Mortgage – HousingWire |

- Logan Mohtashami: The 2022 housing forecast

- Rocket acquires Truebill app for $1.275B in cash

- Help for troubled borrowers is on the way. But will it come soon enough?

- Conforming loan limits draw scrutiny

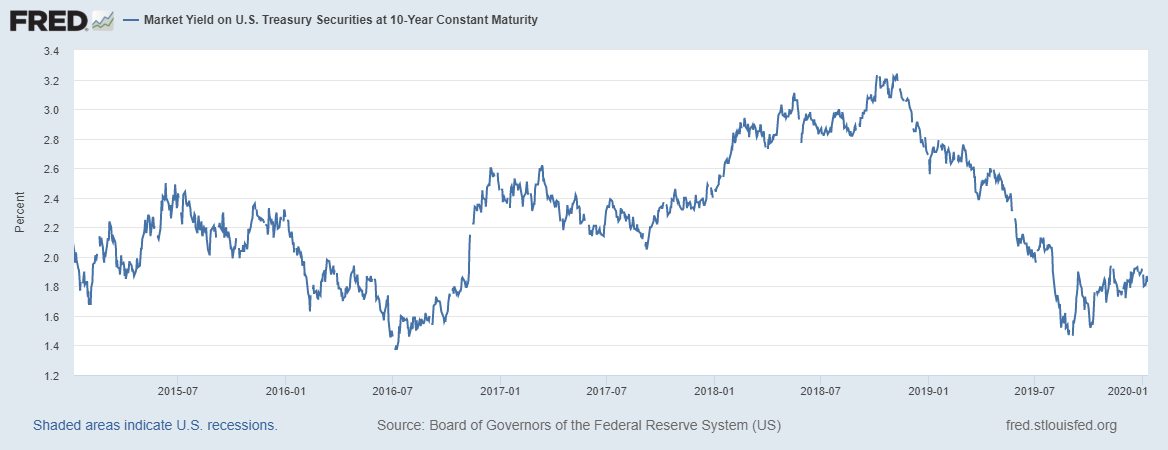

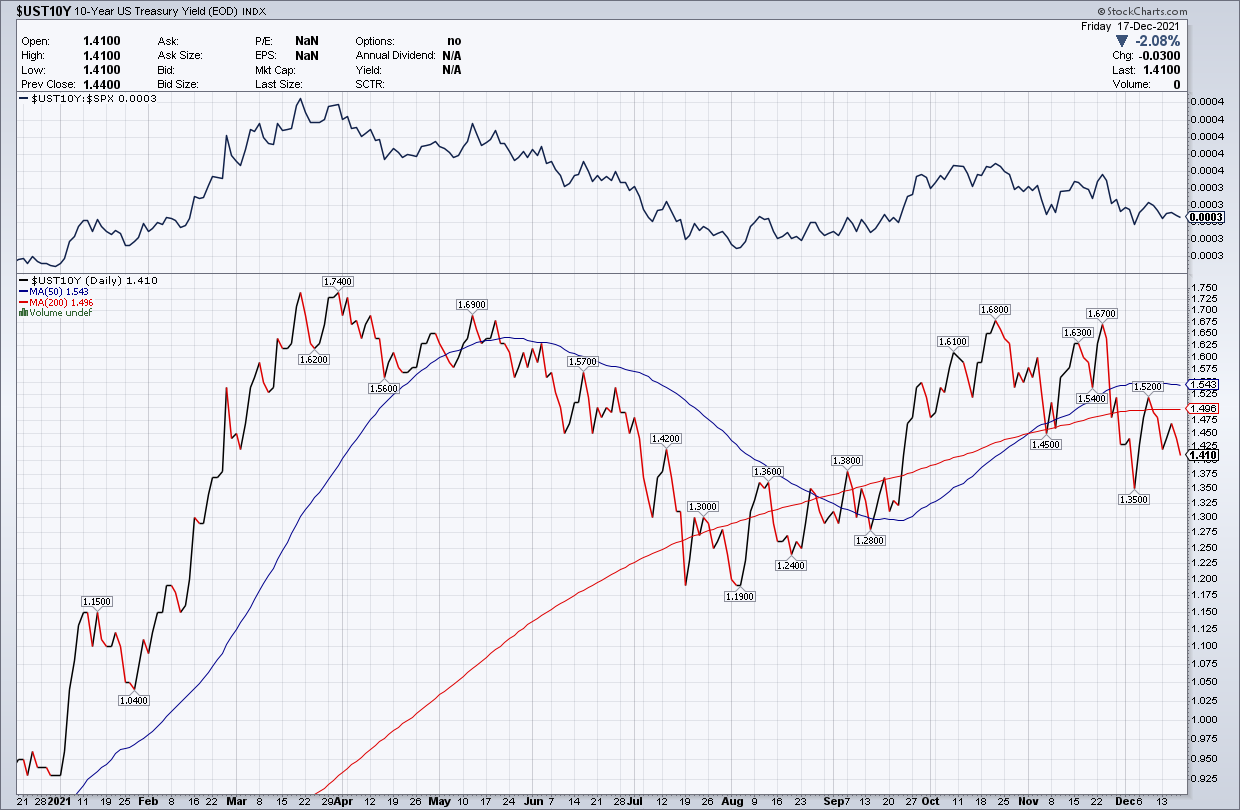

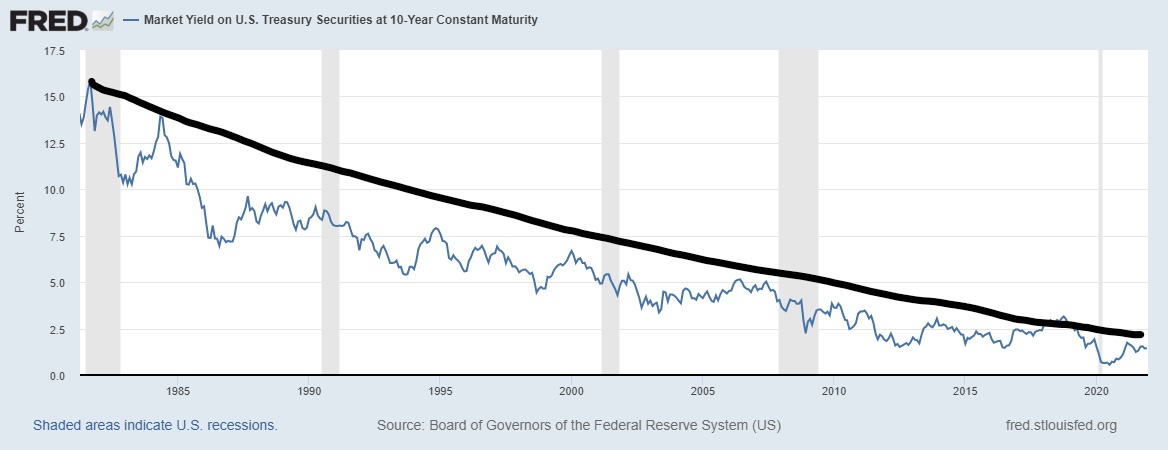

| Logan Mohtashami: The 2022 housing forecast Posted: 20 Dec 2021 10:51 AM PST  Most of the time, the economy is like a slow-moving ocean liner that changes direction gradually and without much effort. But when a new, powerful variable presents itself, like the worldwide COVID-19 pandemic, the economy can change on a dime. COVID was a veritable iceberg for our ocean liner economy, but the ship did not go down! Even in the extreme conditions of COVID-19, my general premise on housing economics predicted that the two variables with the most influence — demographics and mortgage rates — would hold up the housing market. With those two factors still very much in play, here is my 2022 forecast. The 10-year yield and mortgage ratesThe forecastFor 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper end range in mortgage rates is 3.375%-3.625% and the lower end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981. We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don't support this. The backstoryThe lifeblood of my economic work depends greatly on the ebbs and flows of the 10-year yield, even more than mortgage rate targeting, which is unusual for a housing analyst. When I first dipped into 10-year yield and mortgage rate forecasting in 2015, during the previous expansion, I said the 10-year yield will remain in a channel between 1.60%-3%. I've stuck to that channel forecast every year since — and for the most part that 10-year yield channel stuck. That range dictated that mortgage rates would roughly stay between 3.5%-4.75%.

My forecast for the 10-year yield range in 2021 was 0.62%-1.94% which translates to a bottom-end range in mortgage rates of 2.375%-2.5%, and an upper-end of 3.375%-3.625%. Single mortgage rate target forecasts have not fared well over the decades because these forecasters did not respect the downtrend in bond yields since 1981. The X factorCan there be a bond market sell out short term, sending yields above 1.94%, like what we saw early in the COVID-19 crisis? Yes, but if the markets do overreact for any reason, typically bond yields would fall back. Why do I not believe bond yields will push higher aggressively? The economic rate of growth peaked in 2021. The economy was on fire this year, and inflation data was super-hot. Even so, the highest the 10-year yield got was 1.75%. The economic disaster relief that boosted the recovery in 2020 and 2021 has been drawn down.

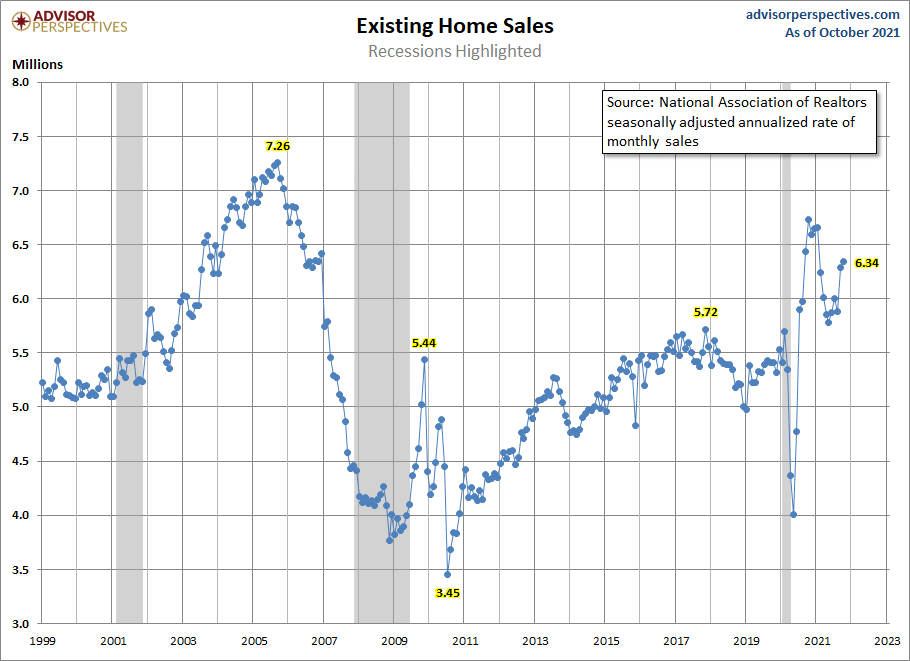

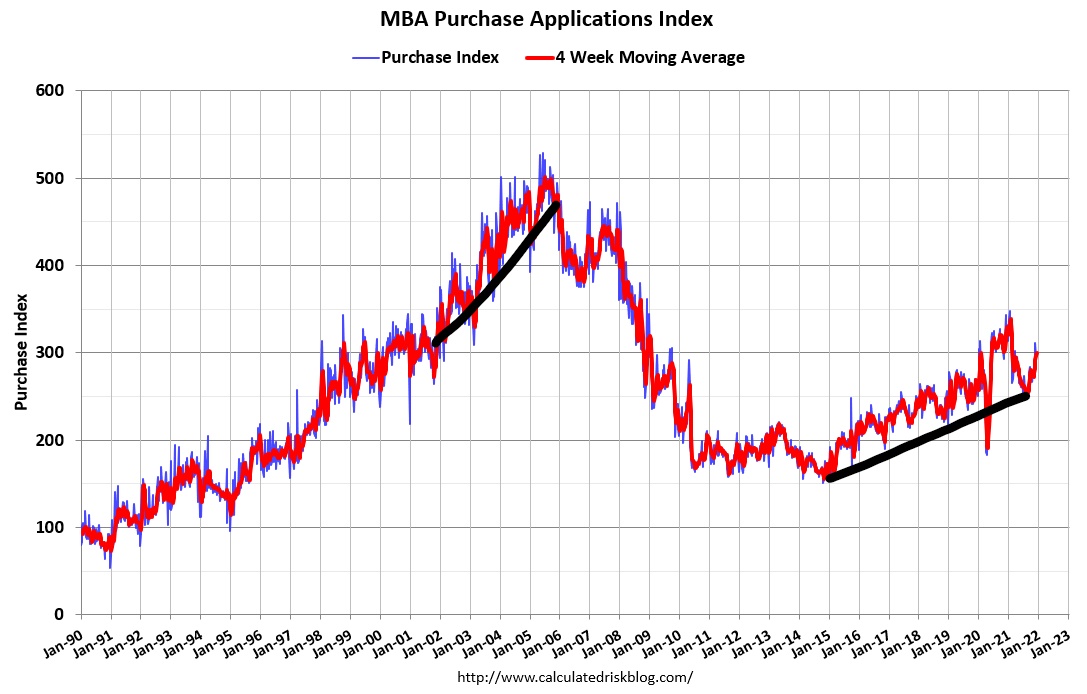

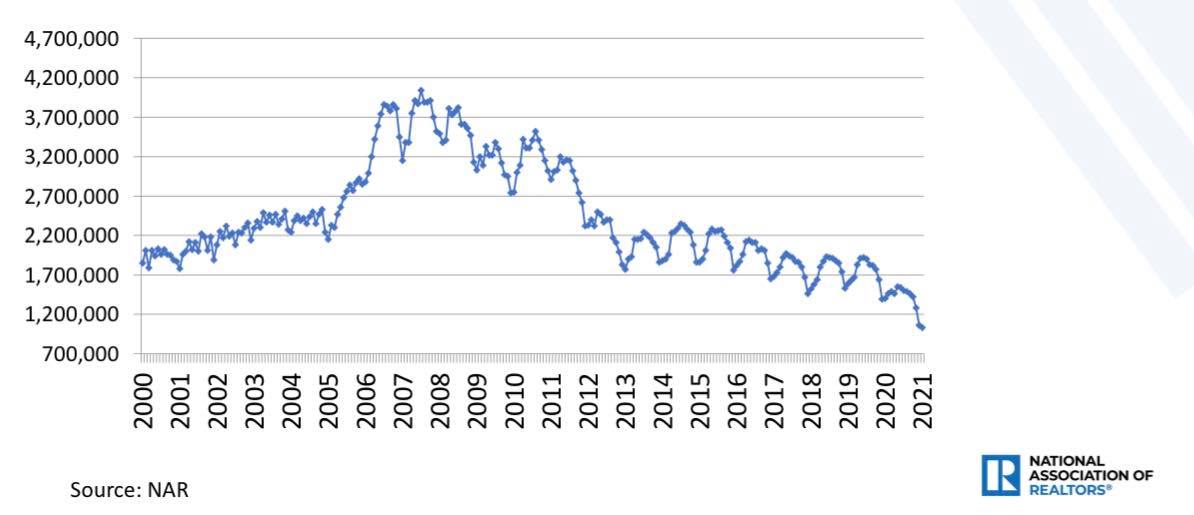

Existing-home salesThe forecastFor 2022, I am forecasting the same sales trend range as 2021 of about 5.74 million to 6.16 million. If monthly sales prints are above 6.16 million for existing homes, then I would consider the market more robust than expected. If sales trend toward 5.3 million then we will be back to 2019 levels. This would still be healthy sales considering the post-1996 trend, but it will mean housing demand has gotten softer. This has happened before when higher rates have impacted demand. This is why since the summer of 2020 I have written about how if the 10-year yield can get above 1.94%, then things should cool down. However, as you can see it's been hard to bond yields over that level and thus mortgage rates above 3.75%. The backstoryIf the last two reports of the year on existing home sales are above 6.2 million, I will admit that sales have slightly outperformed what I predicted for 2021. Early in 2021, I wrote that home sales would moderate after the peaks caused by the COVID-19 shutdown make-up demand and that readers should not overreact to this slowing. I wrote that sales would range between 5.84 million and 6.2 million, and that we could anticipate a few prints under 5.84 million — but sales would consistently be above the closing level of 2020 of 5.64 million. We got one print below 5.84 million and a few recent prints over 6.2 million, with two more reports. Mortgage demand was solid all year long and has picked up in the last 15 weeks. One of my longer-term forecasts in the previous expansion was that the MBA Index would not reach 300 until 2020-2024. We got there in the early part of 2020, then the Index got hit by the COVID-19 delays in home buying to only have a V-shaped recovery that led to the make-up demand surge, moderation down and back to 300. As you can see, it's been like Mr. Toad's wild ride here. We will still have some COVID-19 year-over-year comps to deal with up until mid February and then we can get back to normal. However, one thing is for sure: demand has been solid and stable in 2020 and 2021. Also, the market we have today doesn't look like the credit boom we saw from 2002-2005.

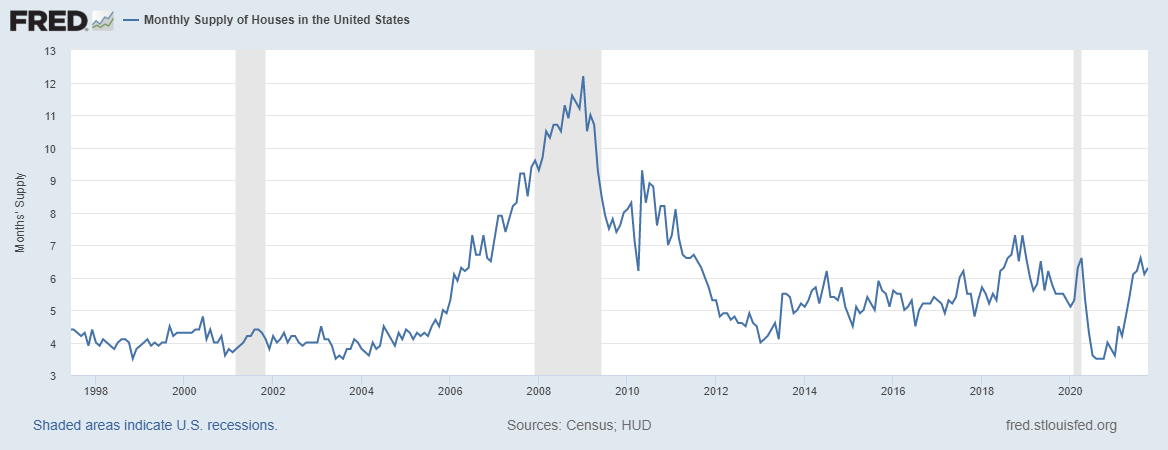

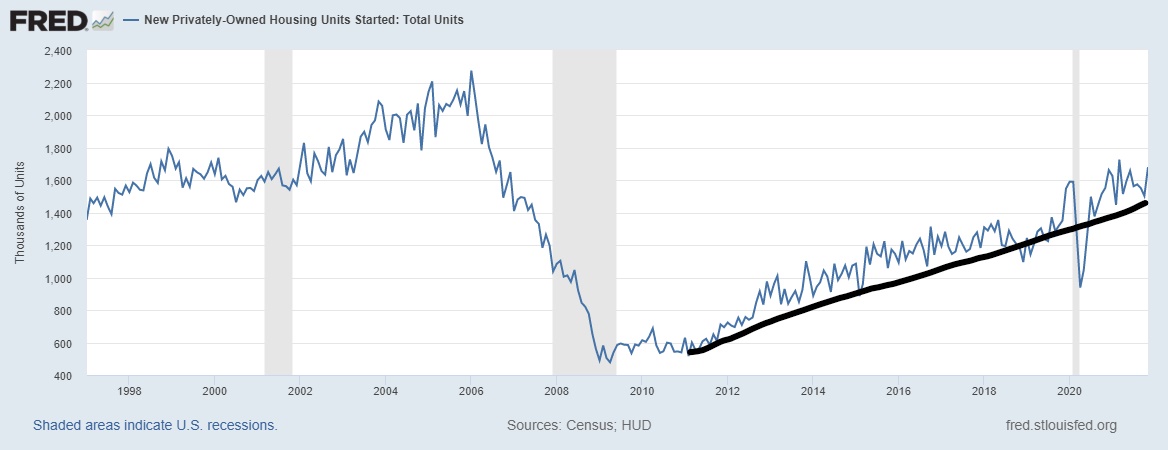

New home sales and housing startsThe forecastMy long-term call from the previous expansion has been that we won't start a year at 1.5 million total housing starts until the years 2020-2024 and we have finally gotten here much like the 300 level in the MBA index. My rule of thumb has always been to follow the monthly supply data for new homes, and as long as monthly supply is below 6.5 months on a three-month average, they will build. The backstoryHousing starts, permits and builders confidence are ending the year on a good note. Even though new home sales aren’t booming this year, it's good enough to keep the builders building more homes even with all the drama of labor shortages, material cost and delays in finishing homes. As you can see below, the uptrend has been intact even with the slowdown in 2018 and the brief pause from COVID-19.

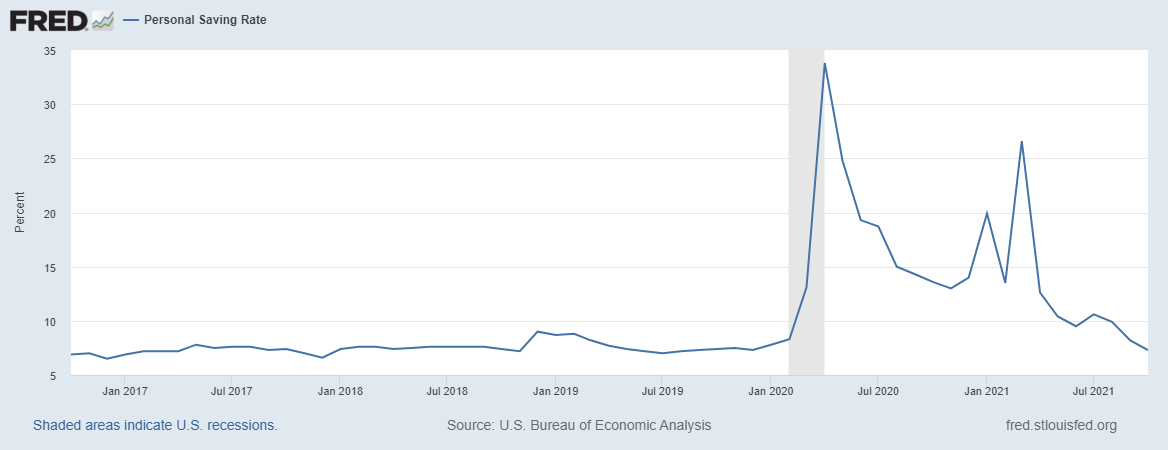

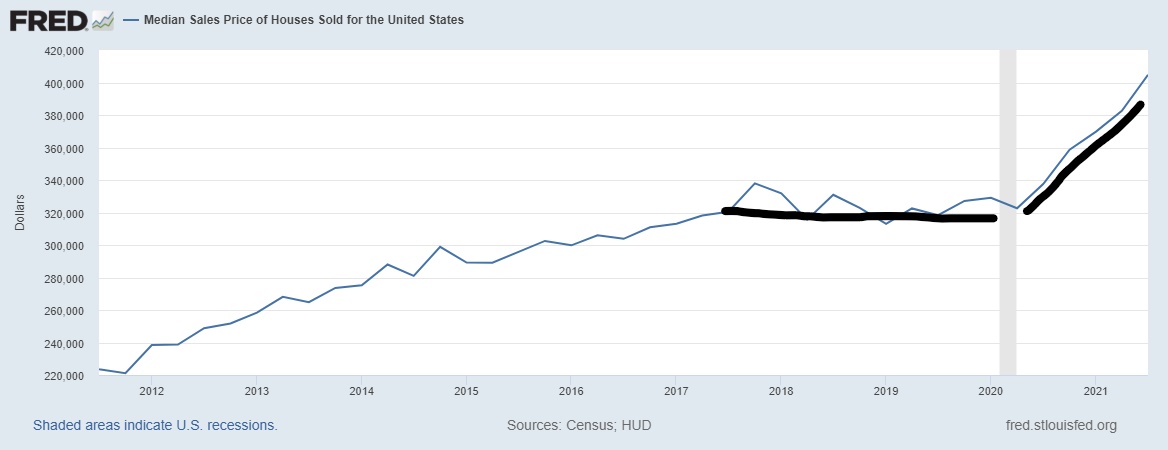

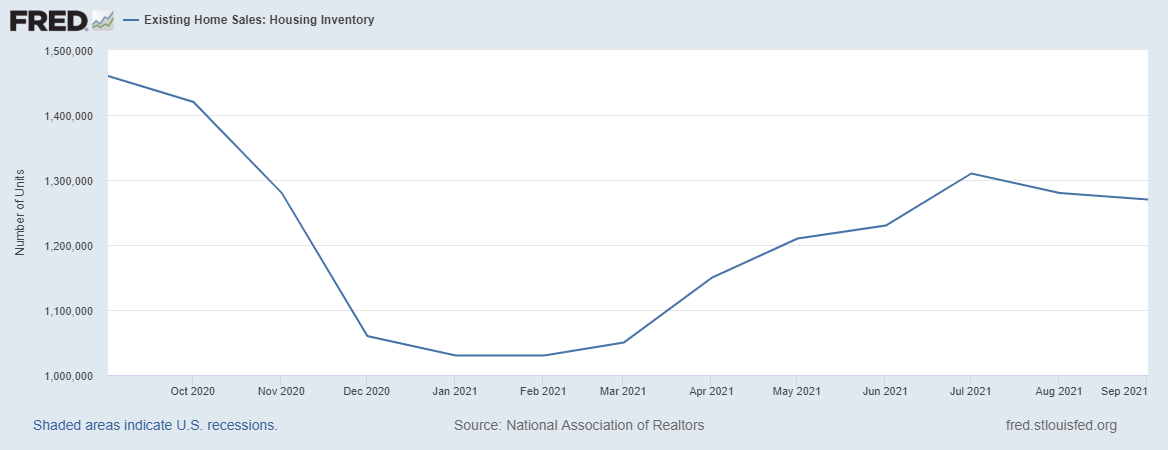

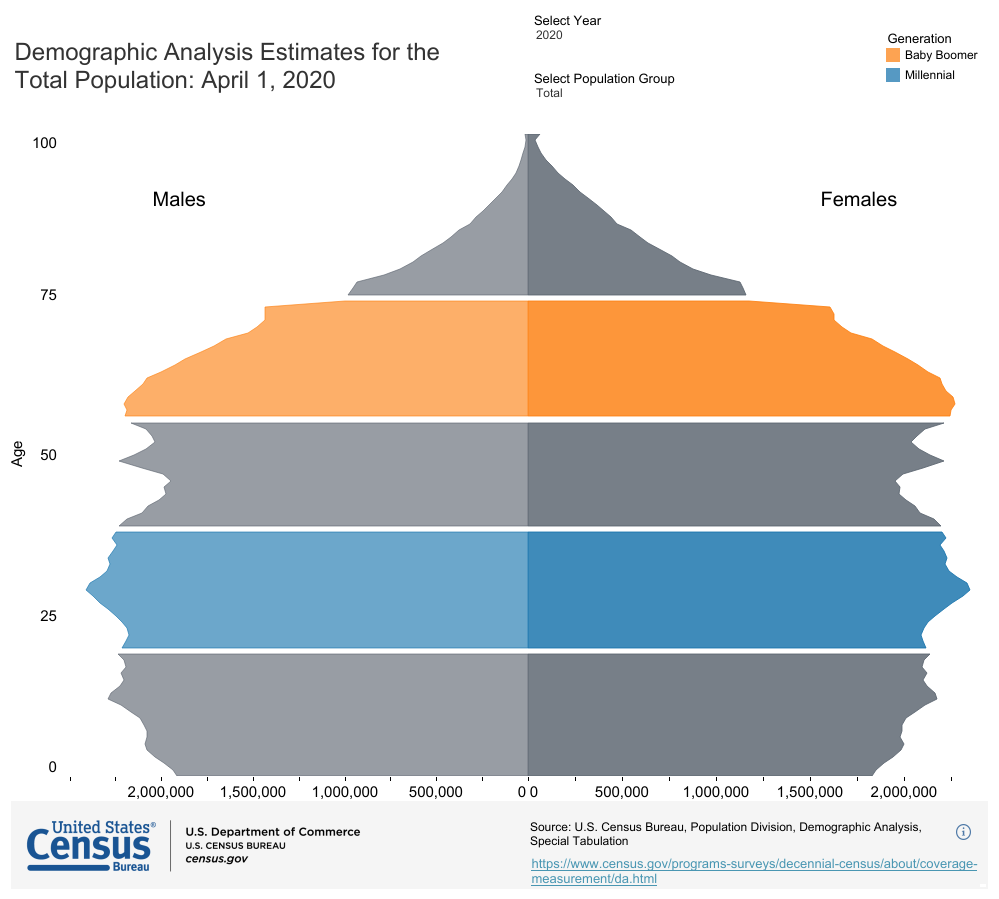

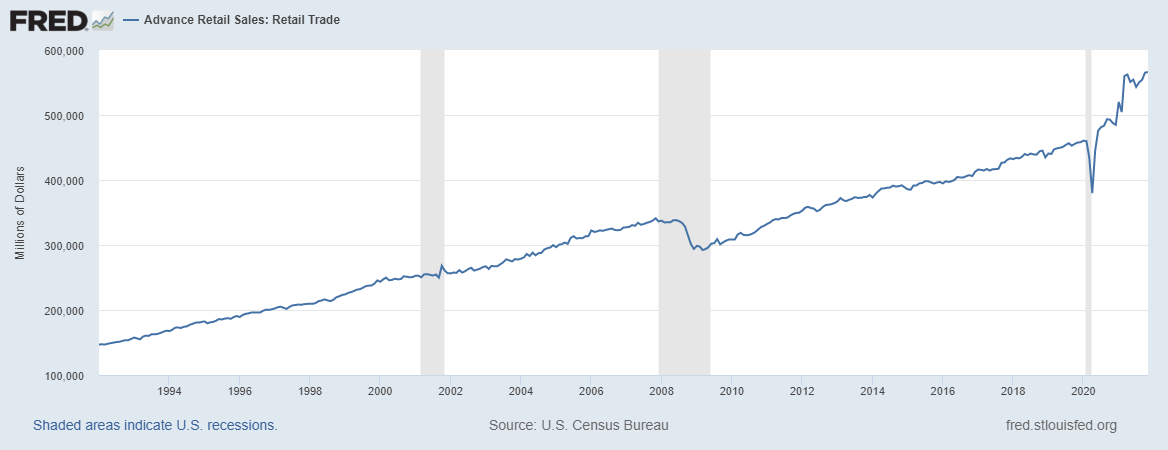

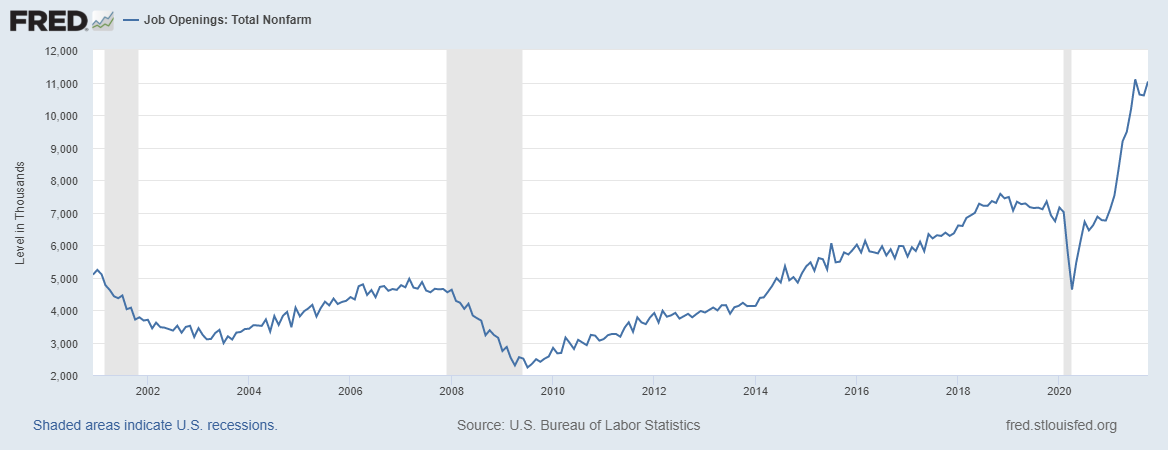

The X factor The one concern I have for this sector in 2022 is if the builders keep pushing the limits of home price growth to make their margins look better. When rates are low, they have the pricing power to do this. This is why the sector has done so well in 2021. If I am wrong about mortgage rates staying low in 2022, and rates go above 3.75% with duration, then demand for new homes should get hit. The longer-term concern for this sector is price growth because if demand slows down, this means a slowdown in construction and the builders really maximized their pricing power in 2020 and 2021. Home pricesThe forecast I am looking for total home-price growth to be between 5.2% and 6.7% for 2022. This would be a meaningful cool down in price growth but would still be a third year straight of too much price growth for my taste. The backstoryMy biggest fear for the housing market during the years 2020 to 2024 was that real home-price growth can be unhealthy. When you have the best housing demographic patch ever recorded in history occurring at the same time as the lowest mortgage rates ever, with housing tenure doubling as it has in the last 12 years, it’s the perfect storm for unhealthy price growth. Housing inventory has been falling since 2014 and mortgage purchase applications have been rising since then. As you can see below, 2021 wasn't looking good for me regarding my fear for home prices rising too much. The X factorWhen I talk about real home-price growth being too hot, I mean that nominal home price growth is above 4.6% each year during the five-year period of 2020 to 2024, for a cumulative 23% growth. This would not be a positive for the housing market. If we end 2021 with 13% home price growth, (and it looks like we will do that or higher), then we have already achieved 23% of the price growth that I am comfortable with in just two years. While I do believe home-price growth is cooling from the extreme high rate of growth we had earlier in the year, I would very much like to see prices get back in line with my model for a healthy market. In order for this to happen, we would need to have no increase in home prices for the next three years. Because inventory levels are falling again, and we are at risk of starting the 2022 spring season at fresh new all-time lows, this outcome is very unlikely. Housing demandThe forecast Everyone is talking about rates going higher and no one, it seems, is talking about the possibility that mortgage rates could go under 3% in 2022, except me. This is front and center in my mind. I want to see a B&B housing market: boring and balanced. In a B&B market, buyers have choices, sales move at a reasonable pace without bidding wars, and the whole home-buying experience is less stressful and more sane. I would like to see inventory get toward 1.52 – 1.93 million, (which is still historically low). However, this will be a more stable housing market. The backstory Millions of people buy homes each year. The only thing that cooled demand for housing in the previous expansion was mortgage rates going over 4% with duration. The increase in rates didn't crash the market or even facilitated negative year-over-year home price declines; but it did increase the number of days homes stayed on the market. Currently the biggest demographic patch ever recorded in U.S. history are ages 28-34, the first-time homebuyer median age is 33. When you add move-up, move-down, cash and investor demand together, demand will be stable and hard to break under the post-1996 trend of 4 million plus total sales every year in the years 2020-2024. The X factor Frankly, I'm getting tired of calling this market the unhealthiest since 2010. This is not due to a massive credit boom or exotic loan products contaminating the market with excess risk — it's the lack of choice for buyers. If mortgage rates go under 3%, which I believe they can, it just keeps the low inventory story going on. The Federal Reserves wants to cool down the economy, the government is no longer providing disaster relief anymore and the world economies should get hit if the U.S. dollar gets too strong. So, my concern is about rates falling in year three of my 2020-2024 period. This is also a first-world problem to have and we aren't dealing with the housing market of 2005-2008 when sales were declining and the U.S. consumer was already filing for bankruptcy and having foreclosures before the great recession started in 2008. This is to give you some perspectives here with my thinking. The economyThe forecastI expect the rate of change to slow in 2022 but the economy will still be expansionary. Retail sales have been off the charts, and this data line, which I expected to moderate, still hasn’t. The rate of growth will cool. Replicating the growth we saw in 2021 will be nearly impossible. As the excess savings have been drawn down and the additional checks that people got are no longer coming, this data line will find a more suitable and sustainable trend in 2022. Still I am shocked that moderation hasn't happened already and I was the year 2020-2024 household formation spending guy, too. The backstoryThe U.S. economy has been on fire this year. Even with the excess savings, good demographics, and low rates, not even I thought we would see economic growth like we did in 2021. However, like all things in life, despite the peaks and valleys, the overall trend will prevail. The X factorI recently raised one of my six recession red flags after the most recent jobs report as the unemployment rate got to a key level for myself. These red flags are more of a progress checklist in the economic expansion, and when all six of my flags are raised, I go into recession watch. The economy is in a more mature phase of expansion since the recovery was so fast. Like everything with me, it's a process to show you the path of this expansion to the next recession. For housing, a strong labor market means more people are getting off forbearance, which is already under 1 million, much smaller than the nearly 5 million we had early in the crisis. I want to wish a Merry Christmas to all my forbearance crash bros who promised a housing crash in 2020 and 2021. You guys are the best trolling grifters ever! So, look for the rent inflation story to be part of the 2022 storyline, as well as the rate of growth of home prices cooling down. For more discussion on this index and the America is Back recovery model, this podcast goes over everything that has happened in 2020-2021. ConclusionWhat a ride it has been for all of us since April 7, 2020 when I wrote the America Is Back economic recovery model for HousingWire. We end 2021 with one of the greatest economic recovery stories ever in the history of the United States of America, and a terrible, dark, two-year period of failure for the extreme housing bears. Now we are well into a recovery and looking forward to a new year with its new challenges. The job of the analyst is to forecast the positive or negative impacts that a whole slew of variables have on the economy based on carefully formulated economic models. The variables, such as demographics, the unemployment rate, what the Federal Reserve is doing, commodity prices and so many others, are constantly in flux and feed off of and influence one another. Additionally, new economic variables pop up all the time. My job, with every podcast and article, is to show you how the changes in these variables light the path to where the economy and the housing market is heading. Take a deep breath — in through the nose and out through the mouth. The last two years have been crazy, but I am glad you are here to read this. This is our country, our world and our universe, and everyone is part of team Life on Earth. Merry Christmas, Happy Holidays and have a wonderful Happy New Year. We will get through 2022 one data line at a time. “We have always held to the hope, the belief, the conviction that there is a better life, a better world, beyond the horizon.” Franklin D. Roosevelt The post Logan Mohtashami: The 2022 housing forecast appeared first on HousingWire. |

| Rocket acquires Truebill app for $1.275B in cash Posted: 20 Dec 2021 07:13 AM PST Detroit-based platform Rocket Companies, the parent of Rocket Mortgage, announced on Monday it is acquiring the personal finance app Truebill for $1.275 billion in cash. The acquisition, expected to close prior to the end of the year, is a step toward a centralized platform for clients to manage their financial lives, the company said. It’s also a step to diversify as mortgage volume slows. Founded in 2015, Truebill has reached $50 billion in monthly transaction volume by offering an app to track spending, build budgets and improve credit scores. The deal, which is expected to connect Rocket to 2.5 million Truebill clients, is expected to bring $100 million in annual recurring revenues to Rocket. That compares to Rocket’s $1.3 billion in annualized mortgage servicing fee income. Jay Farner, CEO of Rocket Companies, said in a statement that Truebill provides an intuitive experience to help its clients save money, a perfect fit for the Rocket platform. The holding businesses include Rocket Mortgage, Rocket Homes, and Rocket Auto. Rocket generated $1.4 billion in net income in the third quarter in the mortgage industry, up from $1 billion the previous quarter. It also originated $88 billion in mortgages in the same period and projects it will reach 10% market share in 2022. Keep Up With the Latest Third Party Origination News Want to stay up to date with the latest on the third party origination front? We designed a specific news hub with lenders and brokers in mind, with Rocket Pro TPO leading the discussion. Presented by: Rocket Pro TPOFarner said that Truebill “follows the same philosophy as Rocket Companies – leveraging the power of technology to remove the friction from complex transactions – and applies it to everyday life.” Truebill was originally a subscription cancelation app but the company expanded its services. It now helps customers renegotiate bills, such as cable and telephone, with a 20% discount and the company says It has saved $100 million for its clients since its foundation. “By joining forces with the Rocket fintech powerhouse, we will be able to extend our reach and seamlessly connect consumers with even more services,” Haroon Mokhtarzada, co-founder and CEO of Truebill, said in a statement. The post Rocket acquires Truebill app for $1.275B in cash appeared first on HousingWire. |

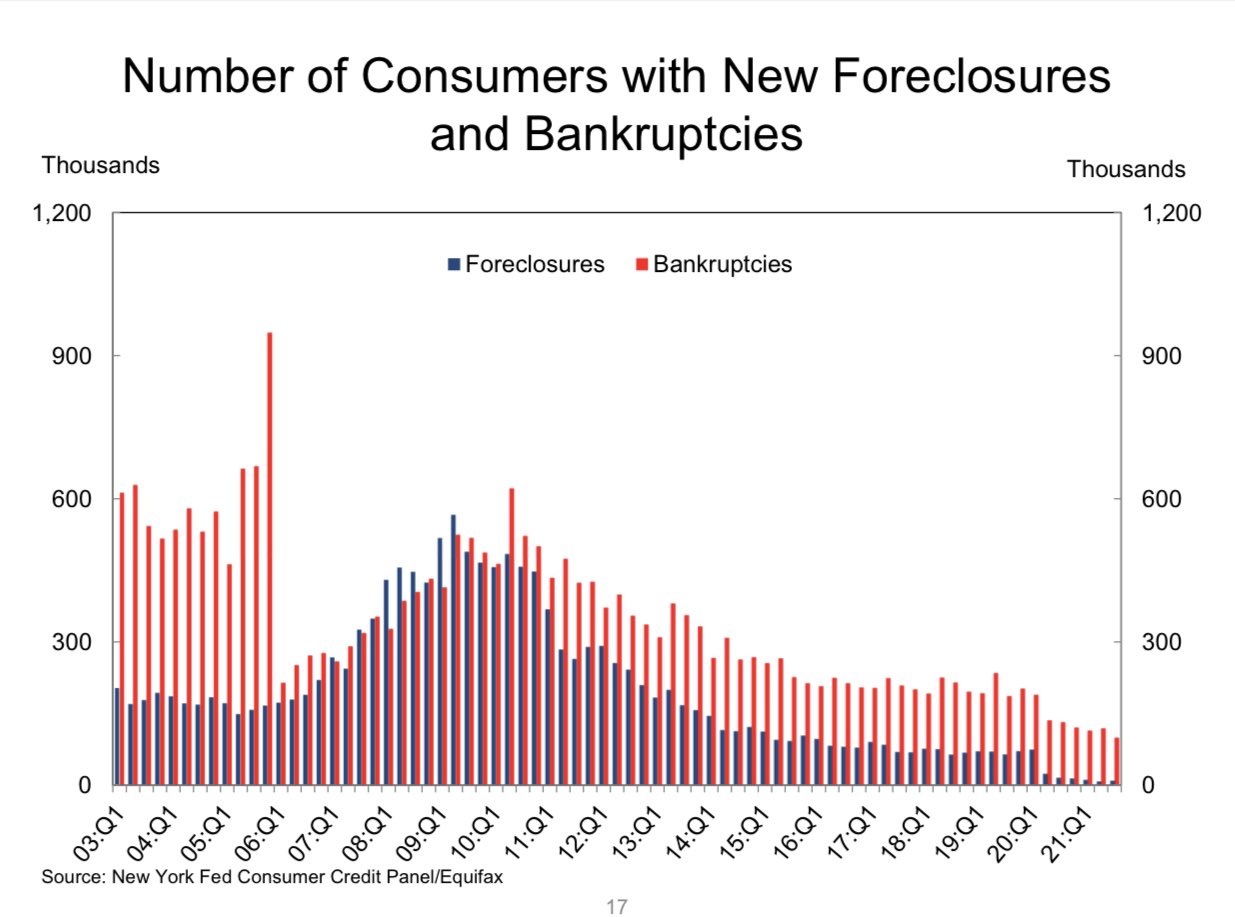

| Help for troubled borrowers is on the way. But will it come soon enough? Posted: 20 Dec 2021 03:00 AM PST  The Covid-19 pandemic hit Jeffrey Wilen and his family hard. In July 2020, he lost his job as an editor at a consulting firm for spa professionals. By that point, his wife, fearing infection, had already decided to resign as a part-time assistant teacher to stay home with their three kids. It took Wilen, 49, about two months to get a new job. In September 2020, he landed a job as a service advisor assistant for an auto repair shop. “I’m still in this job, but I’m not making as much as I was at the previous one,” he said. Since the pandemic first hit, the family’s annual income decreased from around $80,000 to $41,600, according to Wilen. While they wait for the best moment for his wife to return to work – they are still afraid of new Covid-19 variants – he is hustling at side jobs after his shift at the auto repair shop. “What’s happened is that the economy has changed a lot. Gas is more expensive. Groceries are more expensive,” he said. “I’m trying to make an extra anywhere.” Wilen is working with food delivery, which guarantees between $100-200 per week. A $250 monthly child tax credit from the federal government for each child also helps the household. But will end in December. While the family’s income has been cut by almost half and inflation has increased their expenses, Wilen’s primary concern is his mortgage. In 2015, the family paid $250,000 for a 2,900-square-foot house in Ormond Beach, Florida. The four-bed property was perfect for the pre-Covid reality, but it is challenging to afford right now. When Wilen lost his job last year, he stopped paying his $1,460.10 mortgage for 12 months, and the county where he lives paid three months of his mortgage bill as part of an assistance program. “But all my forbearance is done, and I can’t get any more,” Wilen said. He is afraid of losing his home. Wilen’s case illustrates how some Americans have a lot to lose if policies designed to help mortgage borrowers don’t break right. Governments and servicers were both quick to launch forbearance programs for over seven million mortgage borrowers during the pandemic, realizing the historic challenge borne out of the Covid-19 pandemic. The fast and efficient response worked – a foreclosure crisis has not materialized, and most experts do not believe there's a threat of a huge wave of foreclosures in the cards. But housing experts say a new phase of financial aid needs to be issued imminently to help those who are exiting forbearance and are still struggling to pay their mortgages. Black Knight data shows that roughly 450,000 forbearance plan expirations are expected to occur through the end of 2021, representing more than a third of active plans. “We are concerned that we are going to see more and more people in this same position in the coming months: many homebuyers who lost jobs are back to work but making less money,” said Jackie Boies, senior director at Money Management International, a nonprofit that provides credit and debt management counseling. “They’ve had a manageable budget due to mortgage forbearance. Now mortgage forbearances are coming to an end, and many homebuyers will not be able to pay their mortgage again.” The unemployment rate checked in at 4.2% in November 2021, down from 14.8% in April 2020, according to the U.S. Department of Labor. Still, some borrowers haven’t regained employment or are now under-employed. “Just because there are a lot of jobs out there doesn’t mean there are jobs that are paying as well as they were before the pandemic,” said Stephanie Moulton, professor at the John Glenn College of Public Affairs from the Ohio State University and an expert in public policy implementation. A $10 billion hopeThe biggest hope for borrowers who can’t pay their mortgages – apart from winning the lottery – is the Homeowners Assistance Fund (HAF) program. A component of the American Rescue Plan Act, it was approved by Congress in March. The fund allocates $10 billion to prevent homeowners from falling behind on their mortgage, losing utility services, or being displaced. The money can be used for mortgage payment assistance or mortgage principal or interest rate reductions. It can also cover utility payments, including electric, gas, home energy (firewood and home heating oil), water, and wastewater. Homeowners have to document and describe their financial hardship, which has to have occurred after Jan. 21, 2020. They also must have incomes that do not exceed 150% of either the area median income or 100% of the median income for the United States, whichever is greater. According to the latest U.S. Census Bureau data, the median household income in Volusia County, where Wilen lives, is $49,494, so he would be a target. States and eligible territories are tasked with administering the money, subject to the U.S. Department of the Treasury approval. Each state must also submit its own HAF plans to the Treasury for approval. As of October, 10% of the funds have been distributed upfront for states to initiate pilot programs. But few territories and states received a green light to implement their complete plans. “Right now, it is the time to get the HAF implemented,” said Moulton. “Forbearances are starting to expire. If we go much beyond Jan. 1, it might be too late for some borrowers.” According to consumer protection lawyers, advocates, and housing counselors, the expectation is that some state programs will be up and running sometime in the first quarter of 2022. After the plans’ approval, borrowers need to submit applications to the states, more complicated than the automatic forbearance plans provided to millions after a phone call to their servicers. Additionally, states will have to select and reach out to borrowers, which can take some time. Mortgage servicers are negotiating uniform procedures and documents with states, so their interactions can be faster when paying borrowers’ debts. “Servicers don’t want to get in a position where the customers think they are deciding who gets the money or not,” said Dana Dillard, principal advisor at Housing Finance Strategies, a consulting firm for the mortgage and servicing industry. Up to the task?The recent experience with state distribution of rental assistance and unemployment insurance is perhaps a preview of the challenges ahead. Between January and July, states and local governments spent only 20% of the $25 billion in emergency rental assistance funds available in the first round of the program, according to the Treasury Department. The Treasury launched new measures in August to reduce processing delays – for example, allowing self-attestation when other documents were not available. Even by October, states such as Arizona (5%), Ohio (14%), and Florida (39%) distributed only a small share of their resources under the first phase of the program, according to the Treasury. Some states decided to prioritize payments via counties, which also had challenges in the distribution. In Arizona, counties distributed, on average, 71% of their funds, while in Florida the average was 58% and in Ohio, 51%. The Treasury estimates that at least 80% of the ERA's funding will be spent or obligated by year-end. States, overwhelmed with claims and understaffed, also had problems paying unemployment insurance. In some cases, people waited more than three months before they received a check, forcing them to make the choice between a number of terrible decisions – paying credit cards, buying food, making mortgage payments, or getting needed prescriptions. The Department of Labor also reported that as of Sep. 27, states and territories had identified $18.3 billion in overpayments made in the federal programs (regular and those related to the CARES Act) from April 2020 through June 2021, including $1.5 billion resulting from fraud, which reduces trust in programs. The U.S. Government Accountability Office (GAO) is examining the implementation of the programs, including the implications of high claims volumes on the timeliness of benefit payments. GAO has interviewed 10 states (Arizona, Florida, Louisiana, Massachusetts, Michigan, Minnesota, New York, North Dakota, Wisconsin, and Wyoming) and plans to complete this work in the late spring of 2022. In Florida, where Wilen lives, the Department of Economic Opportunity (DEO) also had delays and overpayment related to the state unemployment assistance program. “Many claimants, believing they were fully and accurately applying for Reemployment Assistance within the bounds of the law, received overpayments from the state,” Gov. Ron DeSantis wrote in a letter to the DEO on Oct. 15 recognizing the problem. He requested the state’s Chief Financial Officer to indefinitely defer all referrals to collection agencies for all non-fraudulent overpayments incurred during the pandemic. The DEO told HousingWire that the state is not collecting the overpayments to ensure claimants do not experience adverse impacts to their credit scores. Also, the DEO said it is implementing 20 projects to modernize its systems, and 97% of all eligible benefits requested before Oct.15 for state assistance have been paid to claimants. This same department will be responsible for allocating more than $676 million related to the HAF program in Florida. The state submitted the plan on Aug. 20 for review and approval. “Once the HAF Plan is approved, DEO will implement the program,” the DEO wrote to HousingWire. The first state to have the plan approved in November, New York, will cover up to $50,000 per household. “As we focus on our post-pandemic economic recovery, we need to do everything in our power to help New Yorkers stay in their homes,” Gov. Kathy Hochul said in a statement. The fund will distribute nearly $539 million to assist homeowners at the most significant risk of foreclosure or displacement in the state. According to the NYS HAF website, they expect to receive significantly more applications than can be funded by the program. The website explains that applications will be processed in the order they were received, and it does not guarantee financial assistance. Targeting the needy Money for the program is short, so it is crucial to precisely target those who need assistance most. Updated Black Knight data shows that, as of the end of October, there was $58 billion in past-due mortgage principal, interest, taxes, and insurance on first-lien mortgages, down from $64.5 billion at its peak in February 2021. The figure for October is $26 billion above pre-pandemic levels, but experts say most borrowers who missed payments will get back on their feet through loss mitigation programs with lenders. “There’s a mismatch of the need and available resources. Policymakers are going to face trade-offs, and they’re going to have to make decisions [about how to distribute the money],” said John Walsh, a research analyst in the Housing Finance Policy Center at the Urban Institute. The institute has created a dataset that includes homeowners’ demographic and income characteristics, assessing foreclosure risk in counties, so policymakers can better target HAF dollars. Housing policy experts worry that the Covid-19 pandemic exacerbates the inequality in housing ownership – they indicate the HAF program as one way to mitigate this risk. According to data collected by the Census housing pulse survey, the share of white respondents not caught up on their mortgage payments in September was 5%, compared to 12% among Black and 12% among Asians. “We know that the people who are still in forbearance right now, the people that have been struggling to get out of forbearance, are disproportionately people with FHA loans, and they’re disproportionately Black and Brown,” said Moulton. According to the Federal Housing Administration, their share of lending to Black borrowers is around 17%, compared to 6% for the rest of the mortgage market. To help the most vulnerable population, Tara Roche, research manager for the Pew Charitable Trust, said that HAF will be available to those who are using alternative financing, such as land contracts (agreements directly between sellers and buyers) and loans secured by manufactured homes. These contracts lack protections that accompany mortgages, such as forbearance plans and foreclosure procedures. "We reviewed 36 state HAF plans that are publicly available, and we found that so far 21 states have included both groups: residents living in a manufactured home secured by a loan and homeowners with land contracts. And we found that 30 states had included at least one of those groups," she said. Results, however, can change as many plans analyzed are drafts or preliminary programs. The HAF rules stated that any amount not made available to homeowners that meet income-targeting requirements must be prioritized for assistance to socially disadvantaged individuals, with funds remaining after such prioritization available for other eligible homeowners. “The main challenge is to reach the population that is designated by statute, and the population who you think is most in need of this type of assistance,” said Meg Burns, executive vice president at Housing Policy Council. According to Burns, a simple program that is standardized across the states will help the most people, as complexity can be a barrier to success. If the program does break right, the benefits for the housing market are clear. Looking to the past, a study by six housing policy experts and economists – from universities such as Washington University, the Ohio State University, and the University of North Carolina – shows that the Treasury Department spent $45 billion to assist homeowners in the Great Recession. The most significant share went toward the Home Affordable Modification Program (HAMP), which launched in 2009. But solutions for mortgage borrowers were focused on permanent loan modifications, with mixed success. In 2010, the Treasury launched the Hardest Hit Fund (HHF) program. The most significant subsidy was for mortgage payment assistance, paying homeowners’ loans until they secured employment or up to a typical maximum of 12 to 24 months. The HHF, which is based on mortgage payment relief, served as an inspiration to the HAF program. According to the study, HHF assistance leads to a 40% reduction in mortgage default and foreclosure probability through four years post assistance. The program prevented $8.3 billion in financial loss to lenders, investors, and governments during the Great Recession. “It is important to consider that now the housing market is much stronger than it was during the Great Recession: borrowers can sell their home, they’re not as likely to be underwater,” Moulton, one of the study’s authors, told HousingWire. Sell, and go where?But some troubled borrowers resist the idea of selling their homes, downsizing or becoming renters. Wilen, for example, has an outstanding balance as of Sept. 16 of $165,651.25 (his past due amount related to the forbearance is $20,095.95). His house value is estimated between $390,000 and $440,000, according to various automated valuation models. But, due to rising house prices in his area, he is afraid he will not find a house to accommodate his family adequately. In Volusia County, where he lives, home prices rose by 12.6% in the second quarter, compared to a year earlier, according to the National Association of Realtors (NAR). In addition, there are costs associated with moving to a new place. “The situation is frustrating. It is not my fault that I lost my job because of Covid,” he said. Since his forbearance plan expired at the end of September, Wilen has talked to his servicer, Lakeview, to find a solution. This was the first time he had to negotiate the mortgage in six years, and the option offered was a loan modification, he said. Lakeview didn’t answer phone calls and emails to comment on the case. Wilen is afraid he will not pay even a lower mortgage bill. “This month [November] has been a struggle just making regular bill payments. My car payment was late for the first time because I couldn’t afford it. It was either the water bill, the power bill, the food, or the car,” he said. “If they tell me, ‘You’re gonna have to start paying $1,000 a month for a mortgage,’ I’ll be honest: I don’t know how I’m going to do it with my current income.” According to counselor Jackie Boies, from the Money Management International, borrowers exiting forbearance have several options. If they can pay a mortgage, they can benefit from a loan modification or refinance, which will bring the mortgage current and lower the monthly payment. Borrowers who can’t afford a modified payment will need to consider increasing their income with a second job, selling their home and downsizing considerably, and potential sale lease-back options. Regarding Wilen’s situation, she said: “Truth is if he doesn’t want to be homeless, he’ll have to pay a mortgage payment or rent. Typical loan modifications might bring his payment down to just under $1,000, but he needs to tackle this now and not delay. Once he’s significantly delinquent, he has fewer options.” She advises borrowers exiting forbearance and struggling to pay their mortgages to meet with a housing counselor. “There are a lot of emotions tied to your home. Part of the job of the counselor is to help that consumer set aside the emotional pieces and think about their overall financial picture.” Boies adds: "A counselor can also help borrowers look for resources. The difficulty is that resources vary greatly in cities, states, counties. Some have funds, but some don't." The post Help for troubled borrowers is on the way. But will it come soon enough? appeared first on HousingWire. |

| Conforming loan limits draw scrutiny Posted: 20 Dec 2021 02:00 AM PST  Redwood Trust Inc. has long been a major player in the private-label securitization market, and it sees a looming problem brewing in the housing industry. That issue is about boundaries — specifically, the line drawn between the roles of private industry and the government in the housing market. Redwood completed more than $1 billion worth of private-label securitizations involving jumbo and business-purpose loans in the third quarter of this year alone, U.S. Security and Exchange Commission filings show. The company, through its Sequoia program, has been particularly adept at working in the jumbo loan market — securitizing some $30 billion worth of high-balance loans across 76 private-label deals since 2008, according to company officials. That's why the company is concerned with the expanding conforming-loan limits set by the Federal Housing Finance Agency (FHFA), which oversees the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. In particular, FHFA's recently announced 2022 conforming loan limit of $970,800 for single-family homes in high cost areas of the country has caught Redwood's attention. "The GSEs could more effectively support their affordable-housing mission with a reduced focus on high-balance loans," states a white paper recently published by Redwood. "High balance loans divert capital and other resources to activity that does nothing to promote affordable housing." Redwood's case against the conforming loan limits set for high-cost areas revolves around a couple of major markers that seem to merit attention in both the private- and public-sector. They boil down to the following:

"We disagree with the notion that high-cost areas need a higher loan limit to make homes affordable to local buyers," Redwood President Dashiell Robinson said. "In our whitepaper, we identify a number of counties across the U.S. (there are many others) in which the GSE loan limits are supporting home values for income levels that are two-times that county's median household income. "Focusing more on loan sizes and products that support families earning at or below the median household income would better align with the GSE's mission on affordability." In terms of the role of the GSEs versus the private market, Redwood executives also see the line shifting in an unproductive direction for the market. Robinson points out that "the private market has a consistent track record of providing rates at or better than the GSEs through a balanced model of securitizing and distributing whole loans to portfolio lenders like banks and insurance companies. " Redwood's white paper notes that overall private-sector jumbo loan origination volume for this year is estimated at $569 billion, with the average jumbo rate at 3.10%, compared to the average GSE conforming loan rate of 3.12%. Robinson said the private market can price jumbo loans as efficiently as the agency market, pointing out that in 2021, the private-label market will securitize an estimated $60 billion worth of jumbo loans, triple the level of any prior year in the past 10 years. He said that highlights "the liquidity and appetite for privately funded mortgages at increased levels of scale." "Many traditional jumbo borrowers have an income or reserve profile that takes more specialized underwriting expertise to analyze and deem appropriate — for instance, many own their own businesses," Robinson added. "The expertise in underwriting these types of borrowers is inherent in established private-market processes for underwriting and due diligence, which are in many ways different than what originators are required to do when selling to the GSEs." Redwood is not alone in its push to have the FHFA and market leaders in general re-examine the auto-pilot system of increasing conforming loan limits that has become the norm. "Whether taxpayer backing of $1 million mortgages is consistent with the GSE charter is a question that legislators and policymakers should address," said Ed DeMarco, president of the Housing Policy Council (HPC) and acting director of the FHFA from 2009 to 2014. "Home prices are high in select parts of the country, yet mortgages of this size are clearly being made to families at higher income levels. "… Our concern is that policymakers and legislators are not addressing the question of what the appropriate role of government is in the housing-finance system." DeMarco adds that from HPC's perspective, government intervention in the private market should only happen when there is a need to address a clear public policy goal that the private market has failed to deal with adequately. "With the GSEs operating in conservatorship, backed by taxpayers and established to serve a public purpose, the question for policymakers to consider is whether the loan limits respond to a market failure or further a public purpose," DeMarco stressed. FHFA Acting Director Sandra Thompson, recently nominated by President Joe Biden to become the permanent director of the agency, appears to be listening to the private market's concerns about loan-limit creep, at least when it comes to the question of affordable housing. "Compared to previous years, the 2022 conforming loan limits represent a significant increase due to the historic house-price appreciation over the last year," she said in a prepared statement. "While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million. "FHFA is actively evaluating the relationship between house price growth and conforming loan limits, particularly as they relate to creating affordable and sustainable homeownership opportunities across all communities." DeMarco said Thompson's comments are encouraging, but at the end of the day, resolving this issue will require more parties to come to the table with earnest resolve to address the issue. "We were pleased to see Acting Director Sandra Thompson note the relationship between house price growth and the increasing loan limits and her commitment to evaluate that relationship relative to affordable and sustainable home-ownership opportunities," DeMarco said. "But this requires a full conversation among Congress, the [Biden] Administration, and FHFA." The future of the conforming loan limits, then, will likely ultimately require a political solution, if it runs through Congress and the White House. At least one executive with an Atlanta-based nonbank, however, said he believes the trend line on this issue ultimately leads to a decision favoring the private sector. "The GSEs are not meant to give every single American a loan," said Tom Hutchens, executive vice president of production at Angel Oak Mortgage Solutions, part of Angel Oak Companies, a long-time player in the non-QM market. "And so, I think long-term, they’re probably going to shrink their footprint, as opposed to continue to grow it." The post Conforming loan limits draw scrutiny appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment