Mortgage – HousingWire |

- Mortgage forbearance ticks down to 5.14%

- In UWM’s war with Rocket, brokers must choose a side

- Are we seeing a cash-out refinance crisis?

| Mortgage forbearance ticks down to 5.14% Posted: 15 Mar 2021 01:25 PM PDT The industry is now less than two weeks away from the one-year anniversary of the CARES Act, which provided borrowers with federally backed mortgages the option to receive forbearance for up to 180 days. After many extensions and exits, the Mortgage Bankers Association estimates 2.6 million homeowners are still in some form of forbearance, though that number continues to slowly fall. As of March 7, servicers’ forbearance portfolio volume sits at 5.14% – down six basis points from the week prior. Overall, forbearance share managed to drop or go unchanged in every loan type for the first week of march, with Fannie Mae and Freddie Mac once again boasting the smallest share after servicers' portfolios declined six basis points to 2.88%. Ginnie Mae loans in forbearance experienced the greatest drop, down 12 basis points to 7.16%, while the forbearance share for portfolio loans and private-label securities (PLS) remained unchanged relative to the prior week at 9.05%. One year after the onset of the pandemic, many homeowners are approaching 12 months in their forbearance plan. That’s likely because servicers’ call volumes hit its highest peak since April 2020, and forbearance exits increased to the highest level since January, said Mike Fratantoni, MBA's senior vice president and chief economist. How to make the forbearance process effective To accommodate the large volume of loans still in forbearance, mortgage servicers must have functional, flexible and effective processes in place. Here are some actionable steps to create that process. Presented by: FICSOf the cumulative forbearance exits for the period from June 1, 2020, through March 7, 2021, 27.3% represented borrowers who continued to make their monthly payments during their forbearance period, however, that number has slowly decreased for months now. On the other end of the spectrum, borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place, rose to 14.1%. But homeowners now have more time than ever to catch up. The FHFA recently extended forbearance plans an additional three months past beyond their initial 12 month expiration. With the latest edict, the agency is now allowing borrowers up to 18 months of coverage. This means that some borrowers may now be in forbearance through Aug. 31, 2022. Borrowers who are in forbearance the longest though, are statistically shown to be more likely in distress. Courtney Thompson, senior vice president of default mortgage at Flagstar Bank told HousingWire that servicers have to, right now, flip their programs, and meaningfully connect with the majority of their COVID-19 impacted population. COVID-19 forbearances at the end of last summer saw nearly 40% to 50% of those consumers still able to make their regular monthly mortgage payment and avoid delinquency. “If you look at the same group of consumers now,” Thompson said. “We're down to about 10% that are still making their regular monthly mortgage payment. So we can focus on the population. It's a smaller population than it was last fall, but it's a more needy population.” The post Mortgage forbearance ticks down to 5.14% appeared first on HousingWire. |

| In UWM’s war with Rocket, brokers must choose a side Posted: 15 Mar 2021 09:38 AM PDT  Before Thursday, March 4, John was an unabashed fan of United Wholesale Mortgage. His West Coast brokerage shop sent tens of millions of dollars in loans to the wholesale mortgage giant in recent years. He loved their turn times, found their pricing to be competitive, and had good things to say about his account executive. He also believes UWM President and CEO Mat Ishbia is sincere when he says the ultimatum was issued to protect the broker channel from existential threats, specifically from Rocket Mortgage and Fairway Independent Mortgage. “It’s honestly an excellent company,” he said of UWM. But as of Monday, he will no longer do business with the lender, which originated over $182 billion in mortgages last year and is easily the biggest producer within the space. “The reason I do this, the reason I’m a broker, is because I believe in choice – it’s that simple,” said John, whose real name is being withheld by HousingWire so he can speak openly about his decision. “So Mat can talk about how he’s doing this to protect brokers and all, but I just felt like what he did is anti-choice, anti-consumer and it isn’t aligned with our values. So yeah, we’re not going to sign.” Ishbia, whose company went public in January and is valued at $16.58 billion, made arguably the biggest hardball play in the history of the broker channel in issuing his ultimatum on Facebook Live. At stake is the business of about 3,000 brokers who use UWM, Rocket and/or Fairway. In Ishbia’s estimation, these two companies, which both have retail operations, are trying to cut the broker out of the mortgage equation. Rocket is training real estate agents to originate loans, and Fairway is trying to poach loan officers, he claims. And if such moves go unchecked, brokers could find themselves an endangered species in a decade, Ishbia believes. The post In UWM’s war with Rocket, brokers must choose a side appeared first on HousingWire. |

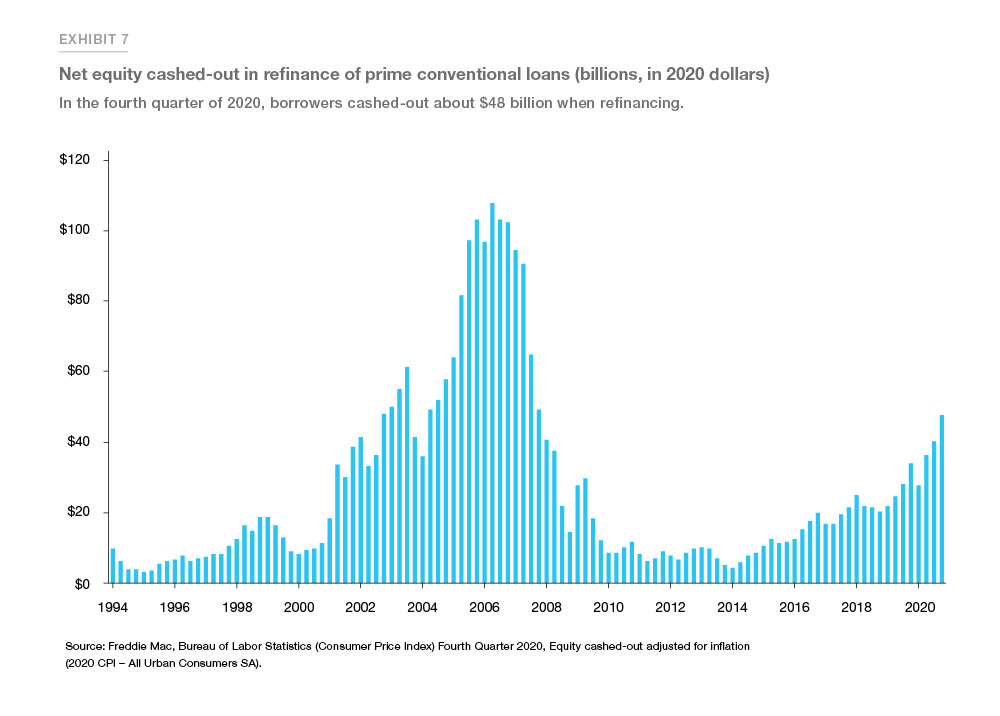

| Are we seeing a cash-out refinance crisis? Posted: 15 Mar 2021 07:34 AM PDT I hear a lot of chatter about a boom in cash-out refinances, and the presumption seems to be that this is destined to wreak havoc on the housing market and the economy at some point. Cash-out loans have been growing over the past few years and it is also true that we have a recent history of excessive equity extraction factoring in a bust in housing. But there are several critical reasons why the recent uptick in cash-out refinancing is nothing like the cash-out boom of the early to mid-2000s. First, the refinance boom's main driver in the 2000s was unhealthy because of the marketplace's speculative unhealthy lending standards. Home prices were growing at an unsustainable level from 2002-2005, leading to some excess risk-taking on inadequate loan debt structures. In the 2020 market, on the other hand, refinances were not driven just by an increase in equity but lower mortgage rates. Cash-out loan borrowers who increased their loan balances could get a more favorable rate than in previous years. Although mortgage refinance activity was the highest in 2020 than it has been since 2003, the reasons for refinancing and the quality of the equity loans are much different than they were in the 2000s. The graph below is from an article by Len Kiefer of Freddie Mac. This is an excellent article for those interested in diving into the minutiae of the 2020 refinance market.

The post Are we seeing a cash-out refinance crisis? appeared first on HousingWire. |

| You are subscribed to email updates from Mortgage – HousingWire. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment