And so this was the only one that was substantial enough…it was a large company that signed a contract, agreed to the terms of a contract and disregarded it.” Ishbia added that any broker firm found to be violating the amended broker agreement could face legal consequences. Nearly a year after the ultimatum was issued, Ishbia calls it an unqualified success. More than 11,500 brokers signed the agreement, and some top brokers who initially didn’t sign have since done so, he said. UWM’s origination volumes have steadily risen while many competitors are slowing down, he said, yet more proof that it’s been effective. Still, many brokers have chafed at the ultimatum. Even some who signed the addendum complained that the ultimatum cut at the identity of a mortgage broker – being able to offer consumers the greatest range of mortgage options was central to their mission, they said. In August, a Florida mortgage broker named Dan O’Kavage filed a class-action-seeking lawsuit that targets the ultimatum. The lawsuit argues that the “All-In” initiative undermined brokers' ability to choose the best programs for their clients, creating harm and potentially higher costs to borrowers. It claimed that UWM "willfully violated numerous federal and Florida laws and regulations," including the Sherman Antitrust Act, the Florida Antitrust Act, the Tortious Interference with Business Relationships and Florida's Deceptive and Unfair Trade Practices Act. O'Kavage's suit also alleges that brokers were forced into an unenforceable contract. In his statement, Nevin said America’s MoneyLine won’t be taking on the biggest player in the channel alone. “We have spoken to other customers and brokers throughout the country who intend to stand up with us and fight this tyranny together,” he said. Correction: An earlier edition of this story incorrectly stated that any broker who violated the addendum could face fines upwards of $5,000 per loan or $50,000 per month, whichever violation sum was greater. There is no time stipulation. For detailed, exclusive reporting and analysis on this subject and more, sign up for HousingWire's LO-focused LendingLife newsletter. The post UWM sues broker shop for sending loans to Rocket, Fairway appeared first on HousingWire. |

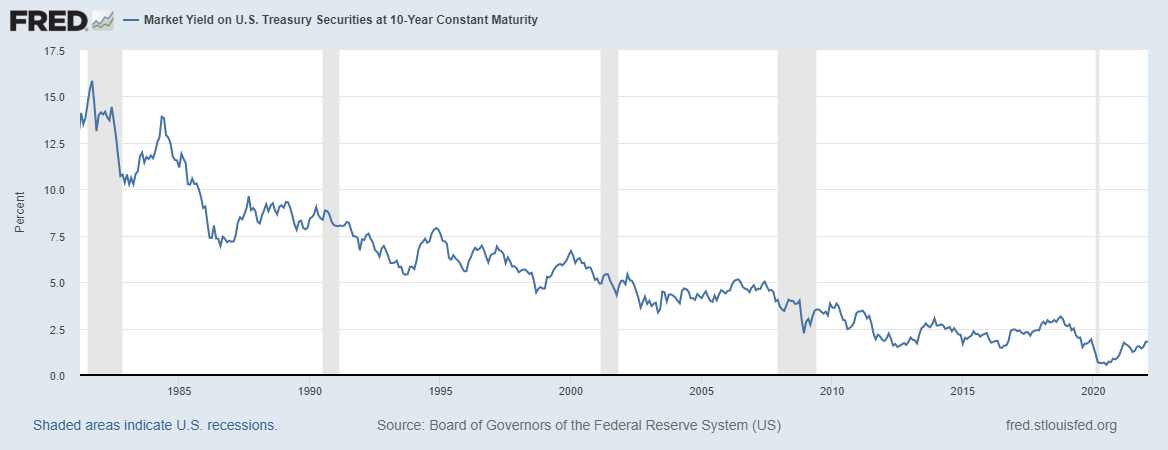

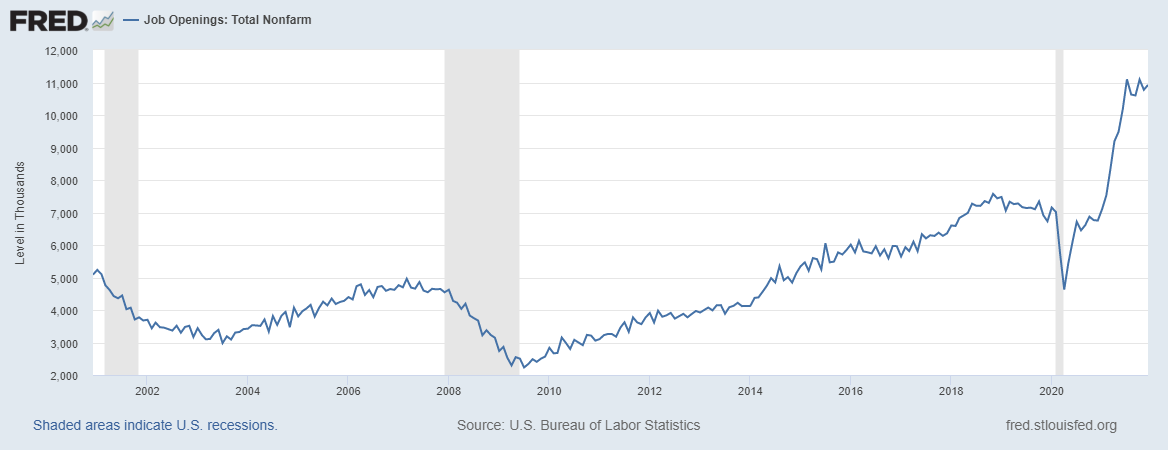

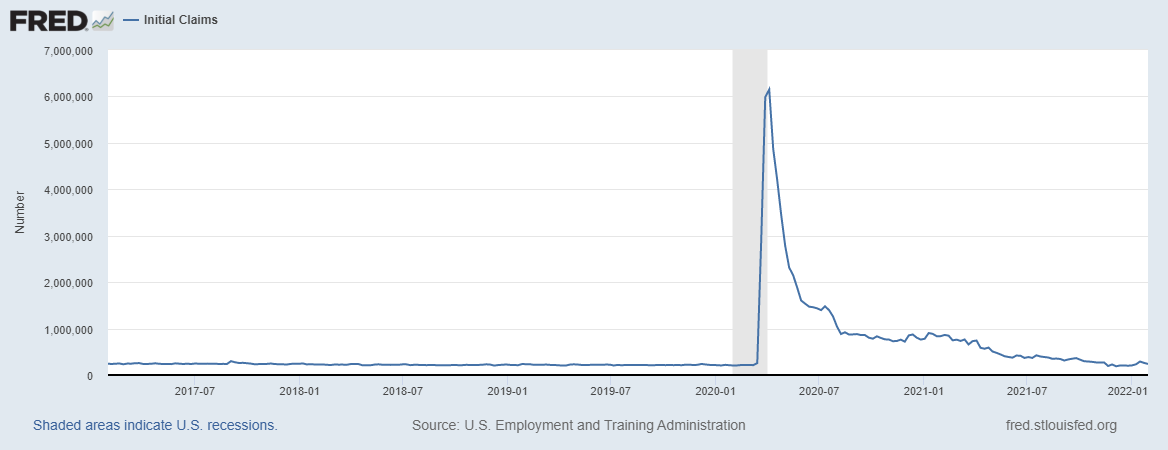

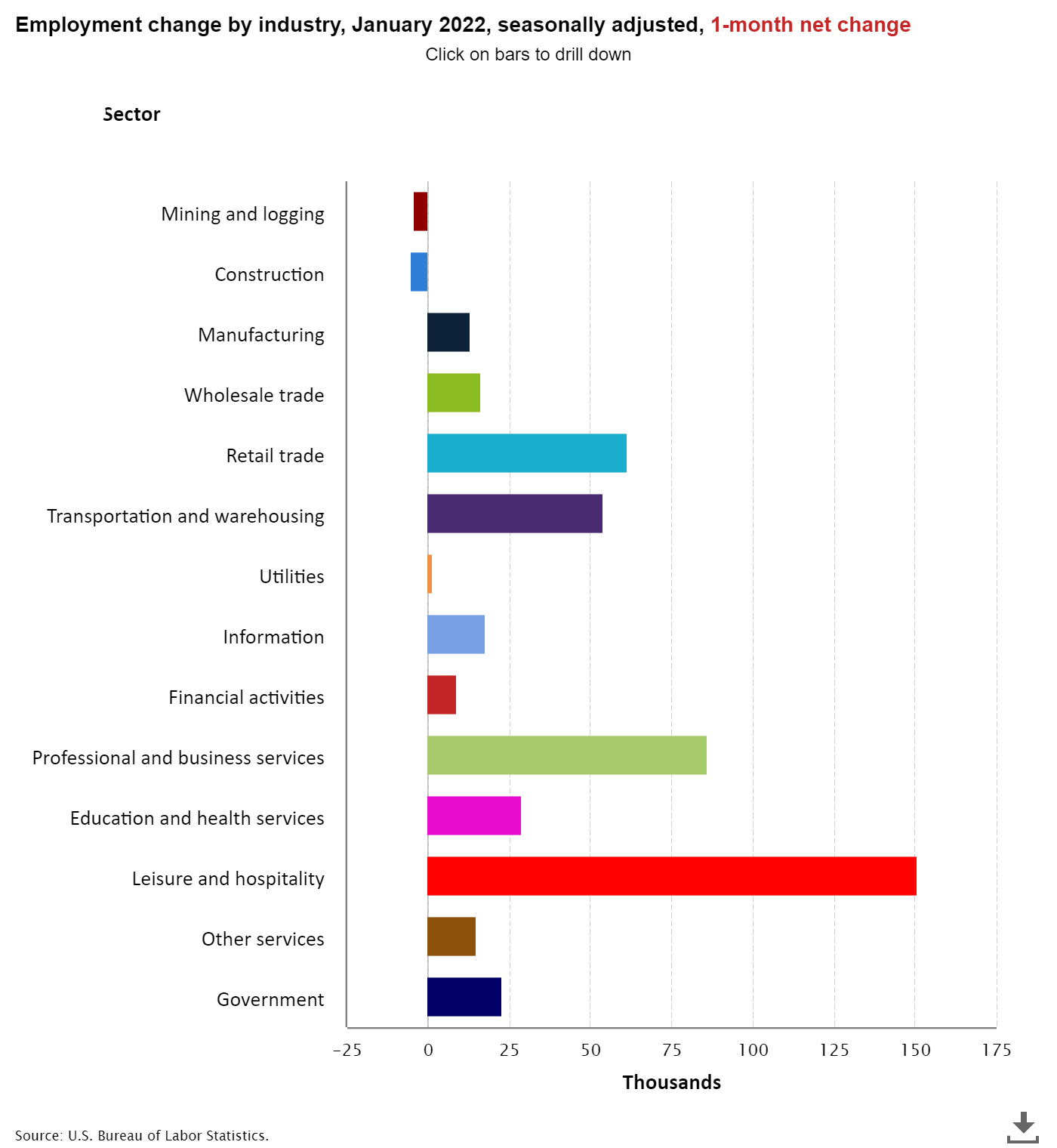

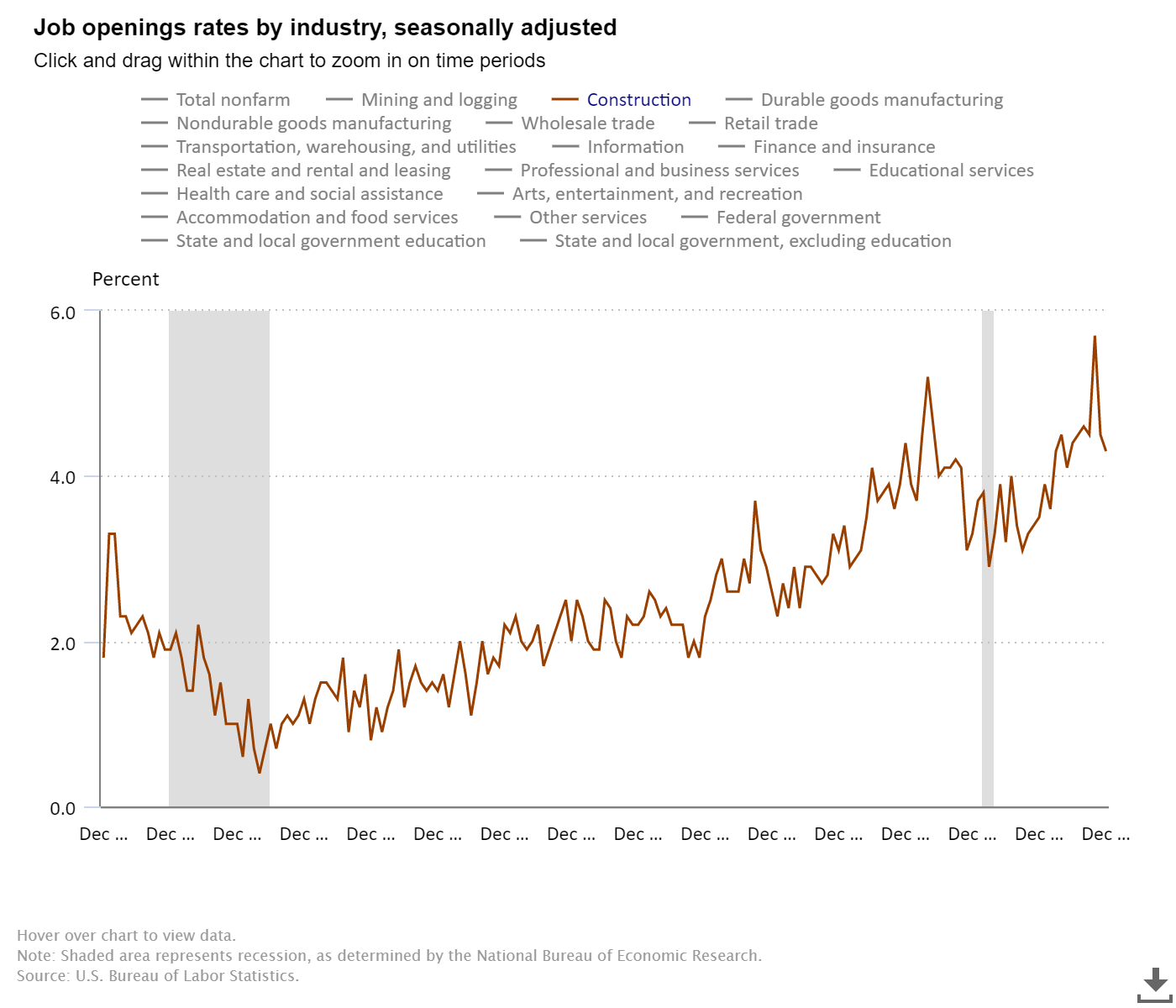

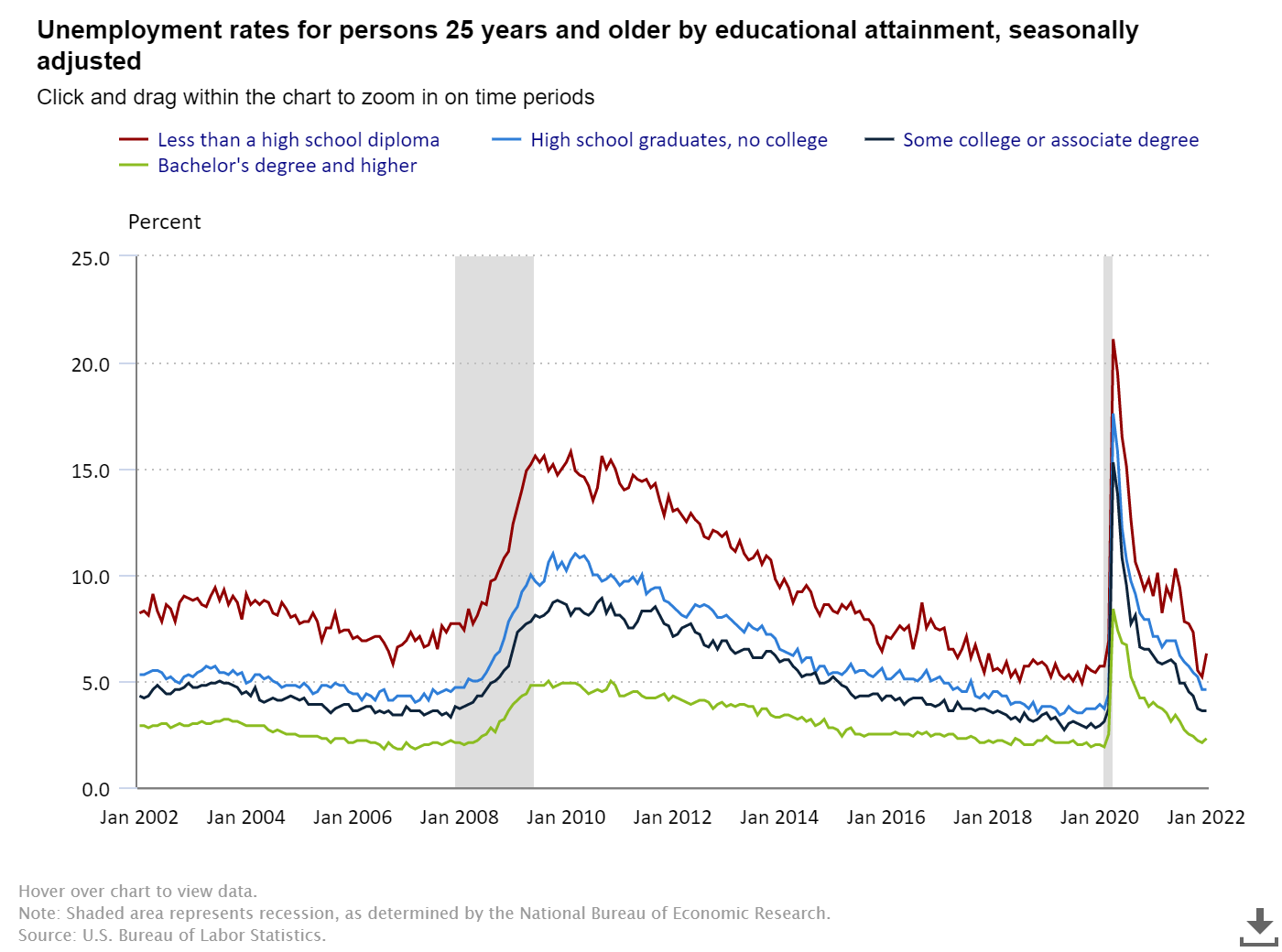

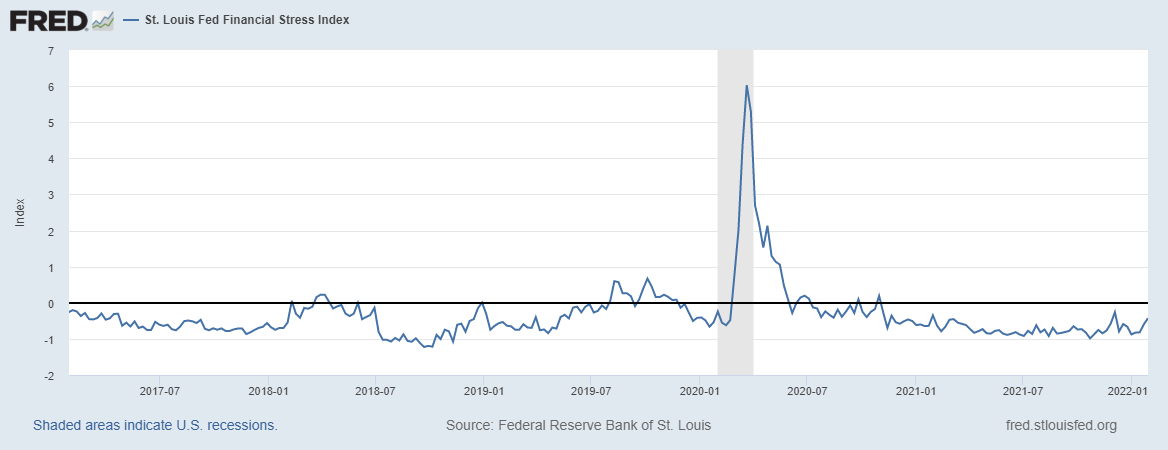

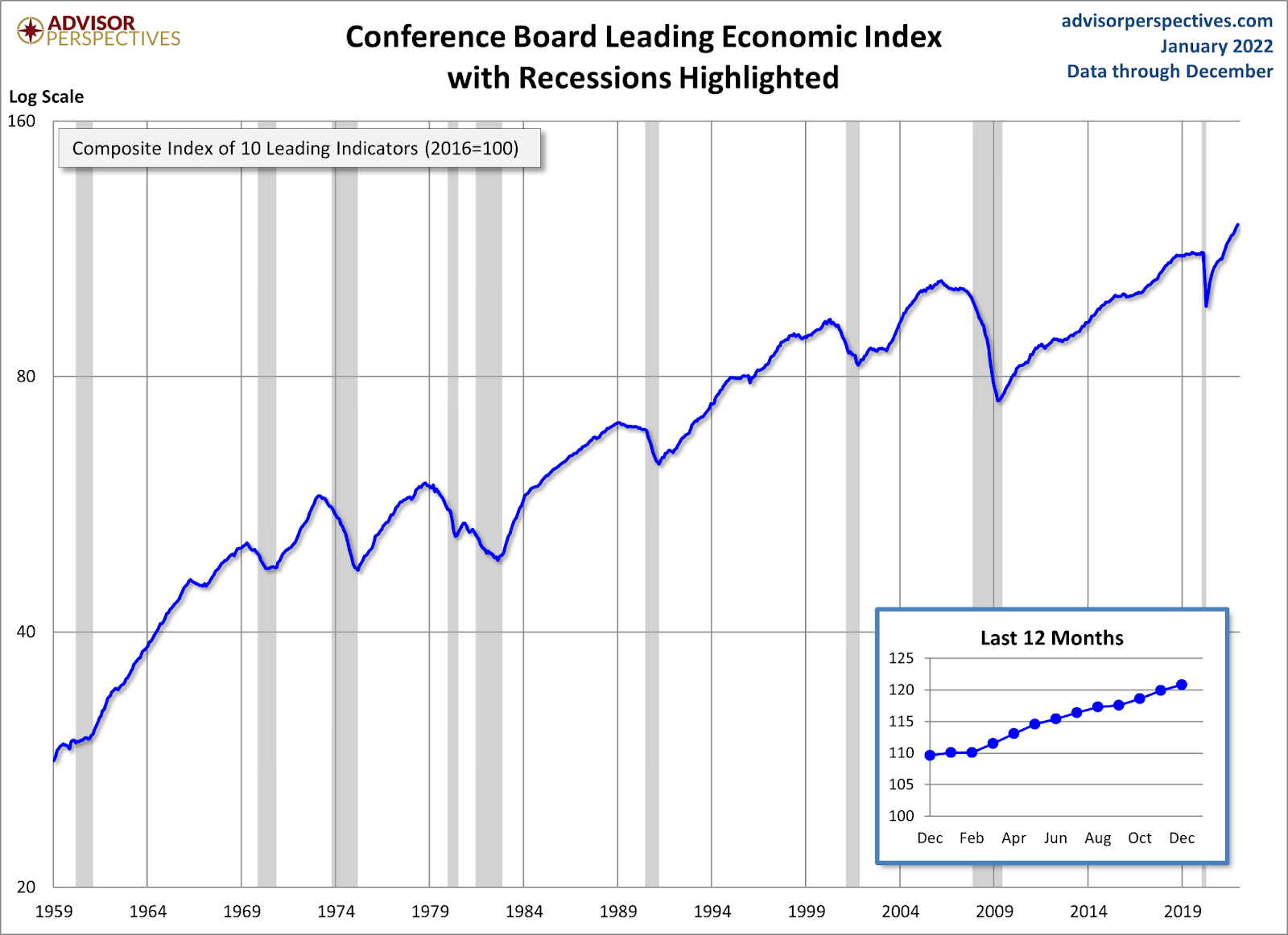

| Positive jobs report sends bond yields higher Posted: 04 Feb 2022 11:23 AM PST  Today, the Bureau of Labor Statistics reported that 467,000 jobs were created in January. This was a big surprise as some people, including me, thought the rise in the number of sick days being reported could impact this month's job report. One of the factors I’ve cited over the last few months is that we should see more positive revisions occur in the future. The total positive revisions in this report are 709,000. To say that I was excited to see this report is an understatement. Since the economic lows in April of 2020, it has been a joy to see my country make the most significant economic comeback ever. What I wrote on April 7, 2020, I truly believe on the economic front: “My faith in America winning has never let me down because I always believe in my people and country. I can tell you now, this virus isn't changing my view on that." One of the most significant differences between the recovery from the great financial crisis compared to the COVID-19 recovery is that the labor dynamics have been much different this time around. The truth was that we were never going to go into a job-loss recession in 2020 without COIVD-19 and job openings were near 7 million before COVID-19 hit us. Before the job openings data took off, I was very adamant on Twitter that JOLTS would hit 10 million soon. Job openings are now near 11 million, as the U.S., just like many other countries, has an aging workforce that is difficult to replace. As you see from the chart below, the labor market dynamics from the end of the great financial crisis, where job openings were just a tad over 2 million, weren’t as positive as those we had right before the COVID recession. Jobless claims data looks very solid. Even with all the Americans reporting sick due to Omicron, the need for labor in America is massive. So, let’s take a look at the numbers today with eight months left until the September report. That leaves us with 2,924,000 jobs left to make up with eight months to go, which means we need to average adding 365,500 jobs per month. The unemployment rate currently stands at 4.0% Now this jobs report was such a shocker to the upside that it does have some risk of negative revisions, but still, the trend is your friend and we are still working to get all the jobs back lost to COVID-19. Here is a breakdown of today's job data. Even though total construction jobs fell, residential construction jobs had another positive month. One giant fact that people tend to forget always is that a majority of Americans who want to work have always been working. The part of the labor force with the least educational attainment tends to have a higher unemployment rate. On Twitter, I started the hashtag A Tighter Labor Market Is A Good Thing to remind everyone that the economy runs hot when we have a tighter labor market. We want to see the kind of unemployment rates that college-educated people have spread to everyone because we have tons of jobs that don't need a college education. Here is a breakdown of the unemployment rate and educational attainment for those 25 years and older: —Less than a high school diploma: 6.3%. My 2022 forecast said: For 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper end range in mortgage rates is 3.375%-3.625% and the lower end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981. We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don't support this. The bond market shot up higher as soon as the jobs report came in and currently, at this very second, the 10-year yield is at 1.93%. I totally understand why people are confused why bond yields are still below 2% with the economy running so hot and inflation data being as high as it is. However, as always, I have tried to stress, the trend is your friend. Bond yields and the 10-year yield are just following that long-term trend lower.  With that said, what I want to see is the same thing I stressed in 2019. We need to see the 10 year yield close above 1.94% and follow-through bond yield selling to have conviction that bond yields can go higher. This jobs report was a very big positive for the Untied States of America and global yields, especially in Japan and Germany, are rising. This is the right backdrop for mortgage rates to rise and hopefully create some balance in the housing market because if this doesn't do it, I see nothing else that can create more days on the market as we are starting spring 2022 with fresh new all-time lows in inventory. Economic cycle updateNow for an economic update. Some of the economic data has been cooling off as expected. The surge in Omicron cases, while not being able to create the same fear and panic as we had in March and April of 2020, did impact some of the economic data. In general, the rate of growth in some economic data can't be replicated in 2021, such as GDP and the rate of growth of retail sales. However, the U.S. economy is still in expansion mode with only one of my recession red flags raised. The St. Louis Financial Stress Index, a crucial variable in the AB recovery model, is showing a bit of life lately at -0.4227%. The stock market has been more volatile lately and talks about how many rate hikes are coming in 2022 has perked up the financial markets from their bored state in 2021. The leading economic index has been very solid lately. When this data line falls for four to six months straight, then the topic becomes different. However, this hasn't been the case, it bottomed in April of 2020 and has had a sharp rebound. Once the Fed raises rates, the second recession red flag will be raised. My job is to show you the progress of the economic expansion, into the next recession, and out — over and over again. My models don't sleep! Once more red flags are raised, I will go over each and every single one. At some point in the future, I will be on recession watch, when enough red flags are up. However, we are not at that time yet. Even though I no longer say we are early in the economic expansion, we are still on solid footing. However, the more exciting thing for me is to see whether we can finally crack over 1.94% on the 10-year yield and try to bring balance to an extremely unhealthy housing market. The post Positive jobs report sends bond yields higher appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment